Academic Profile

Statistics

Similar Authors

Papers on arXiv

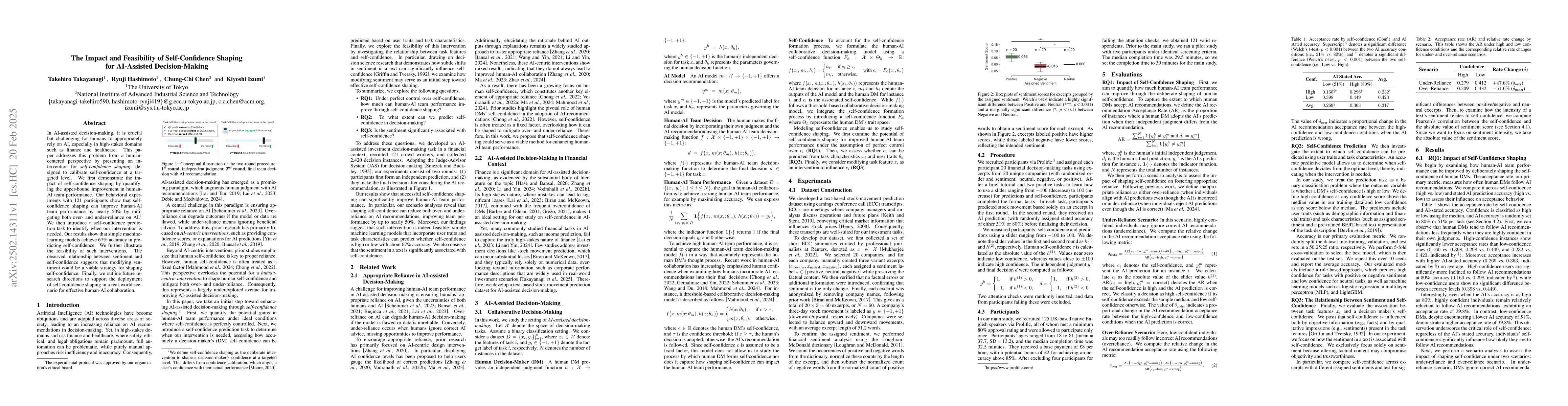

In AI-assisted decision-making, it is crucial but challenging for humans to appropriately rely on AI, especially in high-stakes domains such as finance and healthcare. This paper addresses this proble...

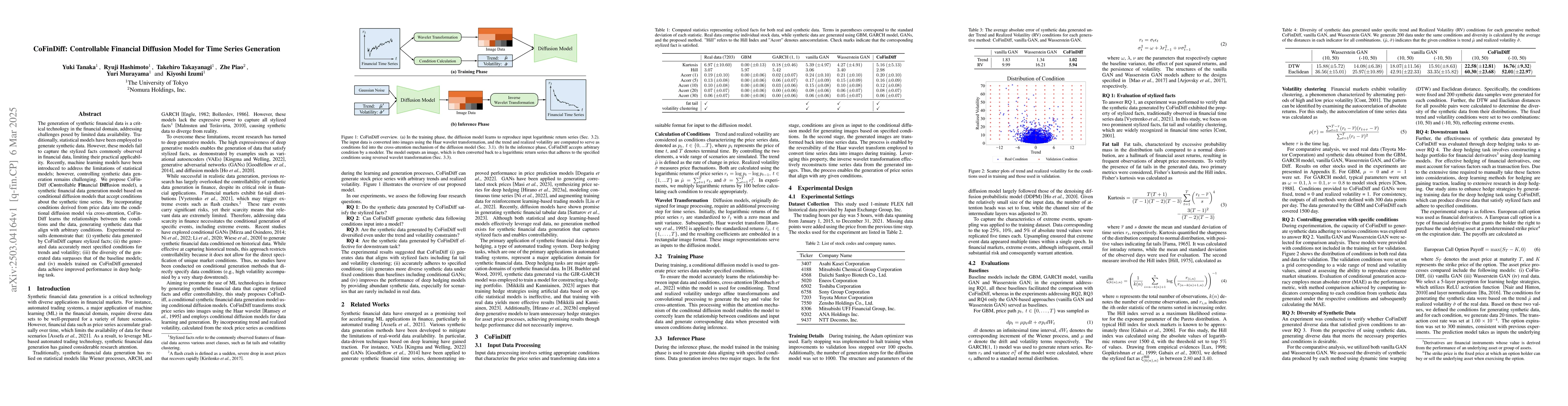

The generation of synthetic financial data is a critical technology in the financial domain, addressing challenges posed by limited data availability. Traditionally, statistical models have been emplo...

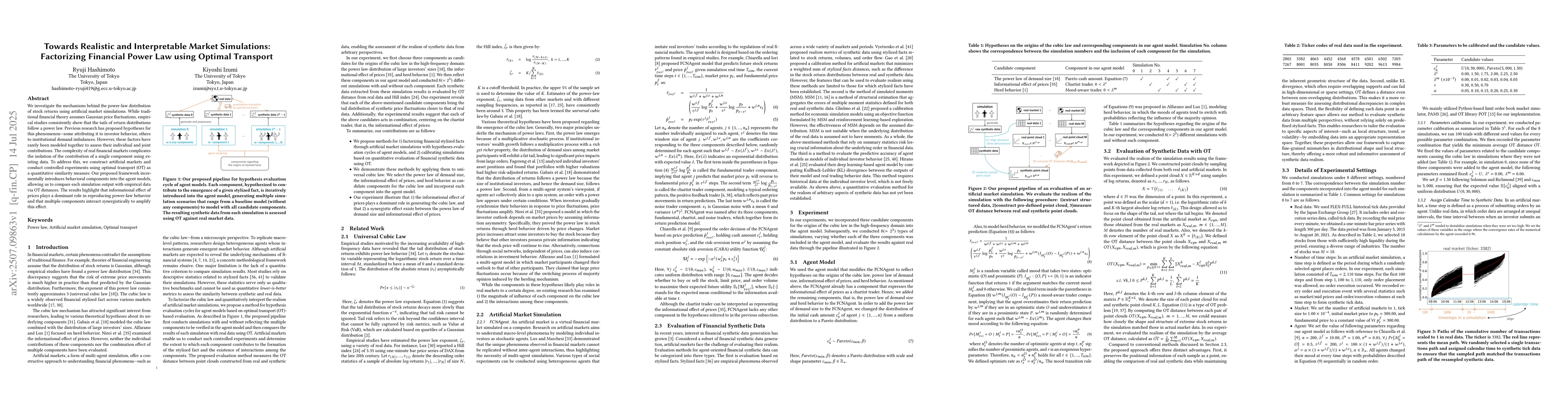

We investigate the mechanisms behind the power-law distribution of stock returns using artificial market simulations. While traditional financial theory assumes Gaussian price fluctuations, empirical ...

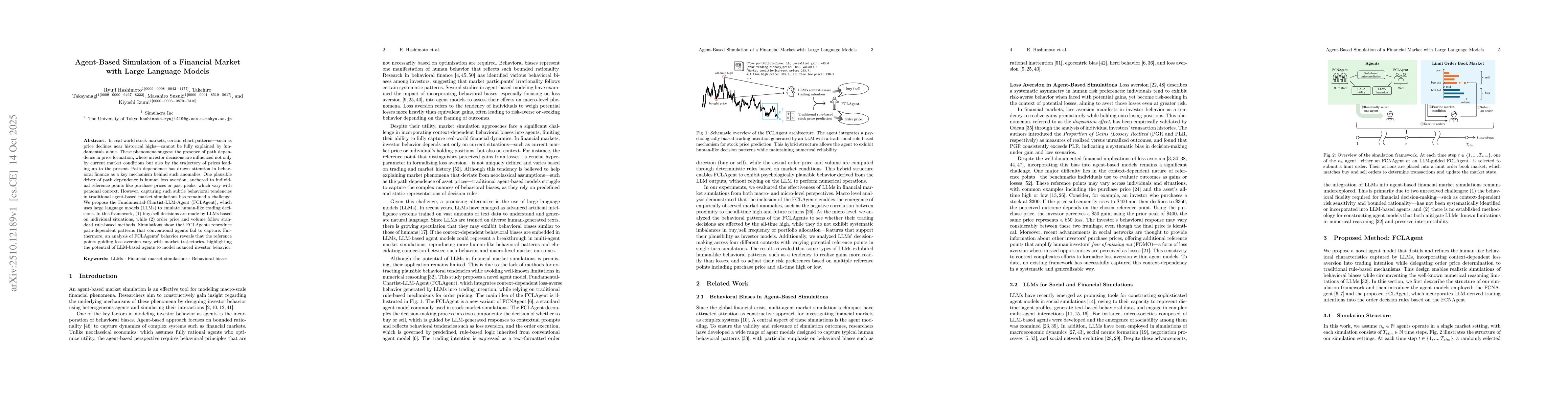

In real-world stock markets, certain chart patterns -- such as price declines near historical highs -- cannot be fully explained by fundamentals alone. These phenomena suggest the presence of path dep...

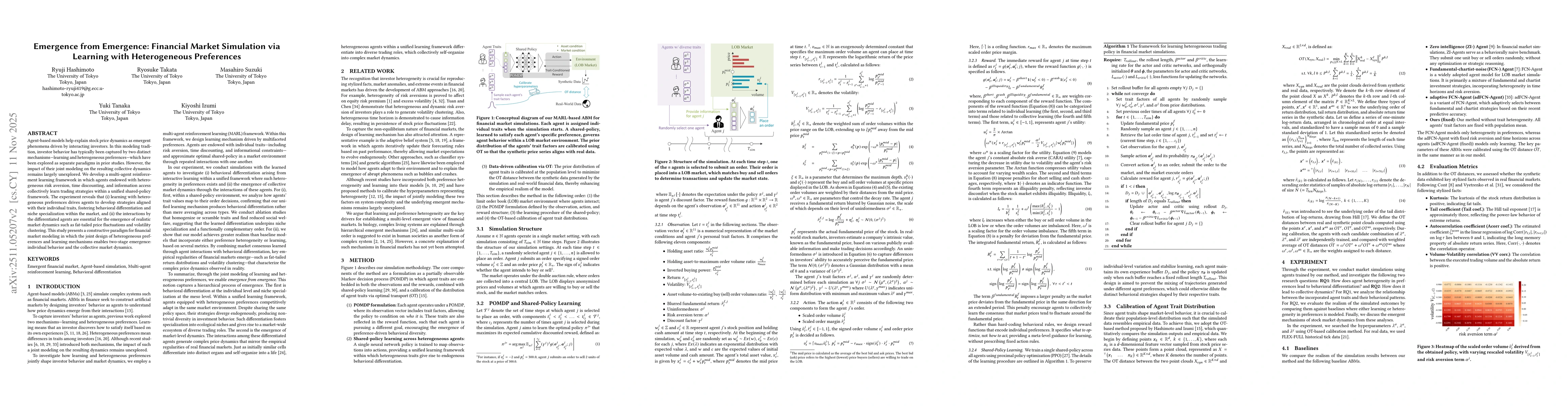

Agent-based models help explain stock price dynamics as emergent phenomena driven by interacting investors. In this modeling tradition, investor behavior has typically been captured by two distinct me...

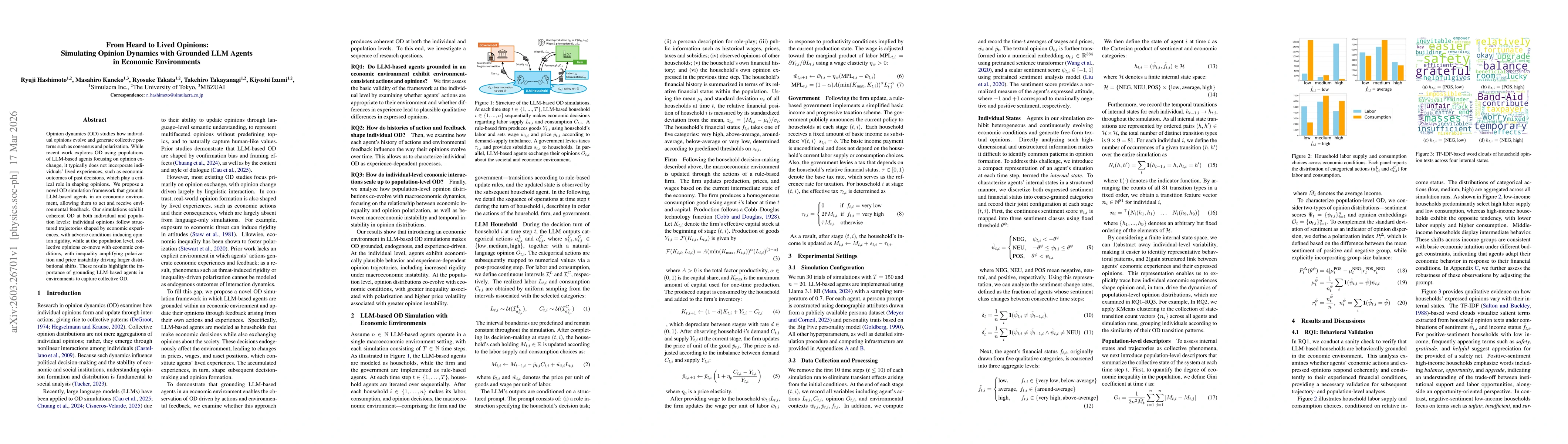

Opinion dynamics (OD) studies how individual opinions evolve and generate collective patterns such as consensus and polarization. While recent work explores OD using populations of LLM-based agents fo...

Agent-based models provide a constructive approach to studying emergent dynamics in life-like systems composed of interacting, adaptive agents. Financial markets serve as a canonical example of such s...

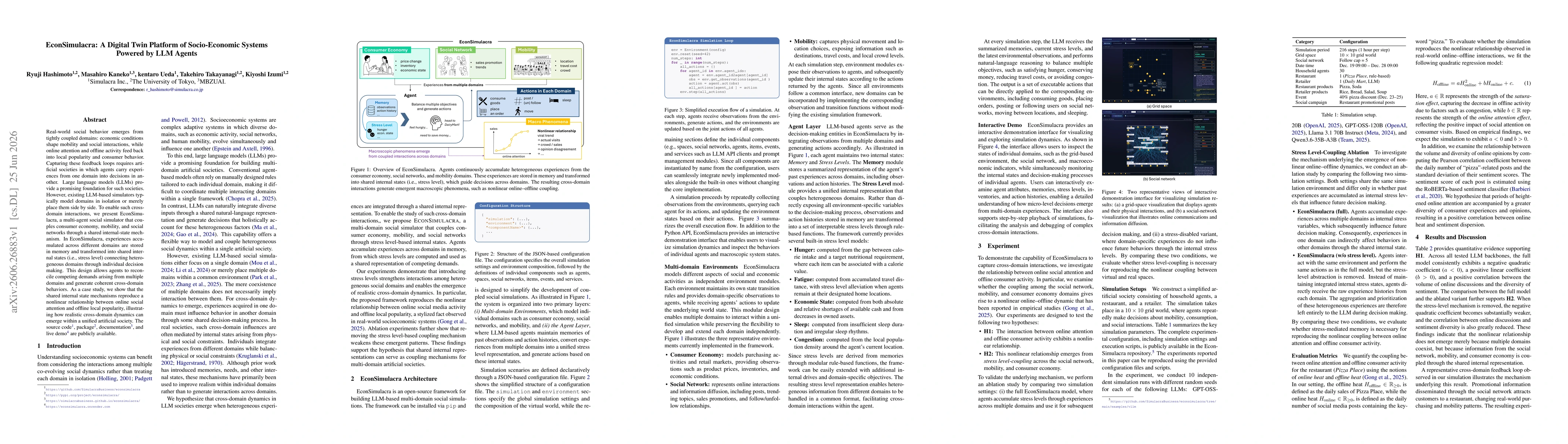

Real-world social behavior emerges from tightly coupled domains: economic conditions shape mobility and social interactions, while online attention and offline activity feed back into local popularity...