Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a self-convolutive recurrence whose solution is the sequence of coefficients in the asymptotic expansion of the logarithmic derivative of the confluent hypergeometic function $U(a,b,z)$....

We give a new improvement over Newton's method for root-finding, when the function in question is doubly differentiable. It generally exhibits faster and more reliable convergence. It can be also be...

We show how to derive the Black-Scholes model and its generalisation to the `exchange-option' (to exchange one asset for another) via the continuum limit of the Binomial tree. No knowledge of stocha...

The notion of a credit spread curve is fundamental in fixed income investing, but in practice it is not `given' and needs to be constructed from bond prices either for a particular issuer, or for a ...

An analysis is presented of a Brownian particle moving on the half-line, subject to a restoring force proportional to its displacement and an absorbing boundary at the origin. When the initial displ...

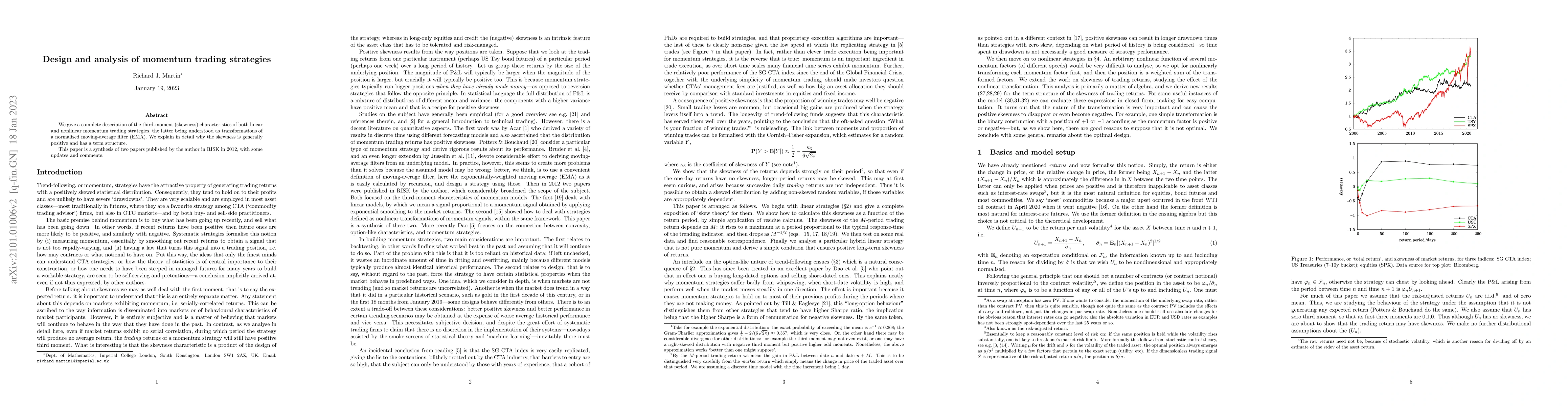

We give a complete description of the third-moment (skewness) characteristics of both linear and nonlinear momentum trading strategies, the latter being understood as transformations of a normalised...

Markovian credit migration models are a reasonably standard tool nowadays, but there are fundamental difficulties with calibrating them. We show how these are resolved using a simplified form of mat...

We address the modelling of commodities that are supposed to have positive price but, on account of a possible failure in the physical delivery mechanism, may turn out not to. This is done by explic...

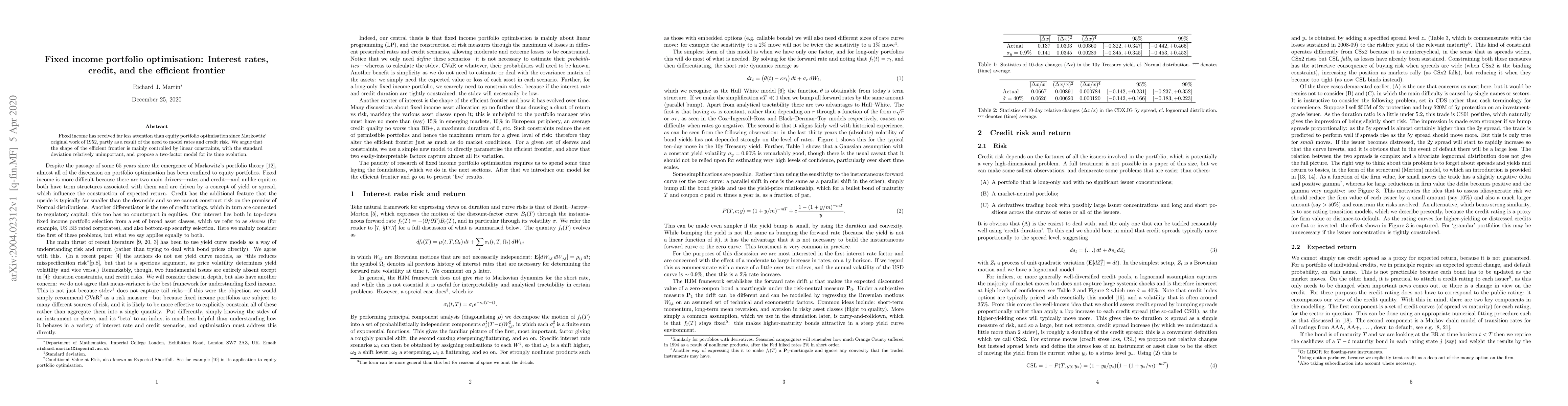

Fixed income has received far less attention than equity portfolio optimisation since Markowitz' original work of 1952, partly as a result of the need to model rates and credit risk. We argue that t...

Motivated by recent studies of record statistics in relation to strongly correlated time series, we consider explicitly the drawdown time of a Levy process, which is defined as the time since it las...