Academic Profile

Statistics

Similar Authors

Papers on arXiv

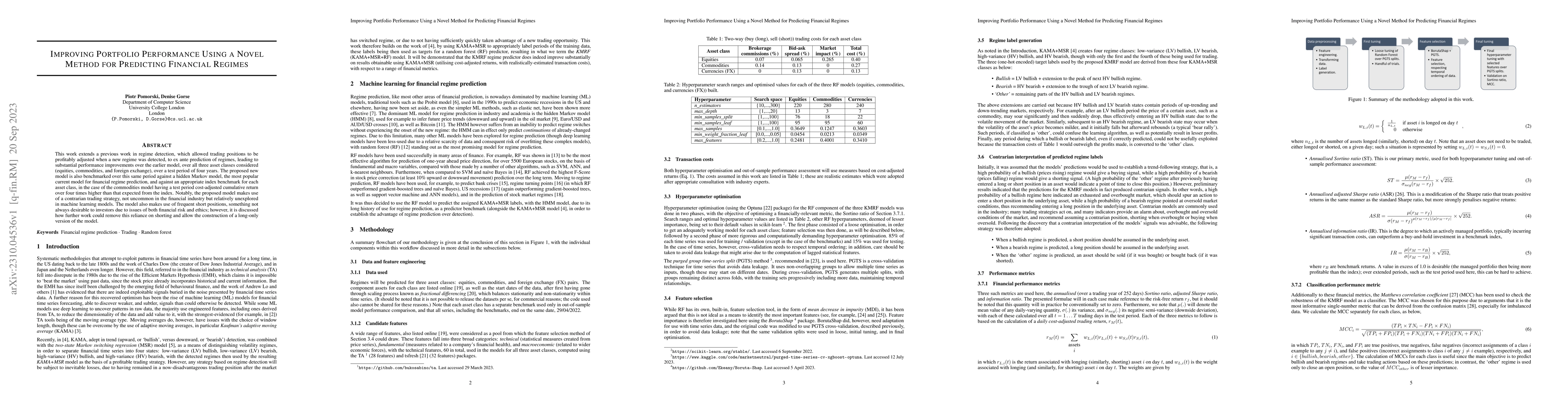

This work extends a previous work in regime detection, which allowed trading positions to be profitably adjusted when a new regime was detected, to ex ante prediction of regimes, leading to substant...

Regime-switching poses both problems and opportunities for portfolio managers. If a switch in the behaviour of the markets is not quickly detected it can be a source of loss, since previous trading ...

Regime detection is vital for the effective operation of trading and investment strategies. However, the most popular means of doing this, the two-state Markov-switching regression model (MSR), is n...