Academic Profile

Statistics

Similar Authors

Papers on arXiv

We reconcile rough volatility models and jump models using a class of reversionary Heston models with fast mean reversions and large vol-of-vols. Starting from hyper-rough Heston models with a Hurst...

Motivated by optimal execution with stochastic signals, market impact and constraints in financial markets, and optimal storage management in commodity markets, we formulate and solve an optimal tradi...

In energy markets, joint historical and implied calibration is of paramount importance for practitioners yet notoriously challenging due to the need to align historical correlations of futures contrac...

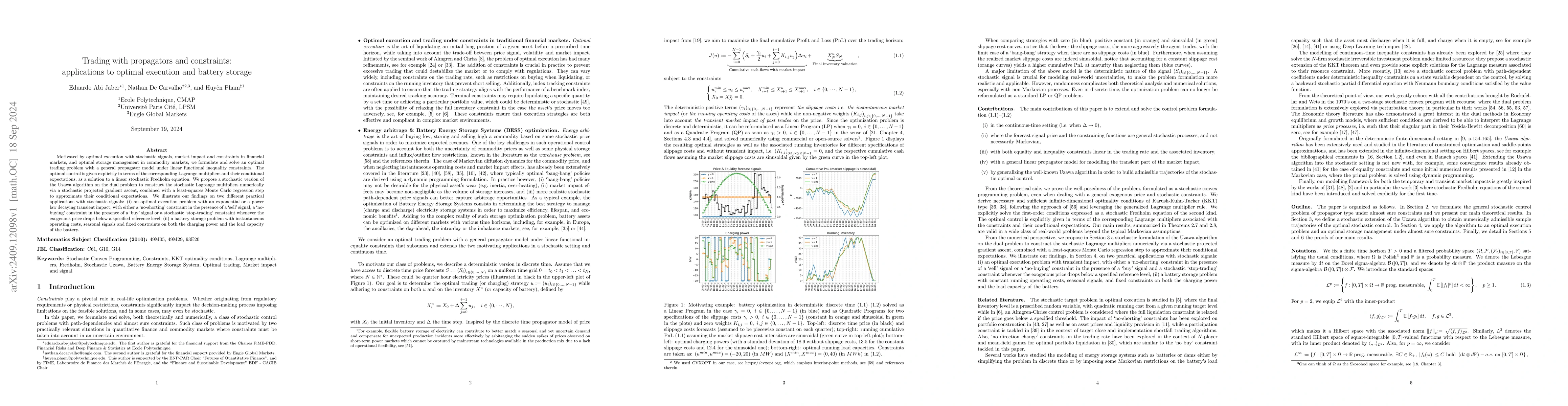

We formulate and solve an optimal trading problem with alpha signals, where transactions induce a nonlinear transient price impact described by a general propagator model, including power-law decay. U...

We consider an optimal trading problem under a market impact model with endogenous market resistance generated by a sophisticated trader who (partially) detects metaorders and trades against them to e...