Academic Profile

Statistics

Similar Authors

Papers on arXiv

We employ scoring functions, used in statistics for eliciting risk functionals, as cost functions in the Monge-Kantorovich (MK) optimal transport problem. This gives raise to a rich variety of novel...

Differential sensitivity measures provide valuable tools for interpreting complex computational models used in applications ranging from simulation to algorithmic prediction. Taking the derivative o...

We introduce a framework for quantifying propagation of uncertainty arising in a dynamic setting. Specifically, we define dynamic uncertainty sets designed explicitly for discrete stochastic process...

We study a reinsurer who faces multiple sources of model uncertainty. The reinsurer offers contracts to $n$ insurers whose claims follow compound Poisson processes representing both idiosyncratic an...

We define and develop an approach for risk budgeting allocation -- a risk diversification portfolio strategy -- where risk is measured using a dynamic time-consistent risk measure. For this, we intr...

Risk budgeting is a portfolio strategy where each asset contributes a prespecified amount to the aggregate risk of the portfolio. In this work, we propose an efficient numerical framework that uses ...

Stress testing, and in particular, reverse stress testing, is a prominent exercise in risk management practice. Reverse stress testing, in contrast to (forward) stress testing, aims to find an alter...

The robustness of risk measures to changes in underlying loss distributions (distributional uncertainty) is of crucial importance in making well-informed decisions. In this paper, we quantify, for t...

We propose a holistic framework for constructing sensitivity measures for any elicitable functional $T$ of a response variable. The sensitivity measures, termed score-based sensitivities, are constr...

We consider the problem where a modeller conducts sensitivity analysis of a model consisting of random input factors, a corresponding random output of interest, and a baseline probability measure. T...

We consider the problem where an agent aims to combine the views and insights of different experts' models. Specifically, each expert proposes a diffusion process over a finite time horizon. The agent...

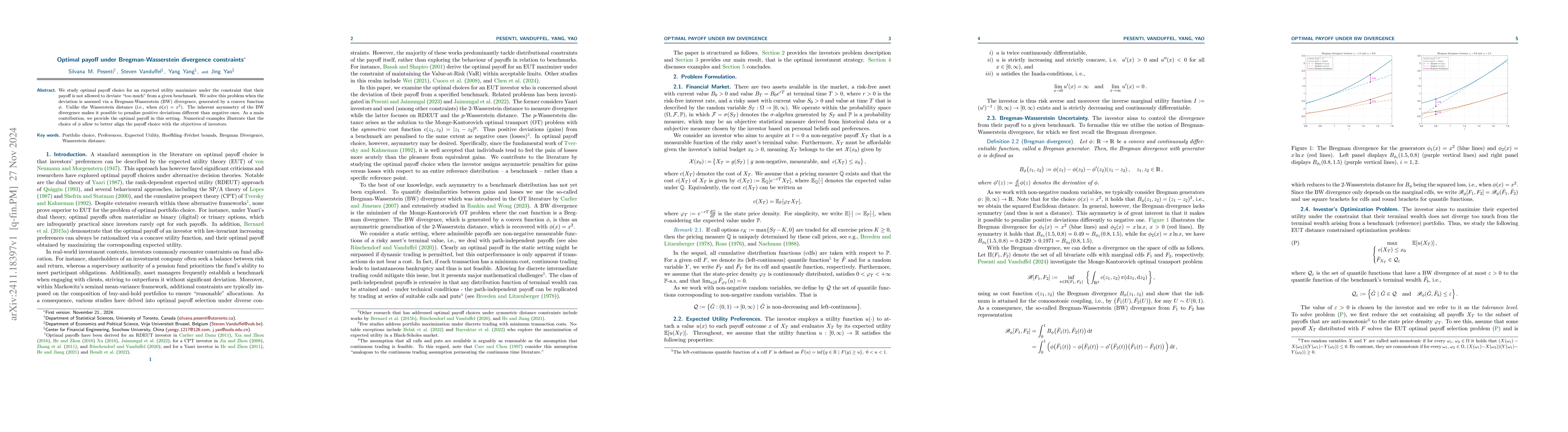

We study optimal payoff choice for an expected utility maximizer under the constraint that their payoff is not allowed to deviate ``too much'' from a given benchmark. We solve this problem when the de...

Elicitable functionals and (strict) consistent scoring functions are of interest due to their utility of determining (uniquely) optimal forecasts, and thus the ability to effectively backtest predicti...

We provide a constructive way of defining new elicitable risk measures that are characterised by a multiplicative scoring function. We show that depending on the choice of the scoring function's compo...

We study distributionally robust optimization (DRO) problems with uncertainty sets consisting of high dimensional random vectors that are close in the multivariate Wasserstein distance to a reference ...

We consider the problem of an agent who faces losses over a finite time horizon and may choose to share some of these losses with a counterparty. The agent is uncertain about the true loss distributio...

This paper introduces marginal fairness, a new individual fairness notion for equitable decision-making in the presence of protected attributes such as gender, race, and religion. This criterion ensur...

Risk assessment in casualty insurance, such as flood risk, traditionally relies on extreme-value methods that emphasizes rare events. These approaches are well-suited for characterizing tail risk, but...

We study a problem of optimal allocation in a discrete-time multi-period pure-exchange economy, where agents have preferences over stochastic endowment processes that are represented by strongly time-...

We consider the problem of active portfolio management, where an investor seeks the portfolio with maximal expected utility of the difference between the terminal wealth of their strategy and a propor...

We consider robust risk measures that arise as worst-case values of convex risk measures evaluated on uncertainty sets. We characterize continuity properties of robust risk measures through their cons...

In static risk measurement, law invariance expresses the principle that the risk of a position should depend only on its distribution, and not on the particular probability space on which it is repres...