Publication

Metrics

AI Quick Summary

The paper explains the persistent cost-of-carry spread in the European carbon allowance market by linking it to the credit spread of involved corporations. Policy implications suggest that including EUAs in ECB collateral could resolve this anomaly, benefiting the carbon market and EU green transition.

Paper Preview

Abstract

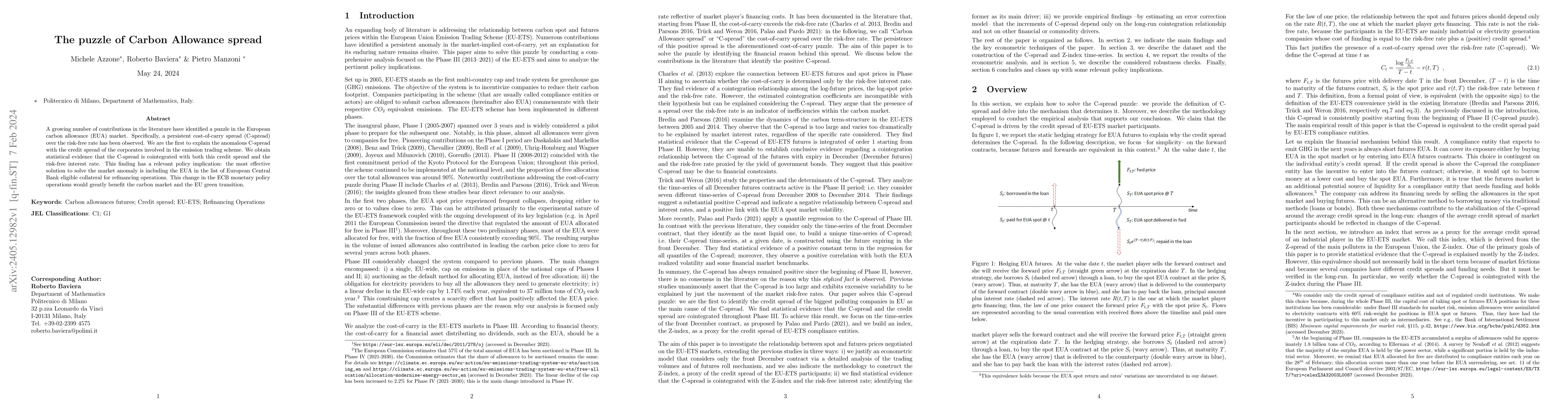

A growing number of contributions in the literature have identified a puzzle in the European carbon allowance (EUA) market. Specifically, a persistent cost-of-carry spread (C-spread) over the risk-free rate has been observed. We are the first to explain the anomalous C-spread with the credit spread of the corporates involved in the emission trading scheme. We obtain statistical evidence that the C-spread is cointegrated with both this credit spread and the risk-free interest rate. This finding has a relevant policy implication: the most effective solution to solve the market anomaly is including the EUA in the list of European Central Bank eligible collateral for refinancing operations. This change in the ECB monetary policy operations would greatly benefit the carbon market and the EU green transition.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0