Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a bootstrap procedure for high-frequency statistics of Brownian semistationary processes. More specifically, we focus on a hypothesis test on the roughness of sample paths of Brownian s...

We introduce a new class of continuous-time models of the stochastic volatility of asset prices. The models can simultaneously incorporate roughness and slowly decaying autocorrelations, including p...

The aim of this paper is to develop estimation and inference methods for the drift parameters of multivariate L\'evy-driven continuous-time autoregressive processes of order $p\in\mathbb{N}$. Starti...

Uncertainty can be classified as either aleatoric (intrinsic randomness) or epistemic (imperfect knowledge of parameters). The majority of frameworks assessing infectious disease risk consider only ...

We present a method for finding optimal hedging policies for arbitrary initial portfolios and market states. We develop a novel actor-critic algorithm for solving general risk-averse stochastic cont...

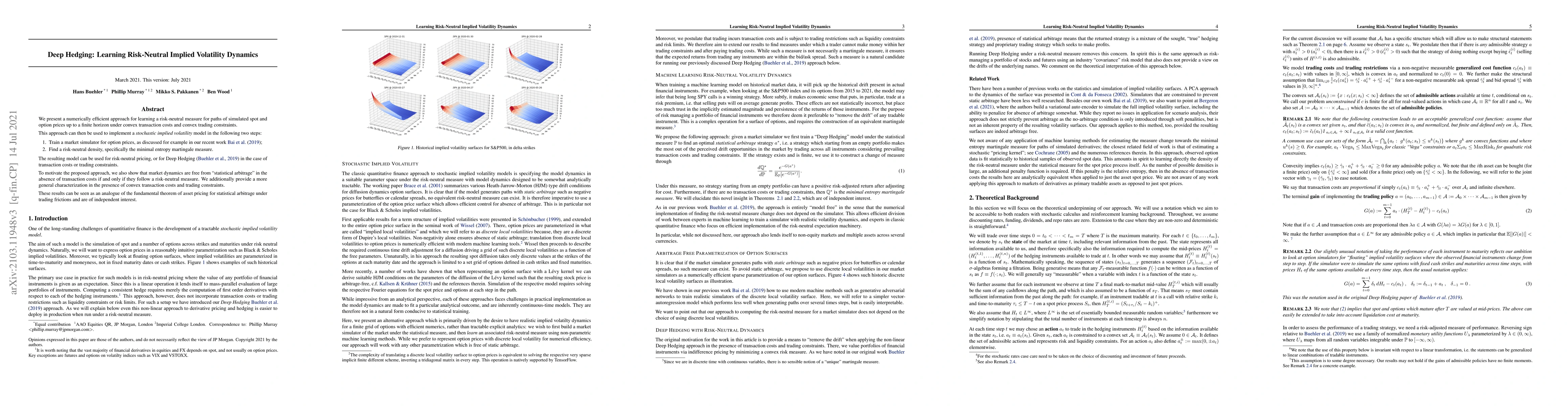

We present a machine learning approach for finding minimal equivalent martingale measures for markets simulators of tradable instruments, e.g. for a spot price and options written on the same underl...

In this article we will introduce the realised semicovariance for Brownian semistationary (BSS) processes, which is obtained from the decomposition of the realised covariance matrix into components ...

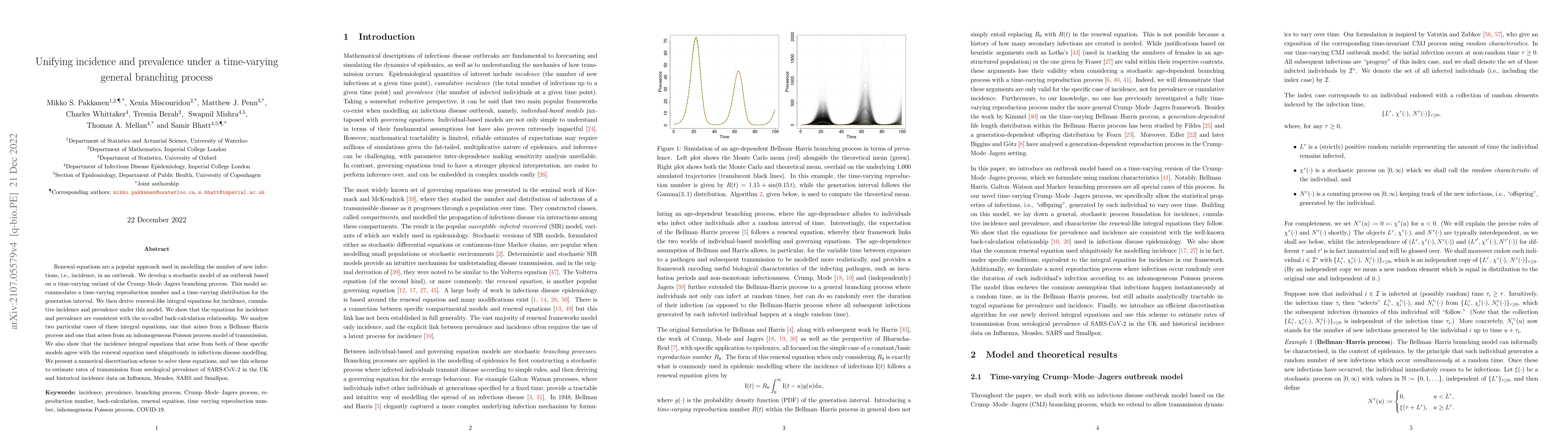

Renewal equations are a popular approach used in modelling the number of new infections, i.e., incidence, in an outbreak. We develop a stochastic model of an outbreak based on a time-varying variant...

We present a numerically efficient approach for learning a risk-neutral measure for paths of simulated spot and option prices up to a finite horizon under convex transaction costs and convex trading...

We develop a GMM approach for estimation of log-normal stochastic volatility models driven by a fractional Brownian motion with unrestricted Hurst exponent. We show that a parameter estimator based ...

In this work we derive limit theorems for trawl processes. First,we study the asymptotic behaviour of the partial sums of the discretized trawl process $(X_{i\Delta_{n}})_{i=0}^{\lfloor nt\rfloor-1}...

We develop a simulation scheme for a class of spatial stochastic processes called volatility modulated moving averages. A characteristic feature of this model is that the behaviour of the moving ave...

The rough Bergomi model, introduced by Bayer, Friz and Gatheral [Quant. Finance 16(6), 887-904, 2016], is one of the recent rough volatility models that are consistent with the stylised fact of impl...

We study the small-time behaviour of the rough Bergomi model, introduced by Bayer, Friz and Gatheral (2016), and prove a large deviations principle for a rescaled version of the normalised log stock...

The expected signature maps a collection of data streams to a lower dimensional representation, with a remarkable property: the resulting feature tensor can fully characterize the data generating dist...

We provide non-asymptotic error bounds in the path Wasserstein distance with quadratic integral cost between suitable functionals of the telegraph process and the corresponding functional of Brownian ...

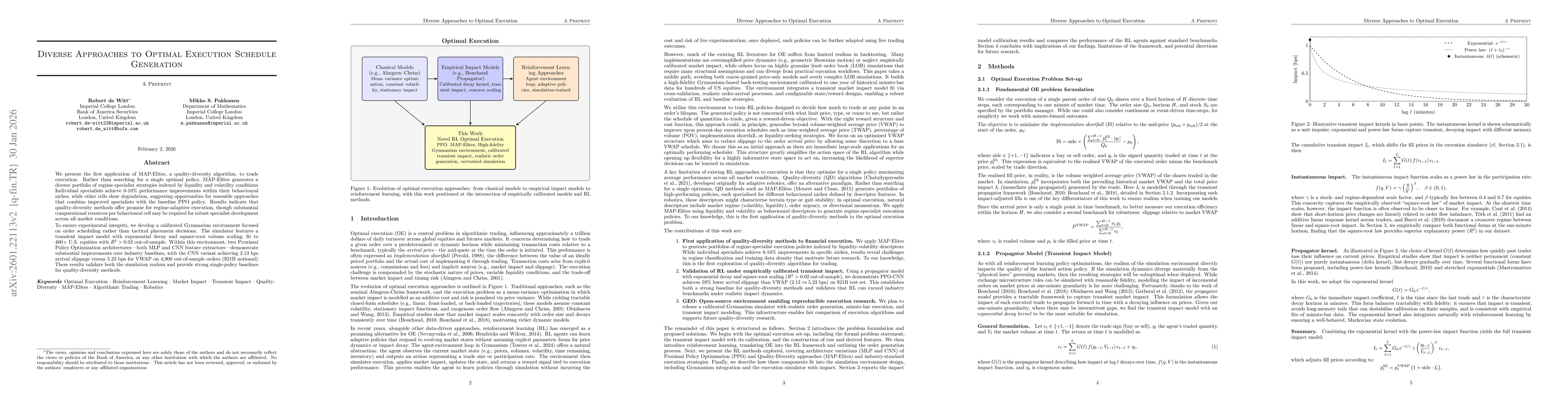

We present the first application of MAP-Elites, a quality-diversity algorithm, to trade execution. Rather than searching for a single optimal policy, MAP-Elites generates a diverse portfolio of regime...