Academic Profile

Statistics

Similar Authors

Papers on arXiv

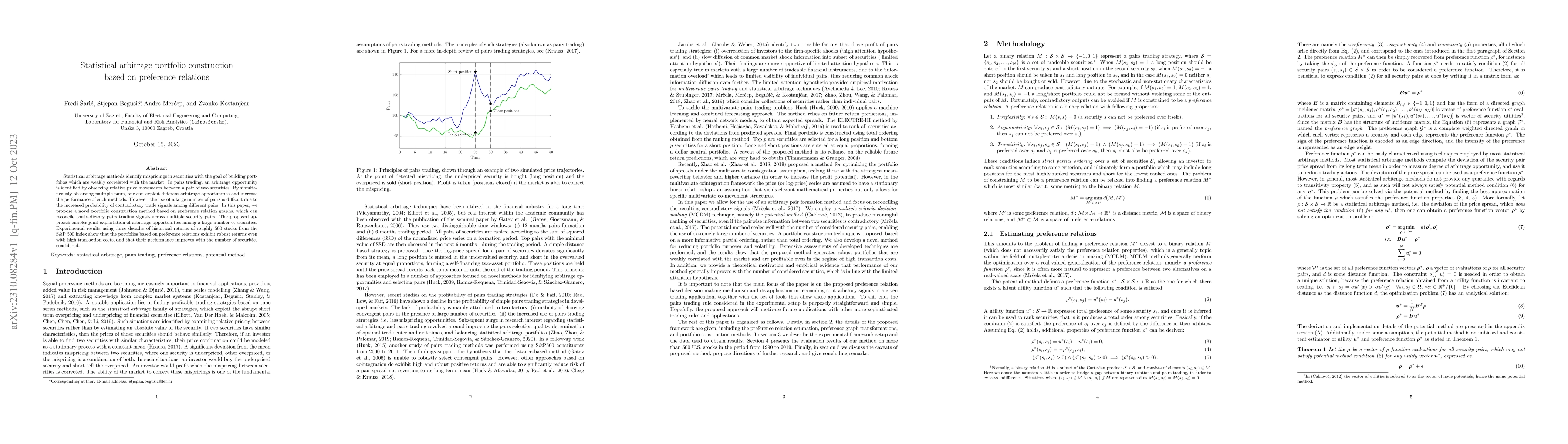

Statistical arbitrage methods identify mispricings in securities with the goal of building portfolios which are weakly correlated with the market. In pairs trading, an arbitrage opportunity is ident...

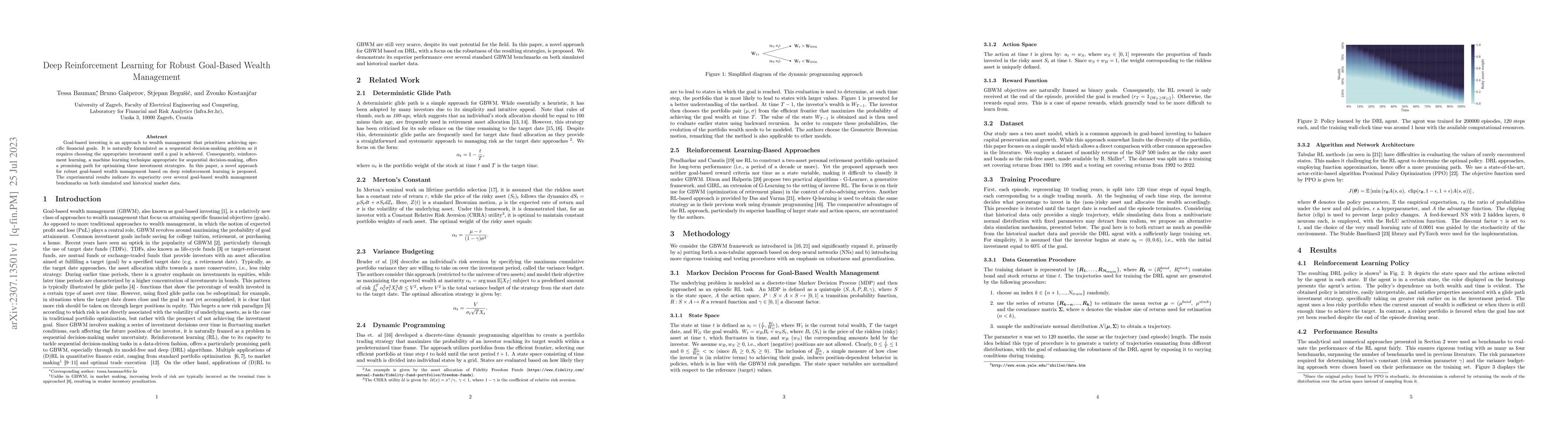

Goal-based investing is an approach to wealth management that prioritizes achieving specific financial goals. It is naturally formulated as a sequential decision-making problem as it requires choosi...

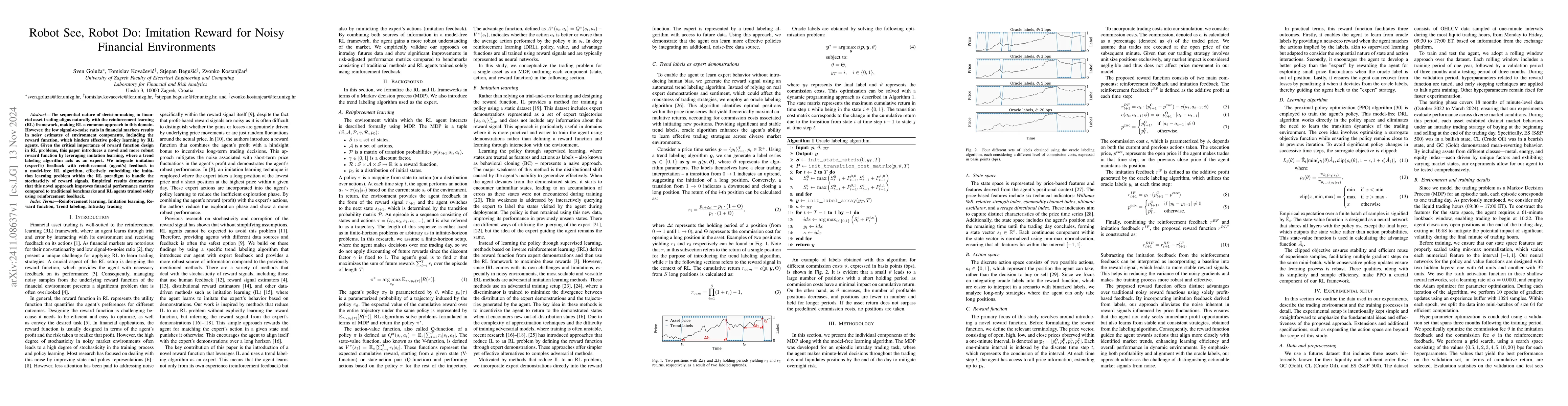

The sequential nature of decision-making in financial asset trading aligns naturally with the reinforcement learning (RL) framework, making RL a common approach in this domain. However, the low signal...

Estimation of high-dimensional covariance matrices in latent factor models is an important topic in many fields and especially in finance. Since the number of financial assets grows while the estimati...