Academic Profile

Statistics

Similar Authors

Papers on arXiv

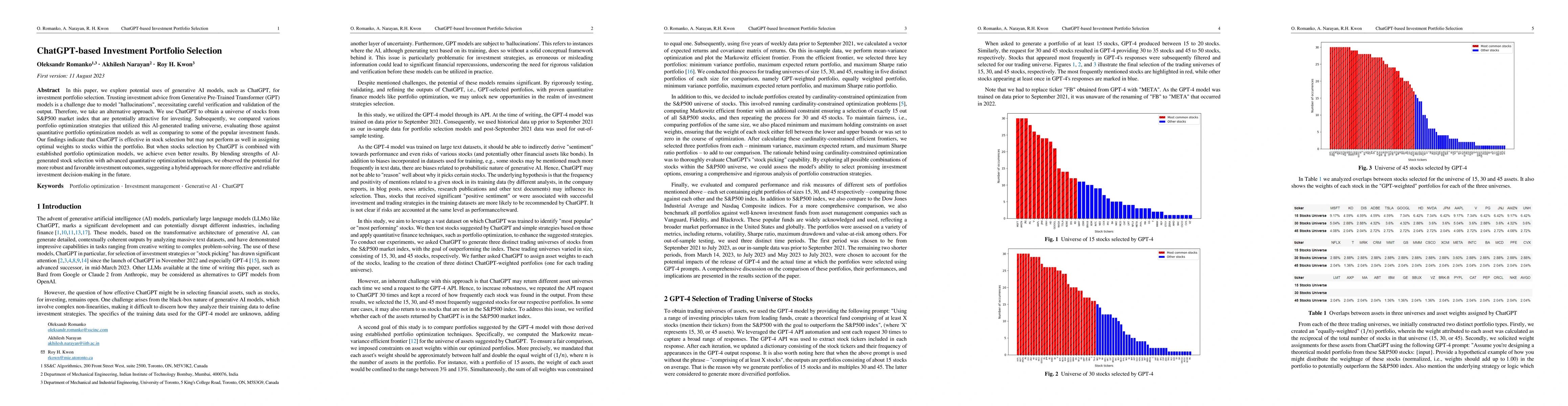

In this paper, we explore potential uses of generative AI models, such as ChatGPT, for investment portfolio selection. Trusting investment advice from Generative Pre-Trained Transformer (GPT) models...

Prediction models are typically optimized independently from decision optimization. A smart predict then optimize (SPO) framework optimizes prediction models to minimize downstream decision regret. ...

Mean-variance optimization (MVO) is known to be sensitive to estimation error in its inputs. Norm penalization of MVO programs is a regularization technique that can mitigate the adverse effects of ...

We propose a distributionally robust formulation of the traditional risk parity portfolio optimization problem. Distributional robustness is introduced by targeting the discrete probabilities attach...

Prediction models are traditionally optimized independently from their use in the asset allocation decision-making process. We address this shortcoming and present a framework for integrating regres...

Two-stage stochastic programs (2SPs) are important tools for making decisions under uncertainty. Decision-makers use contextual information to generate a set of scenarios to represent the true conditi...

This paper investigates how Large Language Models (LLMs) from leading providers (OpenAI, Google, Anthropic, DeepSeek, and xAI) can be applied to quantitative sector-based portfolio construction. We us...