Academic Profile

Statistics

Similar Authors

Papers on arXiv

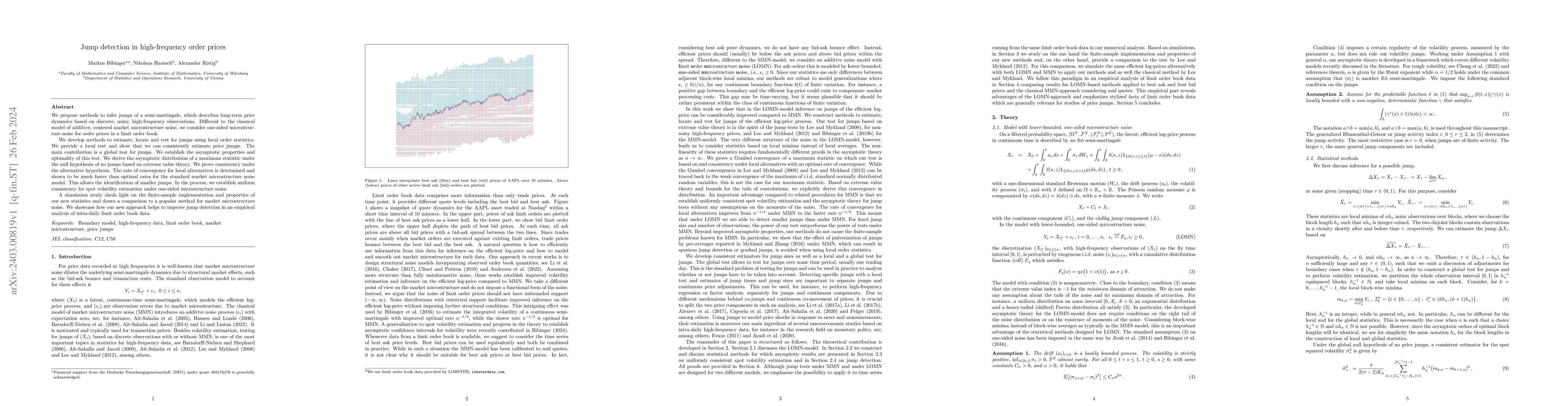

We propose methods to infer jumps of a semi-martingale, which describes long-term price dynamics based on discrete, noisy, high-frequency observations. Different to the classical model of additive, ...

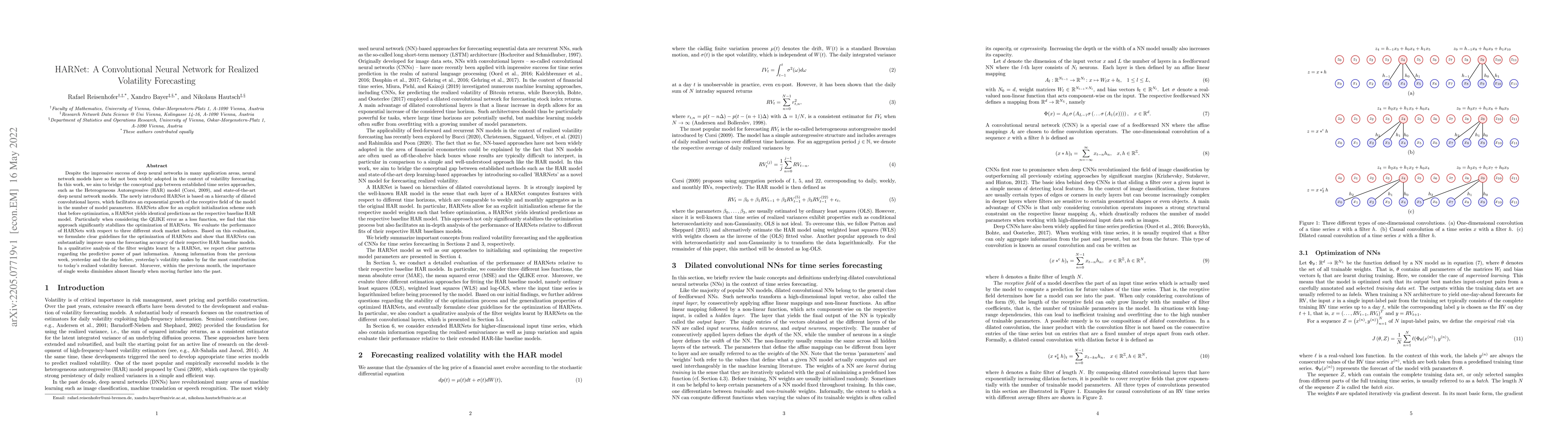

Despite the impressive success of deep neural networks in many application areas, neural network models have so far not been widely adopted in the context of volatility forecasting. In this work, we...

A blockchain replaces central counterparties with time-consuming consensus protocols to record the transfer of ownership. This settlement latency slows cross-exchange trading, exposing arbitrageurs ...

In this paper, we analyze the asymptotic behavior of the main characteristics of the mean-variance efficient frontier employing random matrix theory. Our particular interest covers the case when the d...