Academic Profile

Statistics

Similar Authors

Papers on arXiv

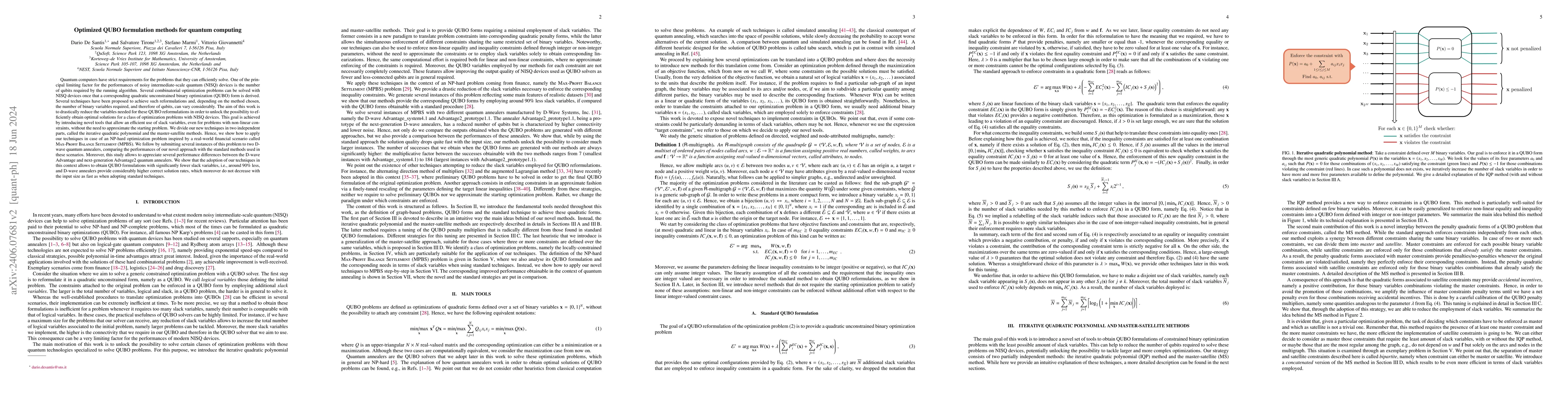

Several combinatorial optimization problems can be solved with NISQ devices once that a corresponding quadratic unconstrained binary optimization (QUBO) form is derived. The aim of this work is to d...

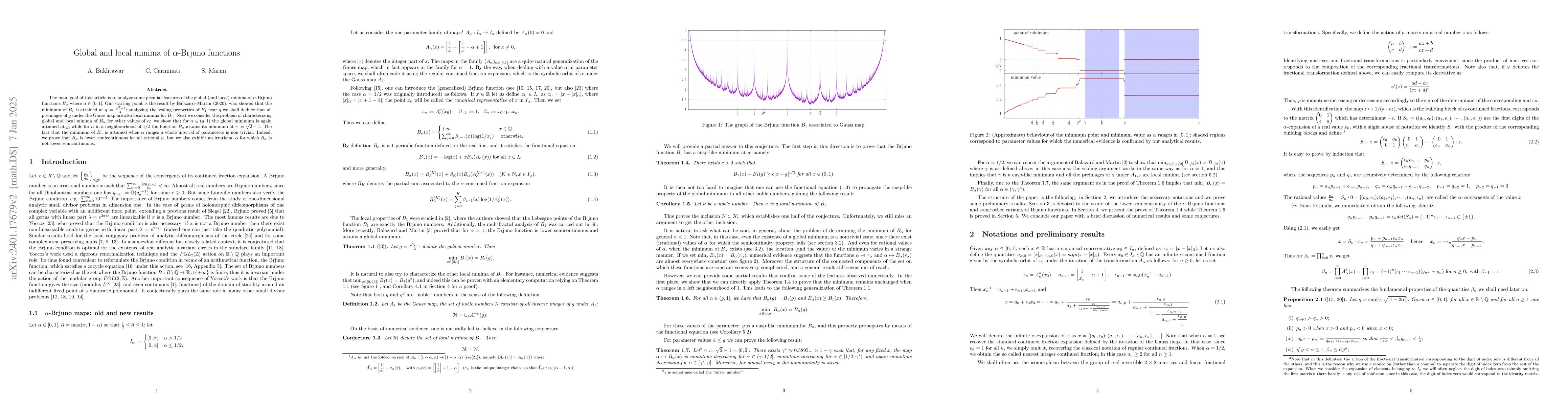

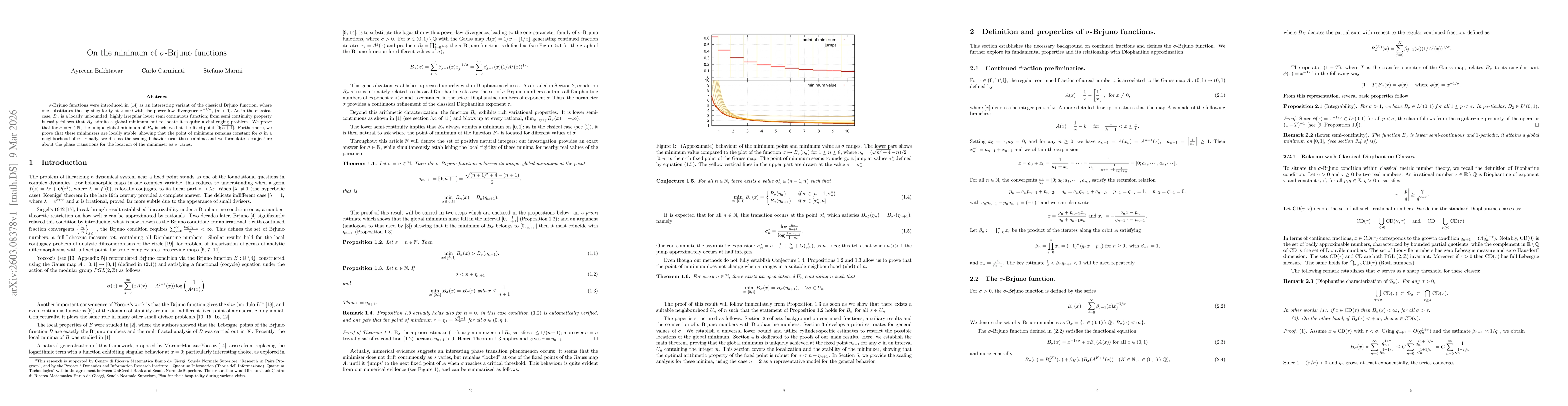

The aim of this article is to analyze some peculiar features of the global (and local) minima of $\alpha$-Brjuno functions $B_\alpha$ where $\alpha\in[\frac{1}{2},1].$ Our starting point is the resu...

We use the statistical properties of Shannon entropy estimator and Kullback-Leibler divergence to study the predictability of ultra-high frequency financial data. We develop a statistical test for t...

This paper investigates the degree of efficiency for the Moscow Stock Exchange. A market is called efficient if prices of its assets fully reflect all available information. We show that the degree ...

We study a random version of the population-market model proposed by Arlot, Marmi and Papini in Arlot et al. (2019). The latter model is based on the Yoccoz-Birkeland integral equation and describes...

We study the asymptotic normality of two feasible estimators of the integrated volatility of volatility based on the Fourier methodology, which does not require the pre-estimation of the spot volati...

The Brjuno function was introduced by Yoccoz to study the linearizability of holomorphic germs and other one-dimensional small divisor problems. The Brjuno functions associated with various continue...

We give an explicit arithmetical condition which guarantees the existence of the unstable manifold of the MacKay approximate renormalisation scheme for the breakup of invariant tori in one and a hal...

One considers a system on $\mathbb{C}^2$ close to an invariant curve which can be viewed as a generalization of the semi-standard map to a trigonometric polynomial with many Fourier modes. The radiu...

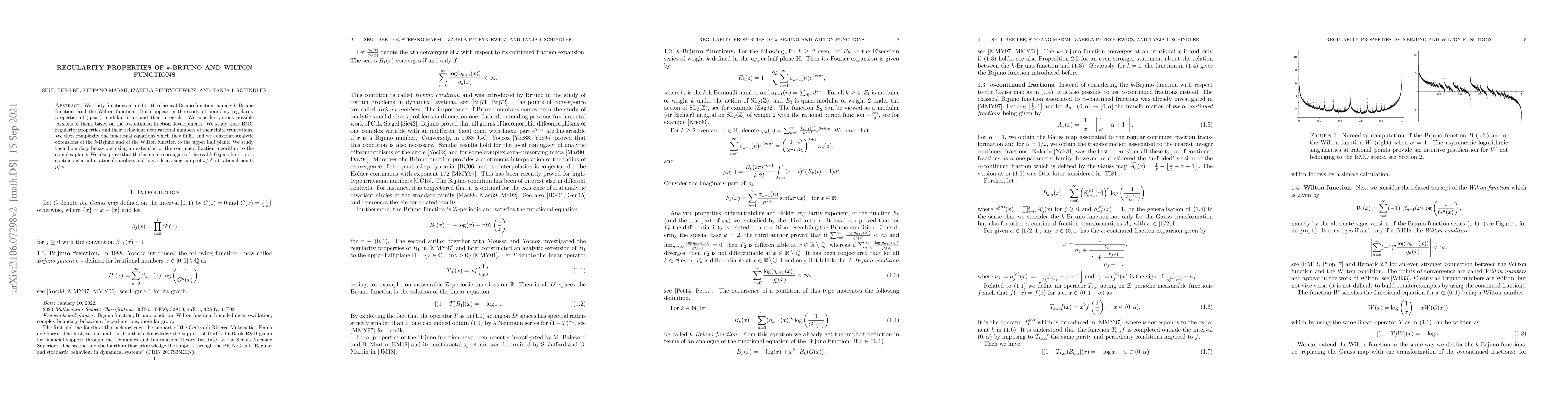

We study functions related to the classical Brjuno function, namely $k$-Brjuno functions and the Wilton function. Both appear in the study of boundary regularity properties of (quasi) modular forms ...

We prove that skew systems with a sufficiently expanding base have approximate exponential decay of correlations, meaning that the exponential rate is observed modulo an error. The fiber maps are on...

We consider a model of a simple financial system consisting of a leveraged investor that invests in a risky asset and manages risk by using Value-at-Risk (VaR). The VaR is estimated by using past da...

We consider the minimal average action (Mather's $\beta$ function) for area preserving twist maps of the annulus. The regularity properties of this function share interesting relations with the dyna...

The main purpose of this study is to introduce a semi-classical model describing betting scenarios in which, at variance with conventional approaches, the payoff of the gambler is encoded into the i...

In the current note we extend results by Marmi, Moussa and Yoccoz about cohomological equations for interval exchange transformations to irreducible linear involutions.

We propose a theory of unimodal maps perturbed by an heteroscedastic Markov chain noise and experiencing another heteroscedastic noise due to uncertain observation. We address and treat the filtering ...

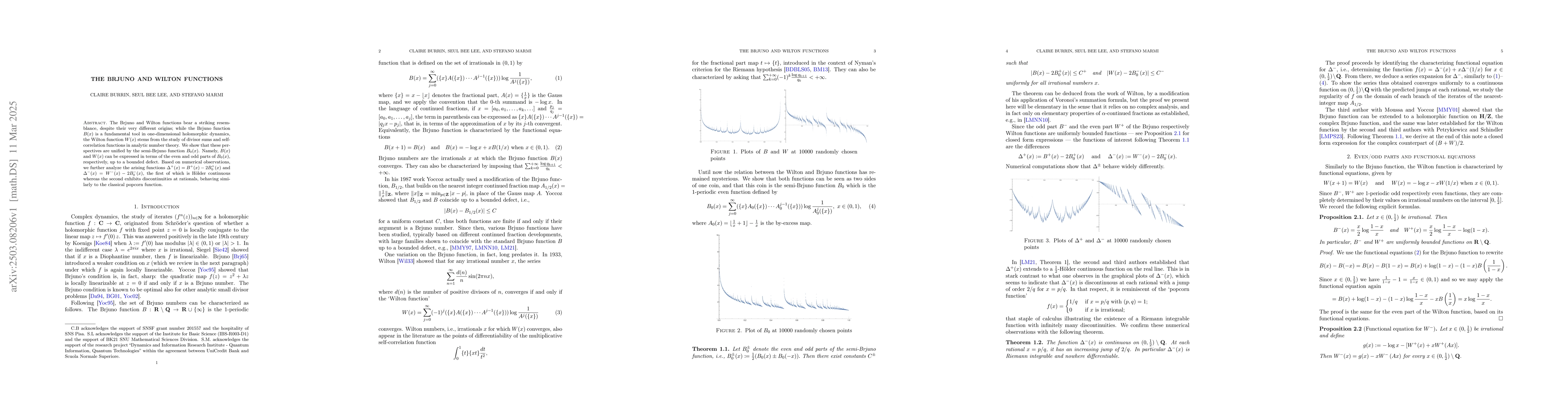

The Brjuno and Wilton functions bear a striking resemblance, despite their very different origins; while the Brjuno function $B(x)$ is a fundamental tool in one-dimensional holomorphic dynamics, the W...

Markets efficiency implies that the stock returns are intrinsically unpredictable, a property that makes markets comparable to random number generators. We present a novel methodology to investigate u...

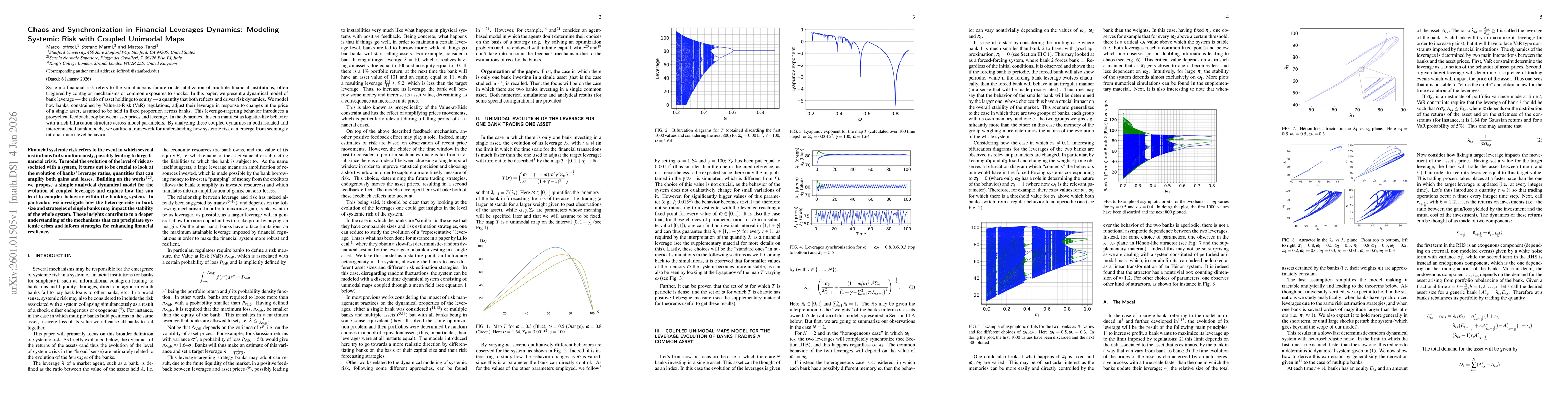

Systemic financial risk refers to the simultaneous failure or destabilization of multiple financial institutions, often triggered by contagion mechanisms or common exposures to shocks. In this paper, ...

Cohomological equations appear frequently in dynamical systems. One of the most classical examples is the Livšic equation $$ v(x) = α\circ F(x) - α(x).$$ The existence and regularity of its solutions ...

$σ$-Brjuno functions were introduced in \cite{MaMoYo_06} as an interesting variant of the classical Brjuno function, where one substitutes the $\log$ singularity at $x=0$ with the power law divergence...