2

arXiv Papers

5

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

5

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Liquidity takers behavior representation through a contrastive learning

approach

Thanks to the access to the labeled orders on the CAC40 data from Euronext, we are able to analyze agents' behaviors in the market based on their placed orders. In this study, we construct a self-su...

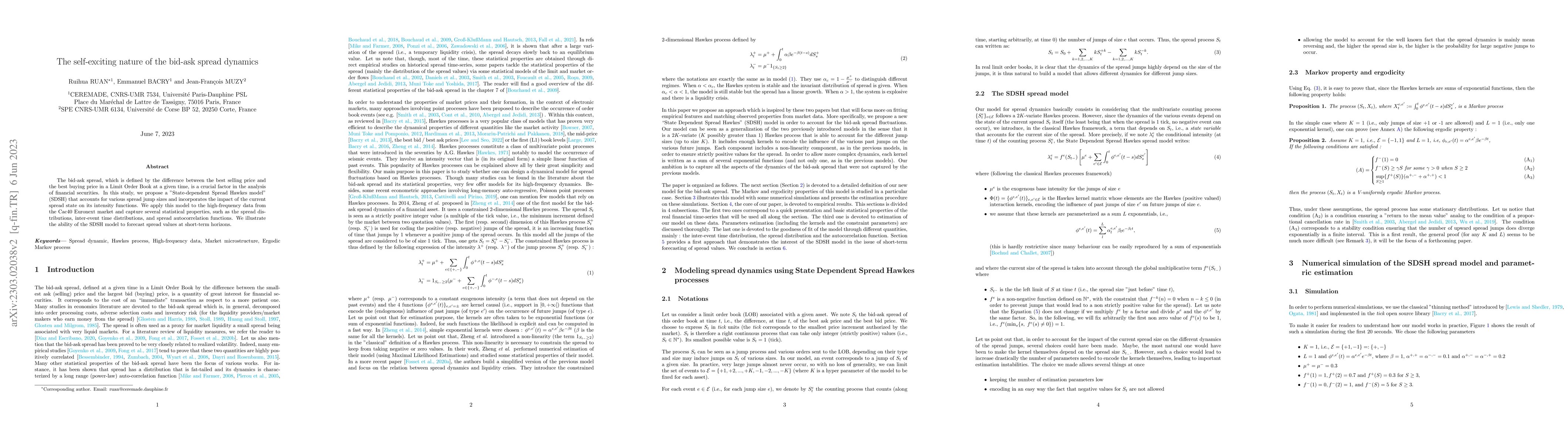

arXiv

The self-exciting nature of the bid-ask spread dynamics

The bid-ask spread, which is defined by the difference between the best selling price and the best buying price in a Limit Order Book at a given time, is a crucial factor in the analysis of financia...