Academic Profile

Statistics

Similar Authors

Papers on arXiv

The price clustering phenomenon manifesting itself as an increased occurrence of specific prices is widely observed and well-documented for various financial instruments and markets. In the literatu...

We investigate the computational issues related to the memory size in the estimation of quadratic covariation, taking into account the specifics of financial ultra-high-frequency data. In multivaria...

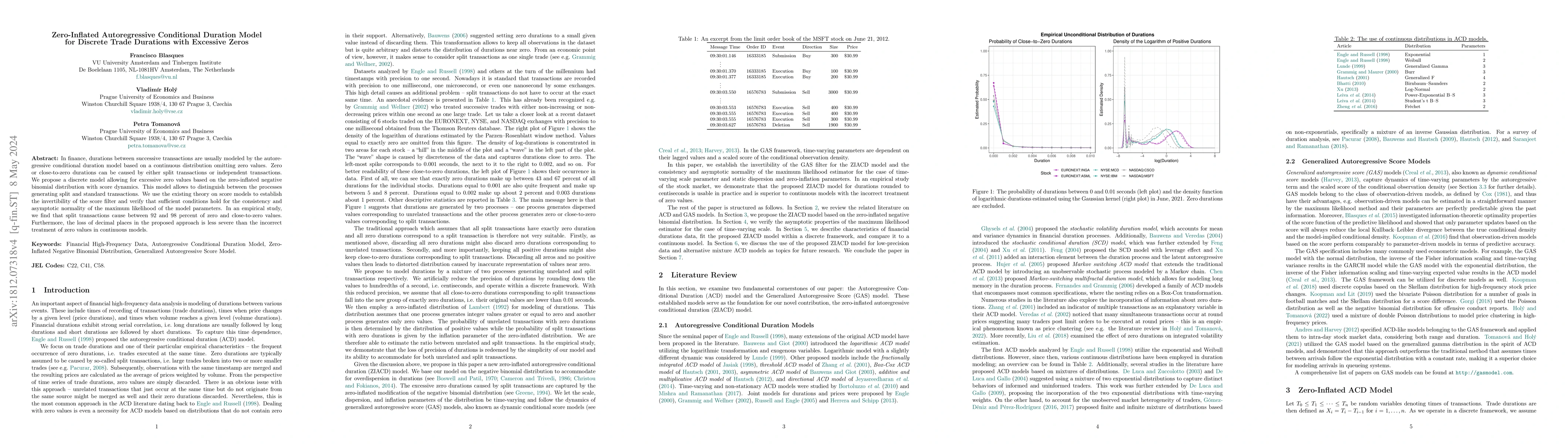

In finance, durations between successive transactions are usually modeled by the autoregressive conditional duration model based on a continuous distribution omitting zero values. Zero or close-to-z...

When stock prices are observed at high frequencies, more information can be utilized in estimation of parameters of the price process. However, high-frequency data are contaminated by the market mic...