Academic Profile

Statistics

Similar Authors

Papers on arXiv

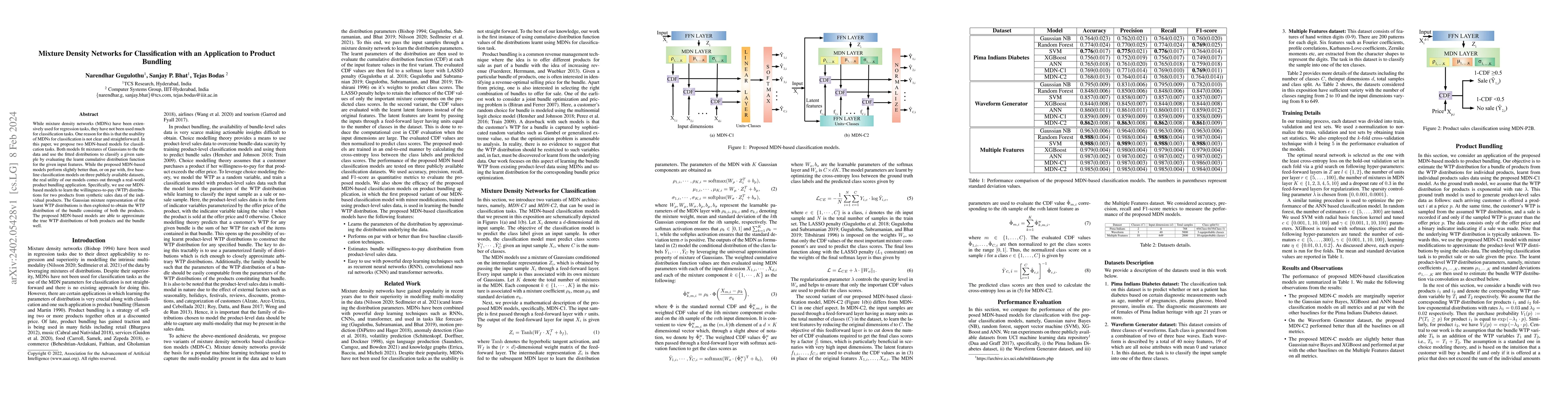

While mixture density networks (MDNs) have been extensively used for regression tasks, they have not been used much for classification tasks. One reason for this is that the usability of MDNs for cl...

We consider the problems of estimation and optimization of utility-based shortfall risk (UBSR), which is a popular risk measure in finance. In the context of UBSR estimation, we derive a non-asympto...

We consider the problem of estimating a spectral risk measure (SRM) from i.i.d. samples, and propose a novel method that is based on numerical integration. We show that our SRM estimate concentrates...

This paper presents a unified approach based on Wasserstein distance to derive concentration bounds for empirical estimates for two broad classes of risk measures defined in the paper. The classes o...

We consider the problems of estimation and optimization of two popular convex risk measures: utility-based shortfall risk (UBSR) and Optimized Certainty Equivalent (OCE) risk. We extend these risk mea...

We propose risk-sensitive reinforcement learning algorithms catering to three families of risk measures, namely expectiles, utility-based shortfall risk and optimized certainty equivalent risk. For ea...