Academic Profile

Statistics

Similar Authors

Papers on arXiv

This research incorporates realized volatility and overnight information into risk models, wherein the overnight return often contributes significantly to the total return volatility. Extending a se...

Capital allocation is a procedure for quantifying the contribution of each source of risk to aggregated risk. The gradient allocation rule, also known as the Euler principle, is a prevalent rule of ...

A useful property of independent samples is that their correlation remains the same after applying marginal transforms. This invariance property plays a fundamental role in statistical inference, bu...

A joint mix is a random vector with a constant component-wise sum. The dependence structure of a joint mix minimizes some common objectives such as the variance of the component-wise sum, and it is ...

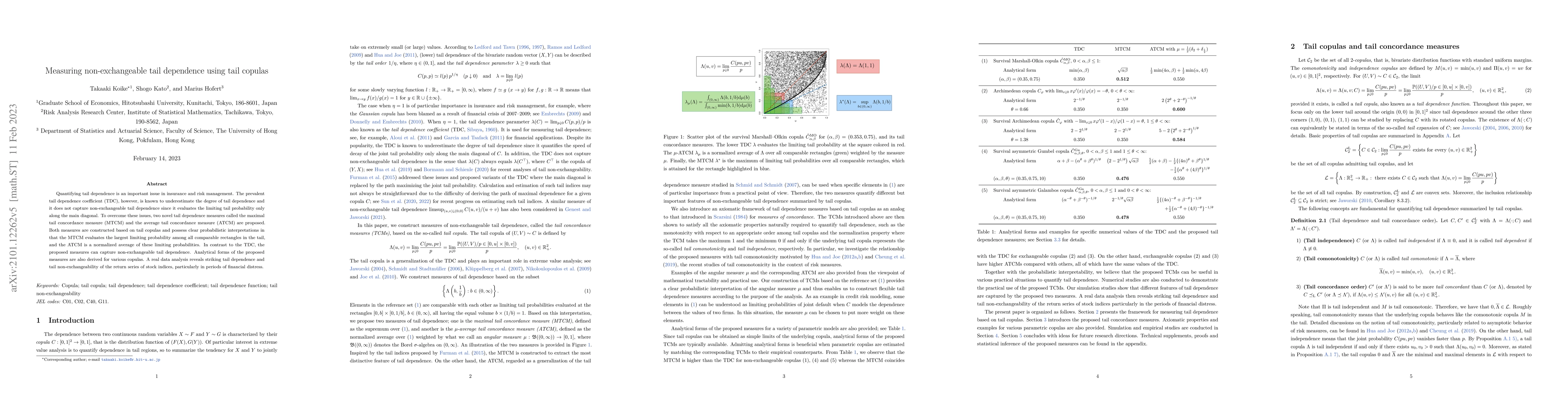

Quantifying tail dependence is an important issue in insurance and risk management. The prevalent tail dependence coefficient (TDC), however, is known to underestimate the degree of tail dependence ...

Representations of measures of concordance in terms of Pearson' s correlation coefficient are studied. All transforms of random variables are characterized such that the correlation coefficient of t...

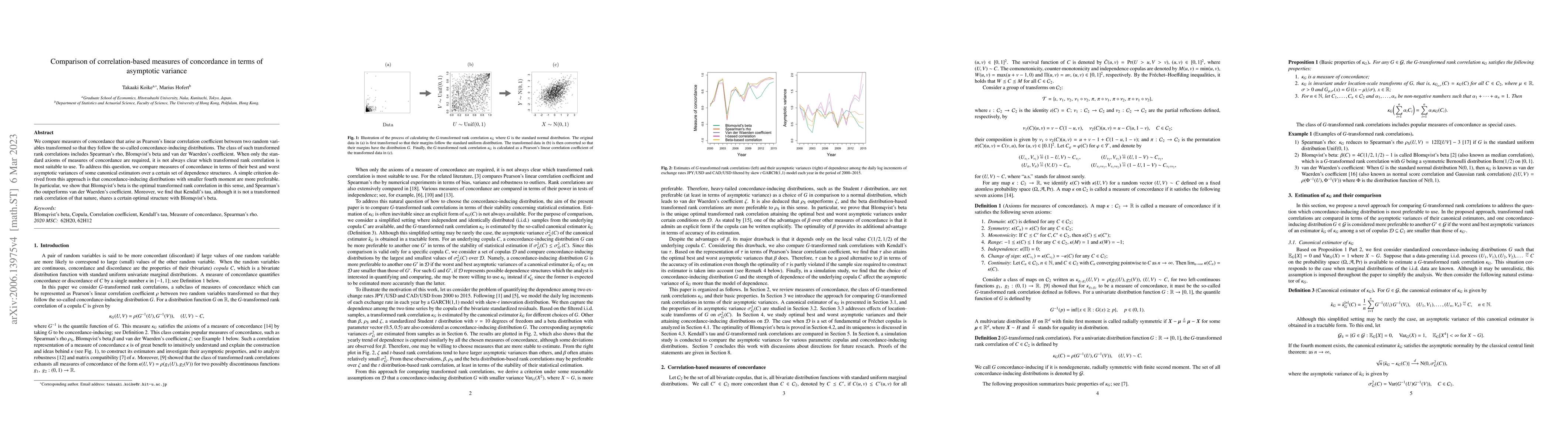

We compare measures of concordance that arise as Pearson's linear correlation coefficient between two random variables transformed so that they follow the so-called concordance-inducing distribution...

We study the variability of a risk from the statistical viewpoint of multimodality of the conditional loss distribution given that the aggregate loss equals an exogenously provided capital. This con...

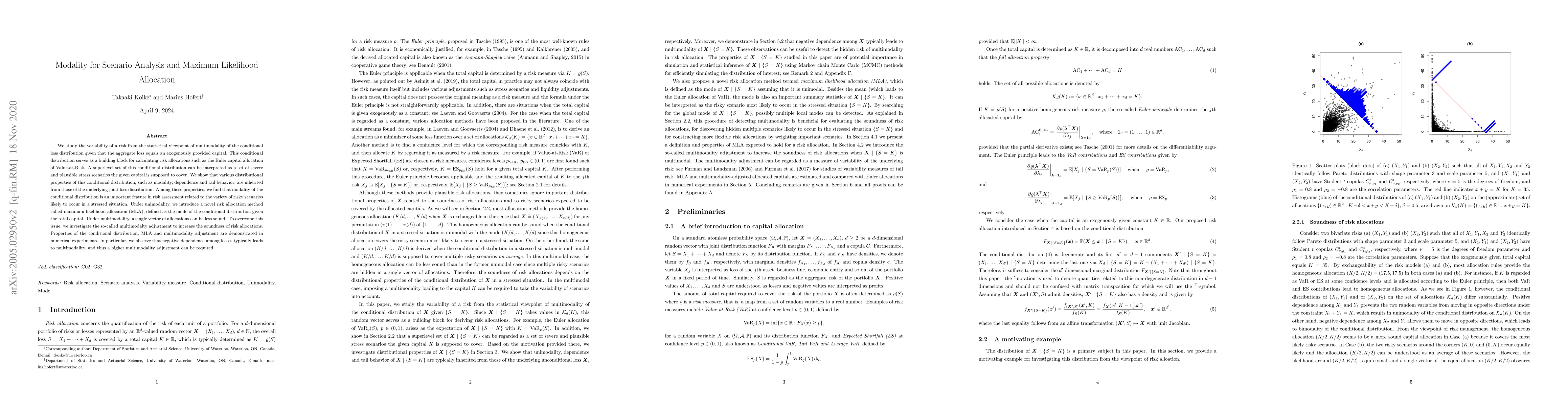

This paper is concerned with the process of risk allocation for a generic multivariate model when the risk measure is chosen as the Value-at-Risk (VaR). We recast the traditional Euler contributions...

We call two copulas tail equivalent if their first-order approximations in the tail coincide. As a special case, a copula is called tail symmetric if it is tail equivalent to the associated survival c...

Dependence among multiple lifetimes is a key factor for pricing and evaluating the risk of joint life insurance products. The dependence structure can be exposed to model uncertainty when available da...

The classical tail dependence coefficient (TDC) may fail to capture non-exchangeable features of tail dependence due to its restrictive focus on the diagonal of the underlying copula. To address this ...

The classical tail dependence coefficient (TDC) may fail to capture non-exchangeable features of bivariate tail dependence since it evaluates the underlying copula only along the diagonal. To address ...