Academic Profile

Statistics

Similar Authors

Papers on arXiv

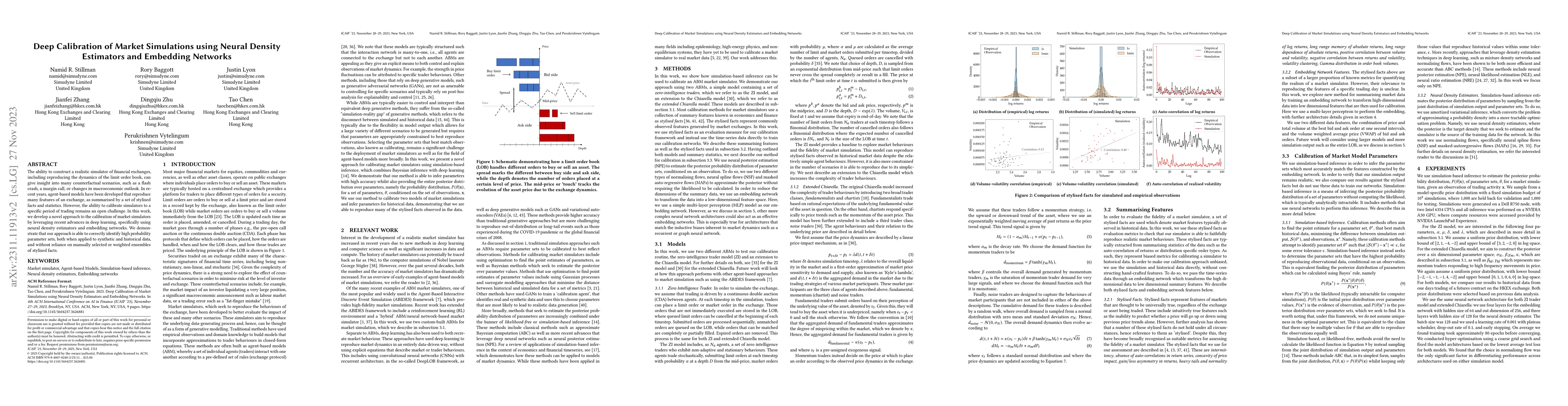

The ability to construct a realistic simulator of financial exchanges, including reproducing the dynamics of the limit order book, can give insight into many counterfactual scenarios, such as a flas...

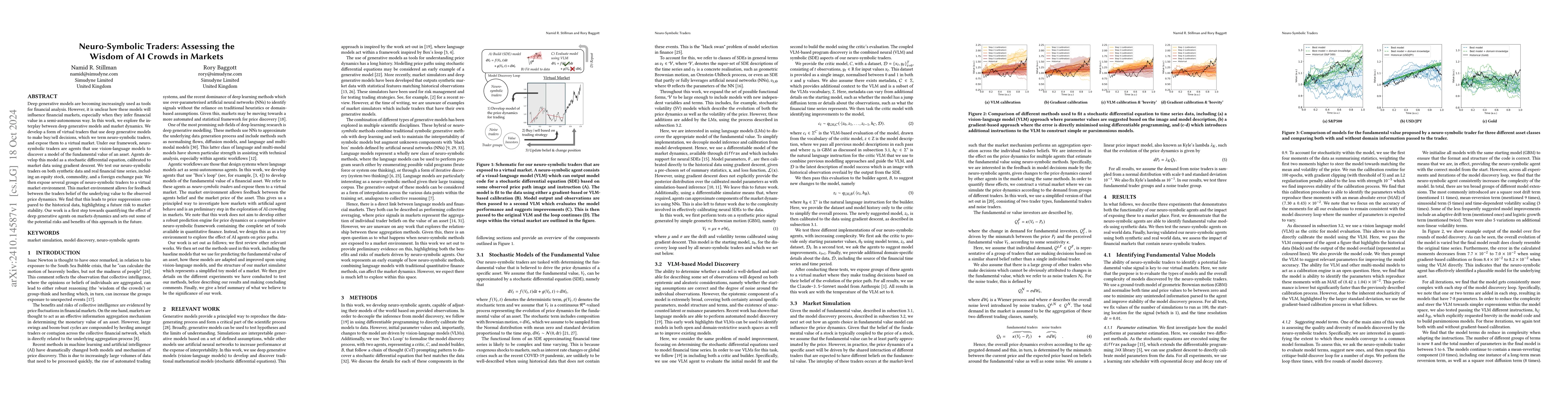

Deep generative models are becoming increasingly used as tools for financial analysis. However, it is unclear how these models will influence financial markets, especially when they infer financial va...

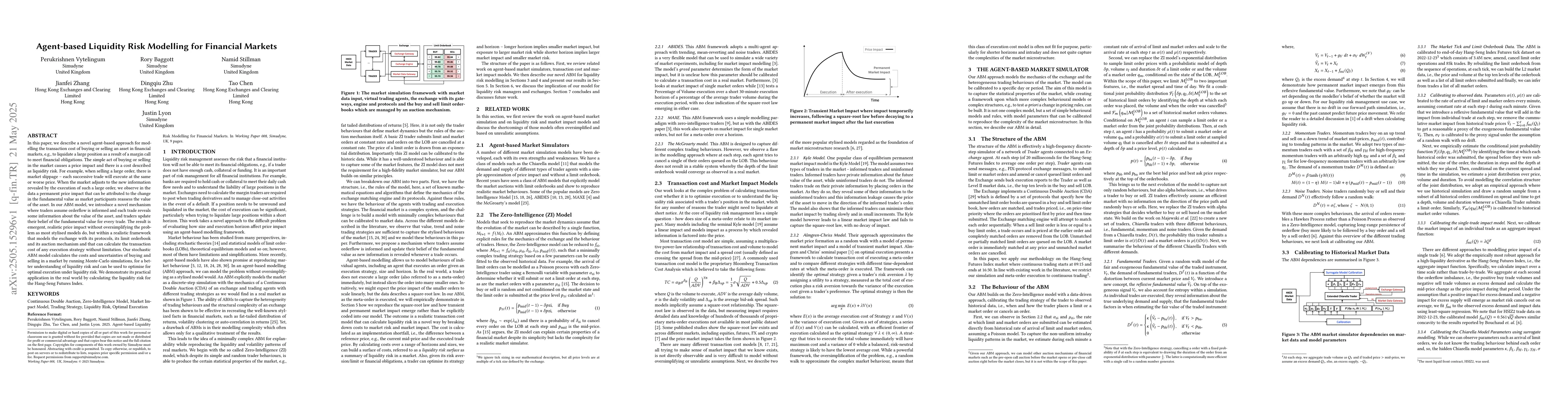

In this paper, we describe a novel agent-based approach for modelling the transaction cost of buying or selling an asset in financial markets, e.g., to liquidate a large position as a result of a marg...

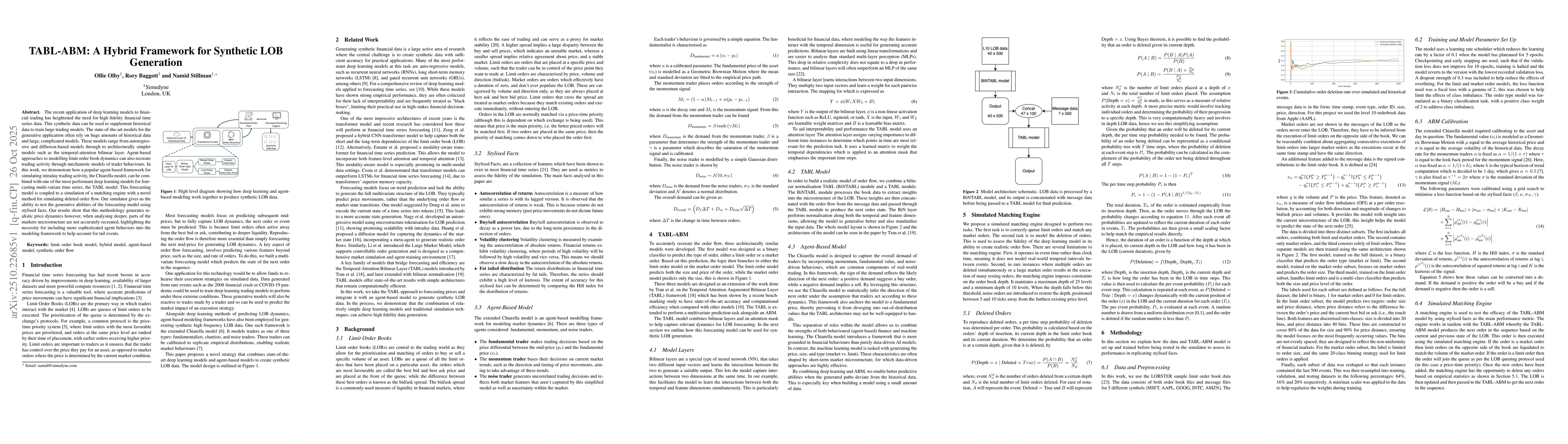

The recent application of deep learning models to financial trading has heightened the need for high fidelity financial time series data. This synthetic data can be used to supplement historical data ...

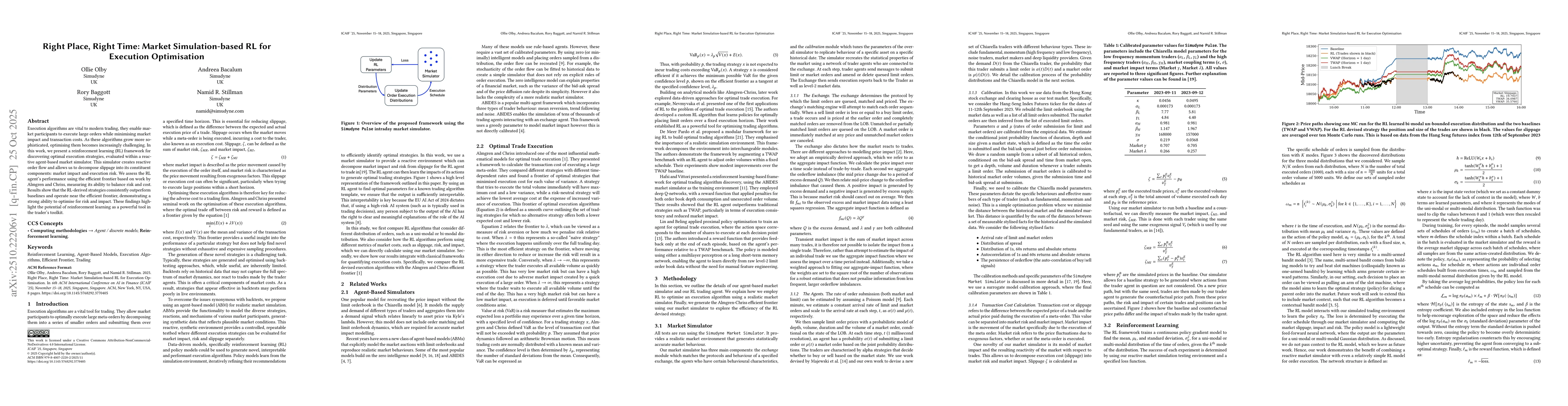

Execution algorithms are vital to modern trading, they enable market participants to execute large orders while minimising market impact and transaction costs. As these algorithms grow more sophistica...