Academic Profile

Statistics

Similar Authors

Papers on arXiv

We tackle the problem of estimating risk measures of the infinite-horizon discounted cost within a Markov cost process. The risk measures we study include variance, Value-at-Risk (VaR), and Conditio...

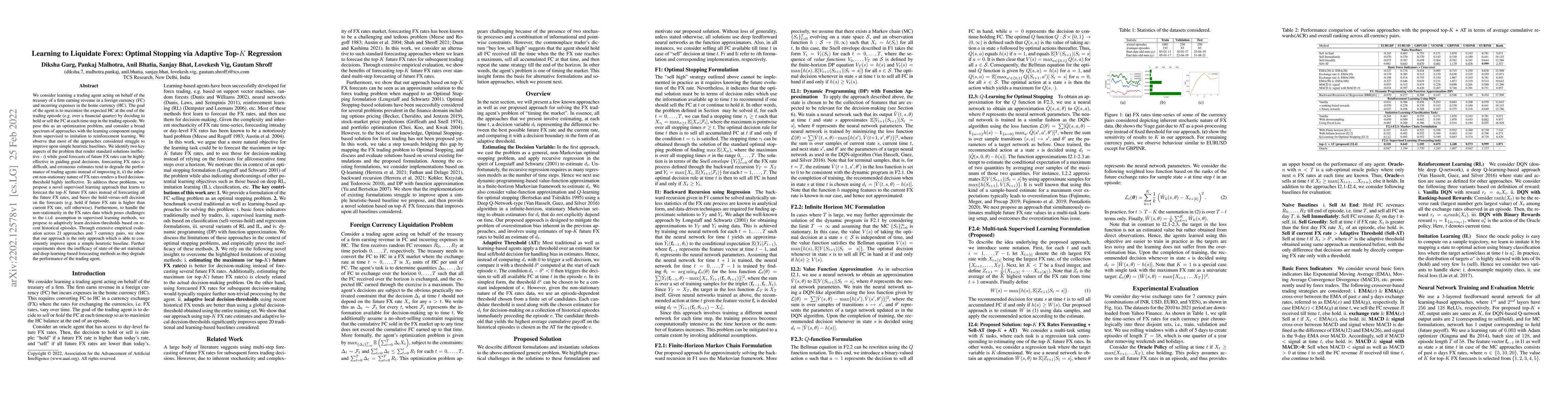

We consider learning a trading agent acting on behalf of the treasury of a firm earning revenue in a foreign currency (FC) and incurring expenses in the home currency (HC). The goal of the agent is ...

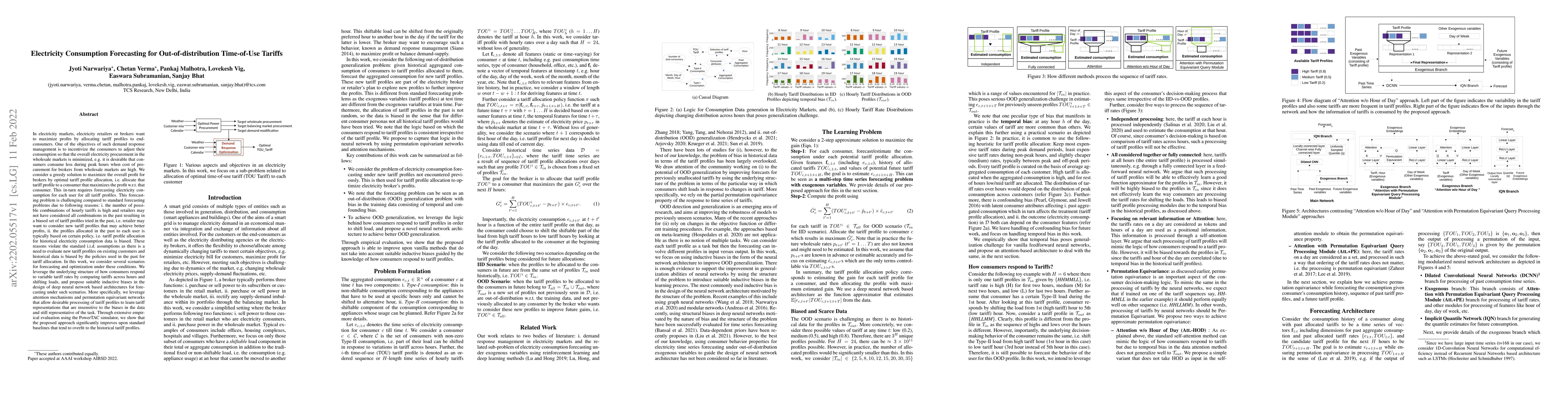

In electricity markets, retailers or brokers want to maximize profits by allocating tariff profiles to end consumers. One of the objectives of such demand response management is to incentivize the c...

Periodic double auctions (PDA) have applications in many areas such as in e-commerce, intra-day equity markets, and day-ahead energy markets in smart-grids. While the trades accomplished using PDAs ...

Reinforcement learning (RL) for exponential-utility optimization in discounted Markov decision processes (MDPs) lacks principled value-based algorithms. We address this gap in the fixed risk-aversion ...