Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we present a probabilistic numerical algorithm combining dynamic programming, Monte Carlo simulations and local basis regressions to solve non-stationary optimal multiple switching pr...

We study a nonzero-sum stochastic differential game with both players adopting impulse controls, on a finite time horizon. The objective of each player is to maximize her total expected discounted p...

We propose a model where a producer and a consumer can affect the price dynamics of some commodity controlling drift and volatility of, respectively, the production rate and the consumption rate. We...

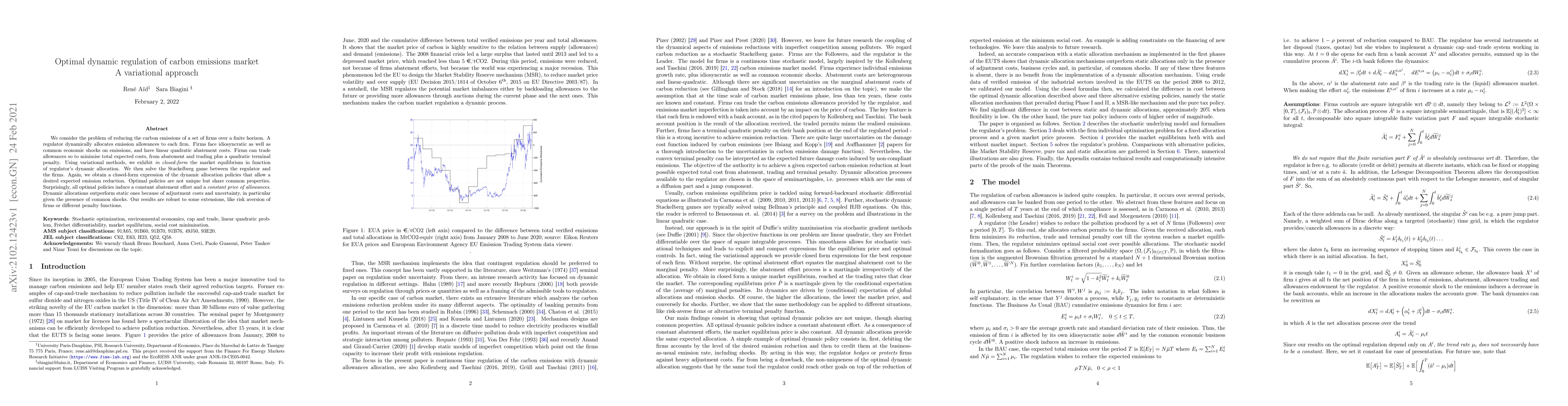

We consider the problem of reducing the carbon emissions of a set of firms over a finite horizon. A regulator dynamically allocates emission allowances to each firm. Firms face idiosyncratic as well...

We study a new kind of non-zero-sum stochastic differential game with mixed impulse/switching controls, motivated by strategic competition in commodity markets. A representative upstream firm produc...

We develop a model for the industry dynamics in the electricity market, based on mean-field games of optimal stopping. In our model, there are two types of agents: the renewable producers and the co...

We design three continuous--time models in finite horizon of a commodity price, whose dynamics can be affected by the actions of a representative risk--neutral producer and a representative risk--ne...

This work presents a novel policy iteration algorithm to tackle nonzero-sum stochastic impulse games arising naturally in many applications. Despite the obvious impact of solving such problems, ther...

We frame dynamic persuasion in a partial observation stochastic control Leader-Follower game with an ergodic criterion. The Receiver controls the dynamics of a multidimensional unobserved state proces...

We provide a theoretical framework to examine how carbon pricing policies influence inflation and to estimate the policy-driven impact on goods prices from achieving net-zero emissions. Firms control ...

We develop a continuous-time model of incentives for carbon emissive firms to exit the market based on a compensation payment identical to all firms. In our model, firms enjoy profits from production ...

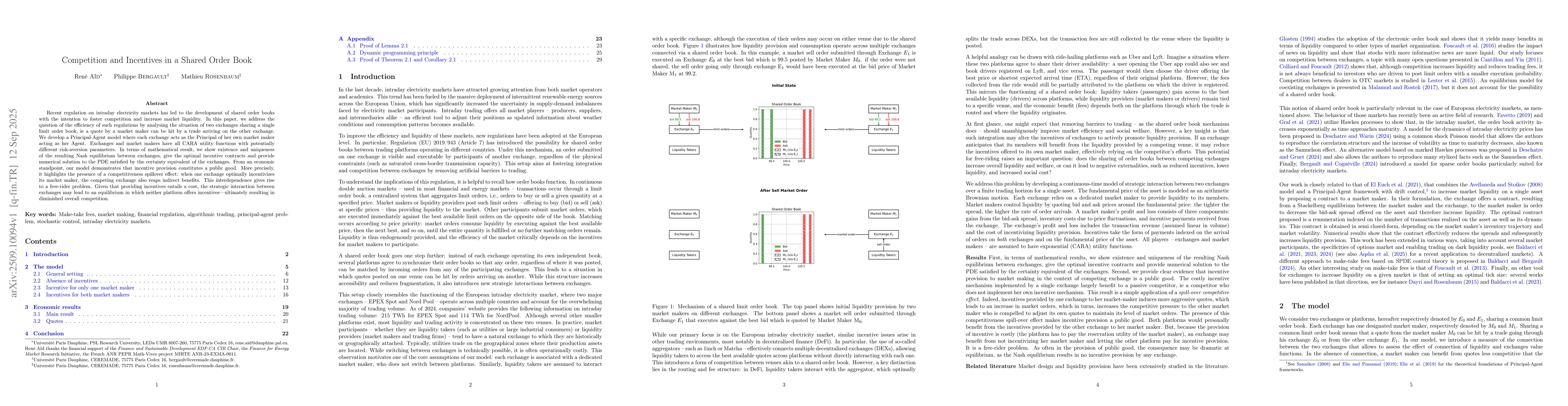

Recent regulation on intraday electricity markets has led to the development of shared order books with the intention to foster competition and increase market liquidity. In this paper, we address the...

We study how forward hedging reshapes incentive provision inside the firm. We consider a risk-averse producer facing demand and production risk that can either operate in-house or delegate production ...