Academic Profile

Statistics

Similar Authors

Papers on arXiv

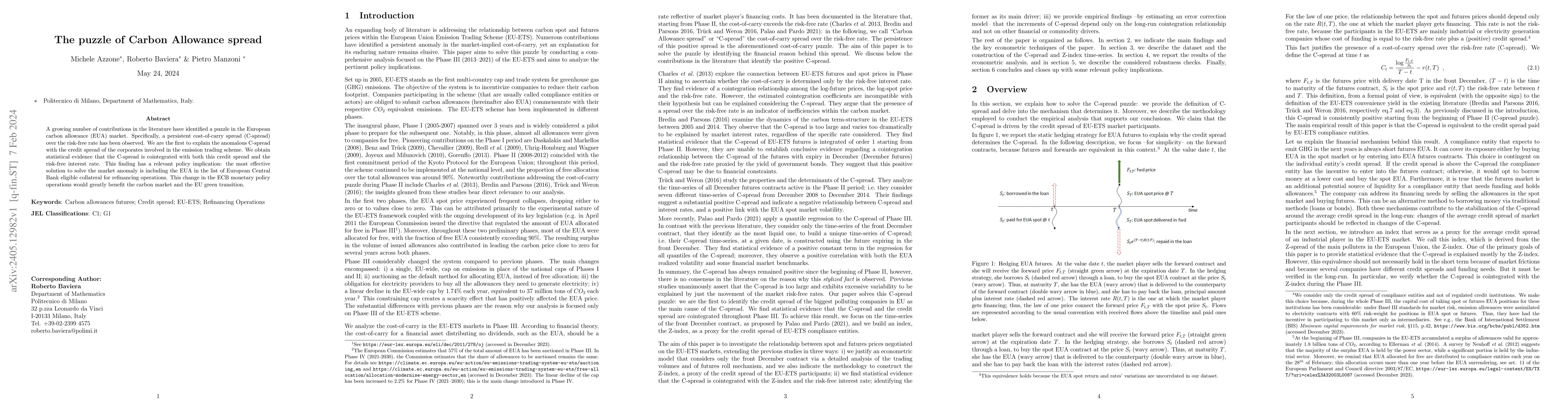

A growing number of contributions in the literature have identified a puzzle in the European carbon allowance (EUA) market. Specifically, a persistent cost-of-carry spread (C-spread) over the risk-f...

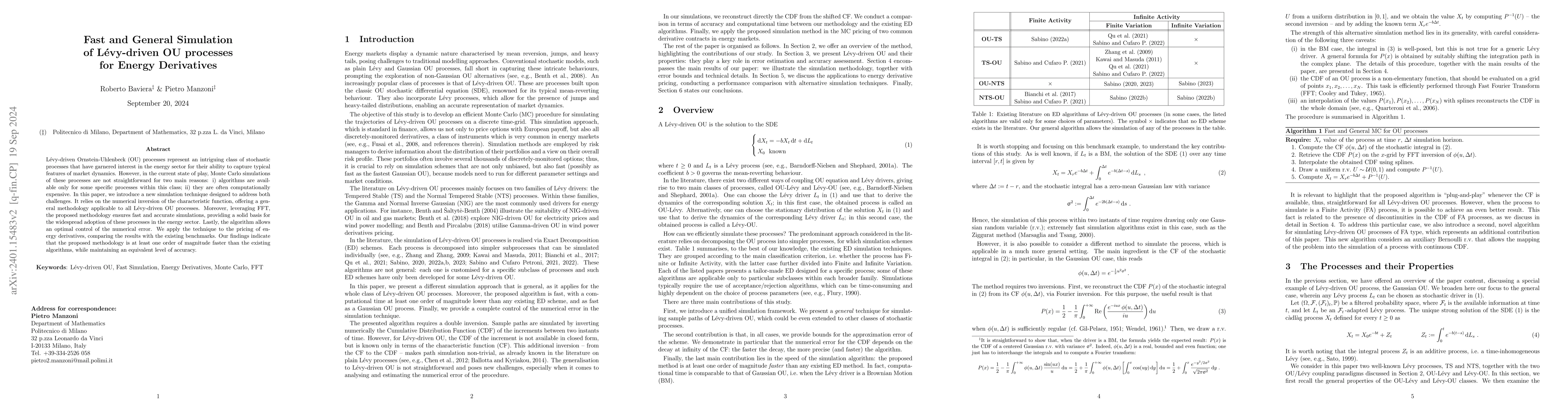

L\'evy-driven Ornstein-Uhlenbeck (OU) processes represent an intriguing class of stochastic processes that have garnered interest in the energy sector for their ability to capture typical features o...

Monroe (1978) demonstrates that any local semimartingale can be represented as a time-changed Brownian Motion (BM). A natural question arises: does this representation theorem hold when the BM and t...

A Recurrent Neural Network that operates on several time lags, called an RNN(p), is the natural generalization of an Autoregressive ARX(p) model. It is a powerful forecasting tool when different tim...

In this paper, we present a very fast Monte Carlo scheme for additive processes: the computational time is of the same order of magnitude of standard algorithms for Brownian motions. We analyze in d...

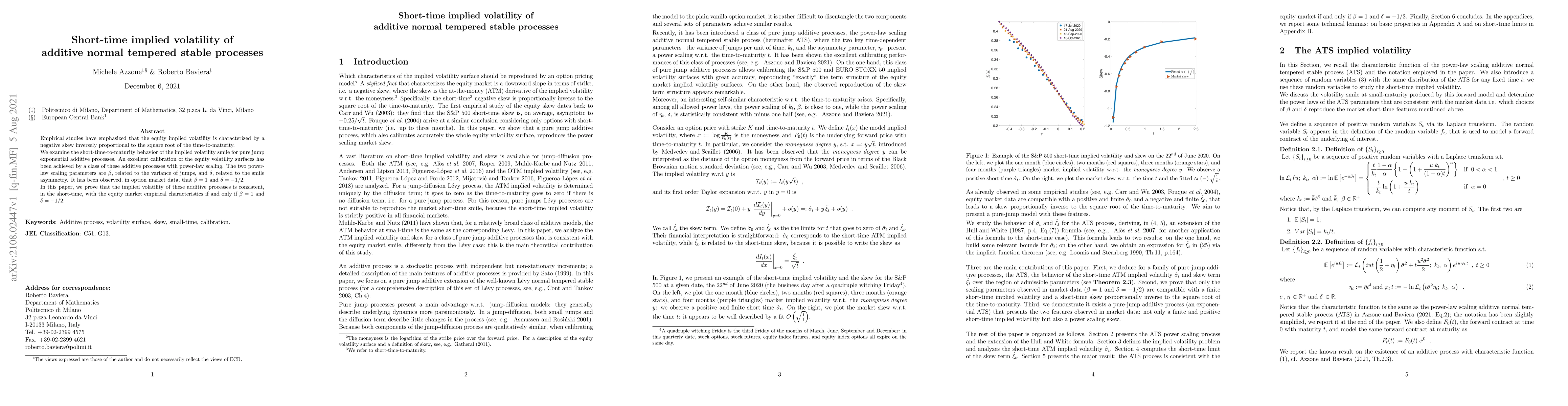

Empirical studies have emphasized that the equity implied volatility is characterized by a negative skew inversely proportional to the square root of the time-to-maturity. We examine the short-time-...

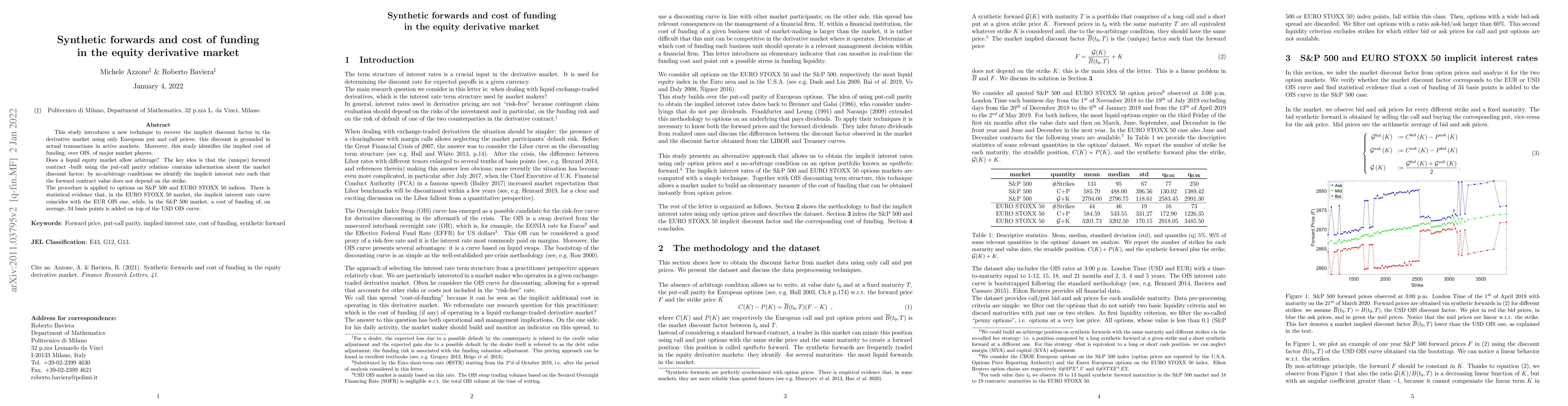

This study introduces a new technique to recover the implicit discount factor in the derivative market using only European put and call prices: this discount is grounded in actual transactions in ac...

Credit capital requirements in Internal Rating Based approaches require the calibration of two key parameters: the probability of default and the loss-given-default. This letter considers the uncert...

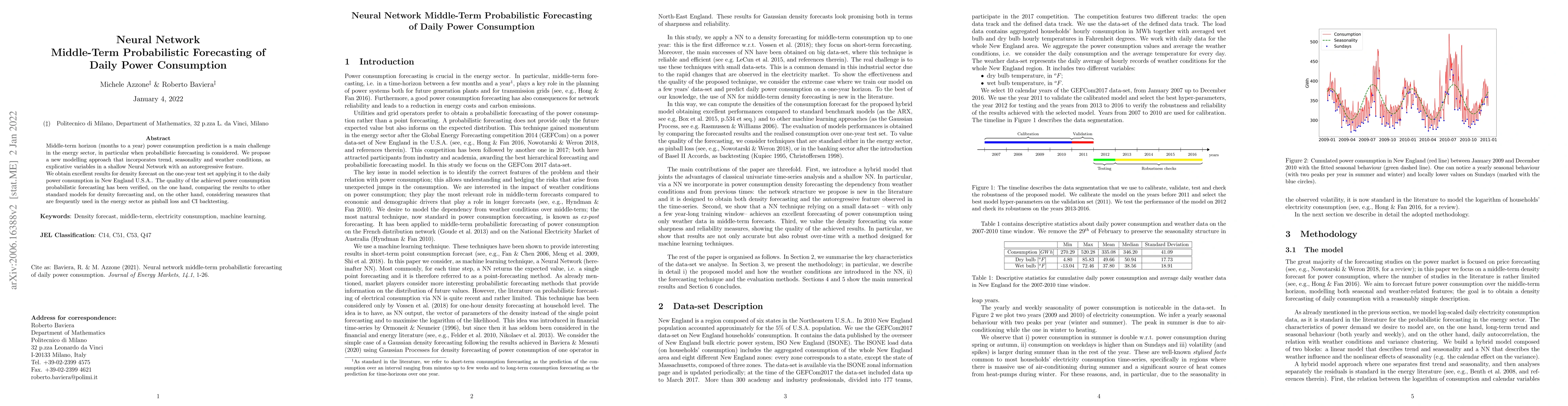

Middle-term horizon (months to a year) power consumption prediction is a main challenge in the energy sector, in particular when probabilistic forecasting is considered. We propose a new modelling a...

We introduce a simple model for equity index derivatives. The model generalizes well known L\`evy Normal Tempered Stable processes (e.g. NIG and VG) with time dependent parameters. It accurately fit...

In April 2020, the Chicago Mercantile Exchange temporarily switched the pricing formula for West Texas Intermediate oil market options from the Black model to the Bachelier model. In this context, we ...

We investigate the asymptotic behaviour of the Implied Volatility in the Bachelier setting, extending the framework introduced by Benaim and Friz for the Black-Scholes setting. Exploiting the theory o...

Modeling the dependence between multiple risk types is a central challenge in contemporary insurance risk management. The standard approaches, Lévy copulas and zero-mixed models, often face practical ...