Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a simple mean reverting diffusion process, with piecewise constant drift and diffusion coefficients, discontinuous at a fixed threshold. We discuss estimation of drift and diffusion para...

We provide a short-time large deviation principle (LDP) for stochastic volatility models, where the volatility is expressed as a function of a Volterra process. This LDP does not require strict self...

Several asymptotic results for the implied volatility generated by a rough volatility model have been obtained in recent years (notably in the small-maturity regime), providing a better understandin...

Least squares Monte Carlo methods are a popular numerical approximation method for solving stochastic control problems. Based on dynamic programming, their key feature is the approximation of the co...

In [Precise Asymptotics for Robust Stochastic Volatility Models; Ann. Appl. Probab. 2021] we introduce a new methodology to analyze large classes of (classical and rough) stochastic volatility model...

We refer by threshold Ornstein-Uhlenbeck to a continuous-time threshold autoregressive process. It follows the Ornstein-Uhlenbeck dynamics when above or below a fixed level, yet at this level (thres...

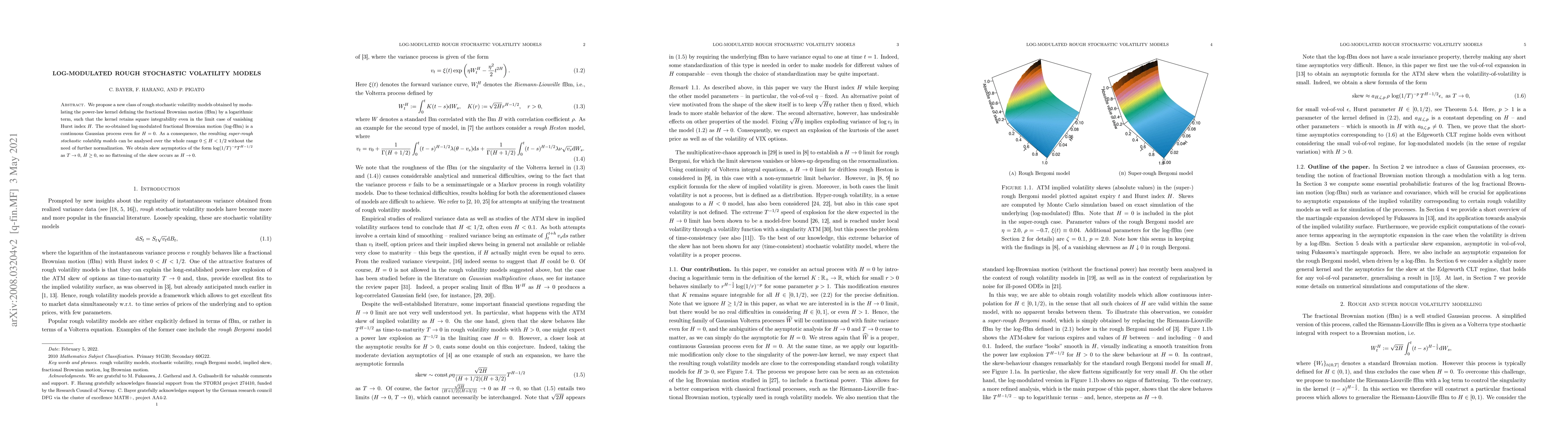

We propose a new class of rough stochastic volatility models obtained by modulating the power-law kernel defining the fractional Brownian motion (fBm) by a logarithmic term, such that the kernel ret...

In this paper we study randomized optimal stopping problems and consider corresponding forward and backward Monte Carlo based optimisation algorithms. In particular we prove the convergence of the p...

We present a new methodology to analyze large classes of (classical and rough) stochastic volatility models, with special regard to short-time and small noise formulae for option prices. Our main to...

We study the maximum likelihood estimator of the drift parameters of a stochastic differential equation, with both drift and diffusion coefficients constant on the positive and negative axis, yet di...

Starting from the notion of multivariate fractional Brownian Motion introduced in [F. Lavancier, A. Philippe, and D. Surgailis. Covariance function of vector self-similar processes. Statistics & Proba...

Motivated by empirical evidence from the joint behavior of realized volatility time series, we propose to model the joint dynamics of log-volatilities using a multivariate fractional Ornstein-Uhlenbec...

We consider a tick-by-tick model of price formation, in which buy and sell orders are modeled as self-exciting point processes (Hawkes process), similar to the one in [El Euch, Fukasawa, Rosenbaum, Th...