Academic Profile

Statistics

Similar Authors

Papers on arXiv

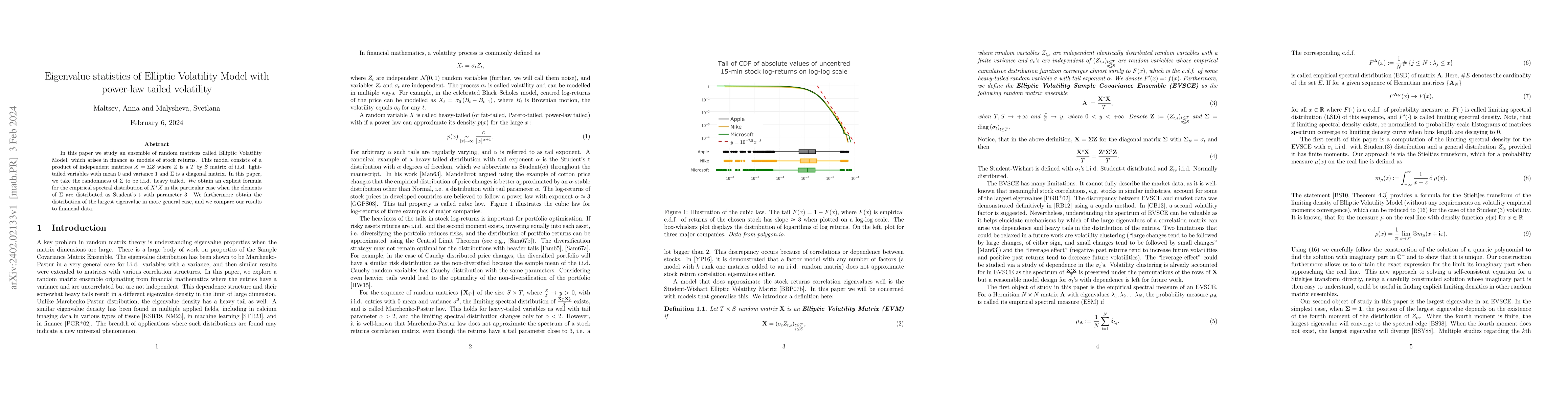

In this paper we study an ensemble of random matrices called Elliptic Volatility Model, which arises in finance as models of stock returns. This model consists of a product of independent matrices $...

We consider the spectrum of the Sample Covariance matrix $\mathbf{A}_N:= \frac{\mathbf{X}_N \mathbf{X}_N^*}{N}, $ where $\mathbf{X}_N$ is the $P\times N$ matrix with i.i.d. half-heavy tailed entries...

Difficulties identifying appropriate biodiversity impact metrics remain a major barrier to inclusion of biodiversity considerations in environmentally responsible investment. We propose and analyse ...