Academic Profile

Statistics

Similar Authors

Papers on arXiv

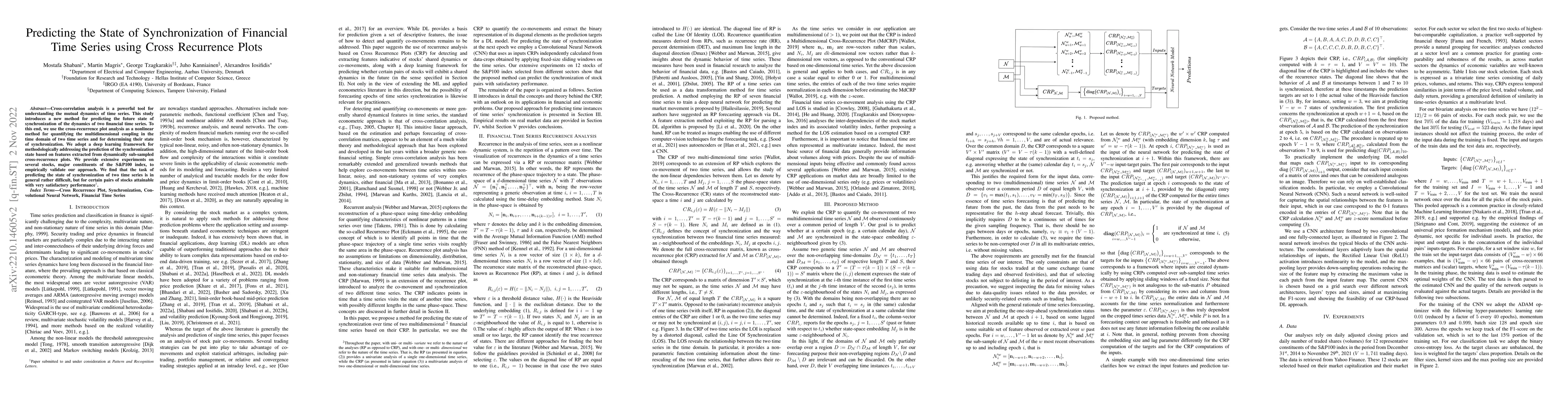

Cross-correlation analysis is a powerful tool for understanding the mutual dynamics of time series. This study introduces a new method for predicting the future state of synchronization of the dynam...

We propose an optimization algorithm for Variational Inference (VI) in complex models. Our approach relies on natural gradient updates where the variational space is a Riemann manifold. We develop a...

Deep Learning models have become dominant in tackling financial time-series analysis problems, overturning conventional machine learning and statistical methods. Most often, a model trained for one ...

We develop an optimization algorithm suitable for Bayesian learning in complex models. Our approach relies on natural gradient updates within a general black-box framework for efficient training wit...

The prediction of financial markets is a challenging yet important task. In modern electronically-driven markets, traditional time-series econometric methods often appear incapable of capturing the ...

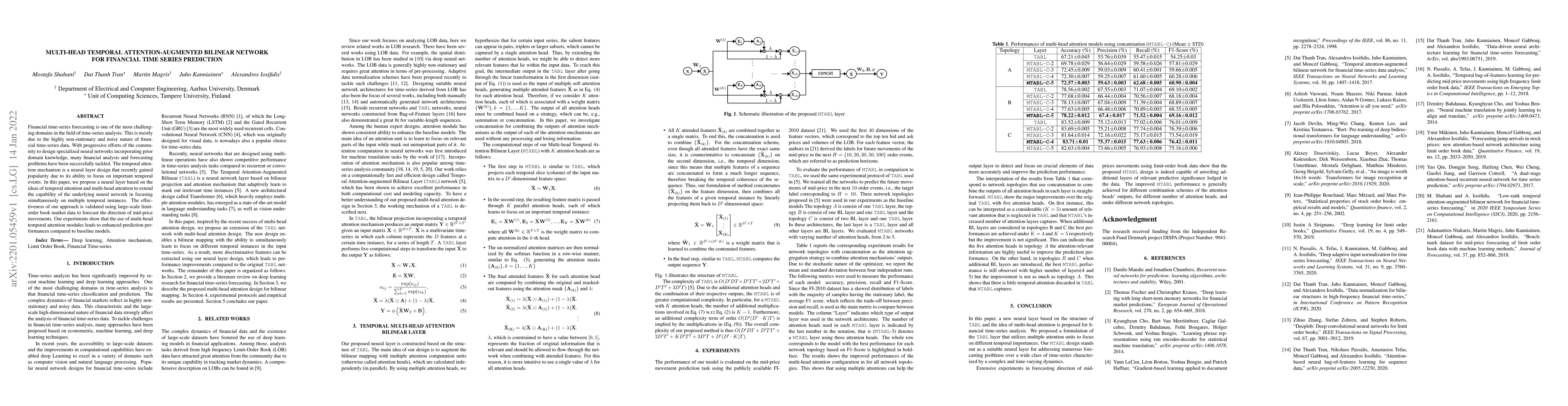

Financial time-series forecasting is one of the most challenging domains in the field of time-series analysis. This is mostly due to the highly non-stationary and noisy nature of financial time-seri...

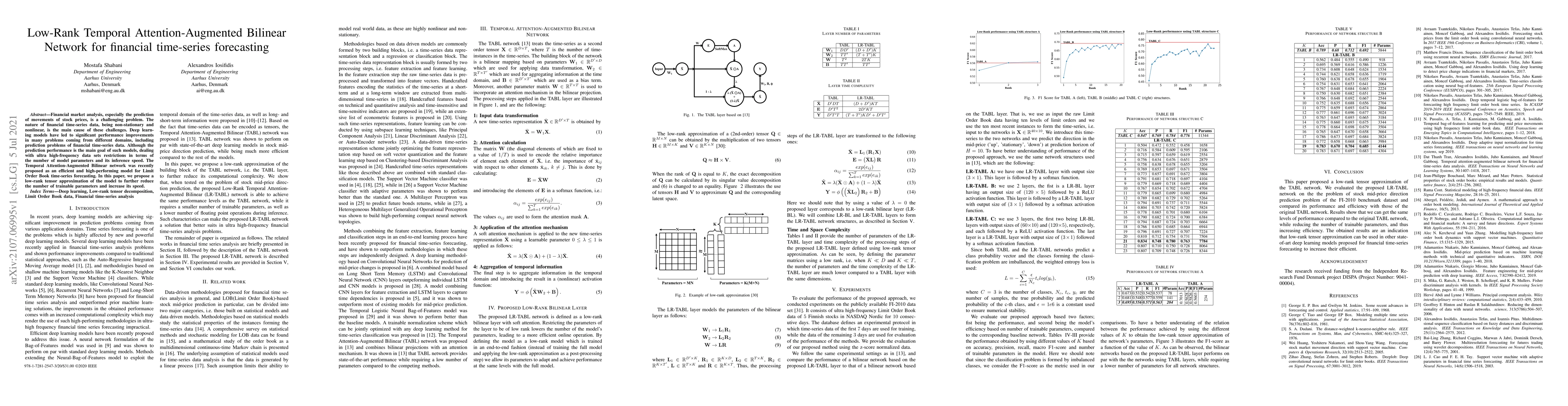

Financial market analysis, especially the prediction of movements of stock prices, is a challenging problem. The nature of financial time-series data, being non-stationary and nonlinear, is the main...