Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies robust and distributionally robust optimization based on the extended $\varphi$-divergence under the Fundamental Risk Quadrangle framework. We present the primal and dual represen...

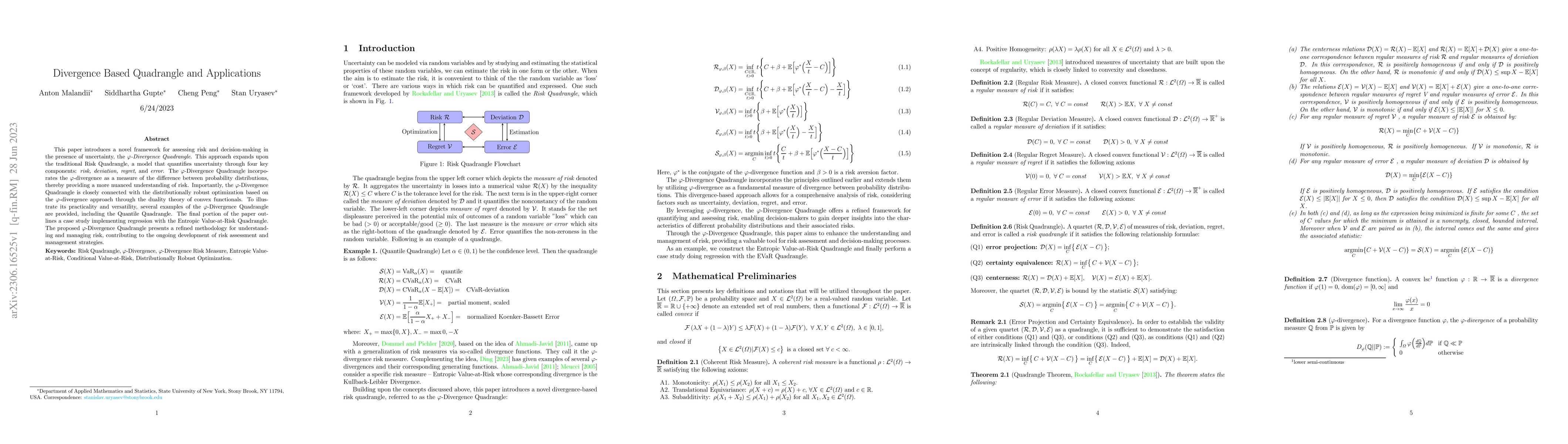

This paper introduces a novel framework for assessing risk and decision-making in the presence of uncertainty, the \emph{$\varphi$-Divergence Quadrangle}. This approach expands upon the traditional ...

The paper explores the concept of the \emph{expectile risk measure} within the framework of the Fundamental Risk Quadrangle (FRQ) theory. According to the FRQ theory, a quadrangle comprises four sto...

The paper considers the problem of modeling a univariate random variable. Main contributions: (i) Suggested a new family of distributions with quantile defined by a linear combination of some basis ...

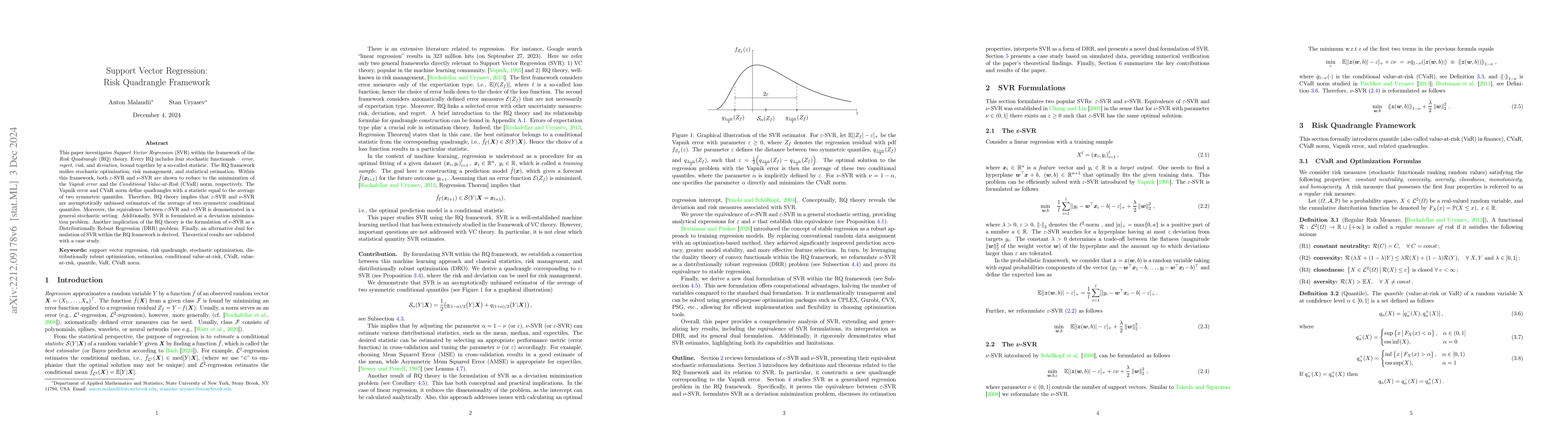

This paper investigates Support Vector Regression (SVR) in the context of the fundamental risk quadrangle theory, which links optimization, risk management, and statistical estimation. It is shown t...

This paper proves equivalences of portfolio optimization problems with negative expectile and omega ratio. We derive subgradients for the negative expectile as a function of the portfolio from a kno...

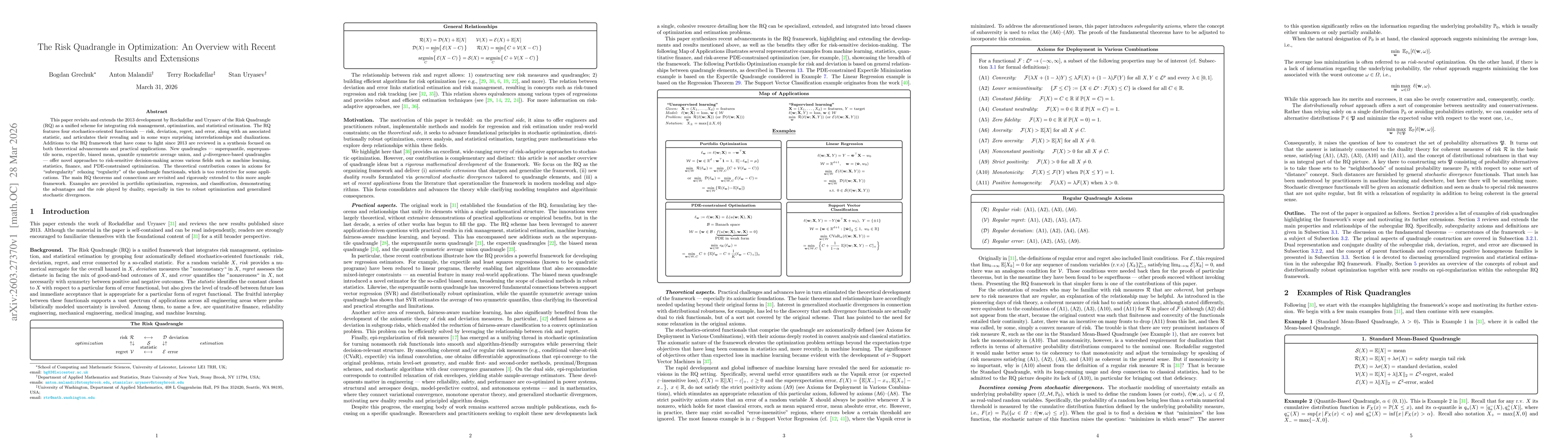

This paper revisits and extends the 2013 development by Rockafellar and Uryasev of the Risk Quadrangle (RQ) as a unified scheme for integrating risk management, optimization, and statistical estimatio...

This paper introduces \emph{biased mean regression}, estimating the \emph{biased mean}, i.e., $\mathbb{E}[Y] + x$, where $x \in \mathbb{R}$. The approach addresses a fundamental statistical problem th...

We present a novel method for solving conditional value-at-risk (CVaR) optimization problems based on the dual representation of CVaR, which is defined as the worst-case expectation over a risk envelo...