Academic Profile

Statistics

Similar Authors

Papers on arXiv

This study investigates the volatility of daily Bitcoin returns and multifractal properties of the Bitcoin market by employing the rolling window method and examines relationships between the volati...

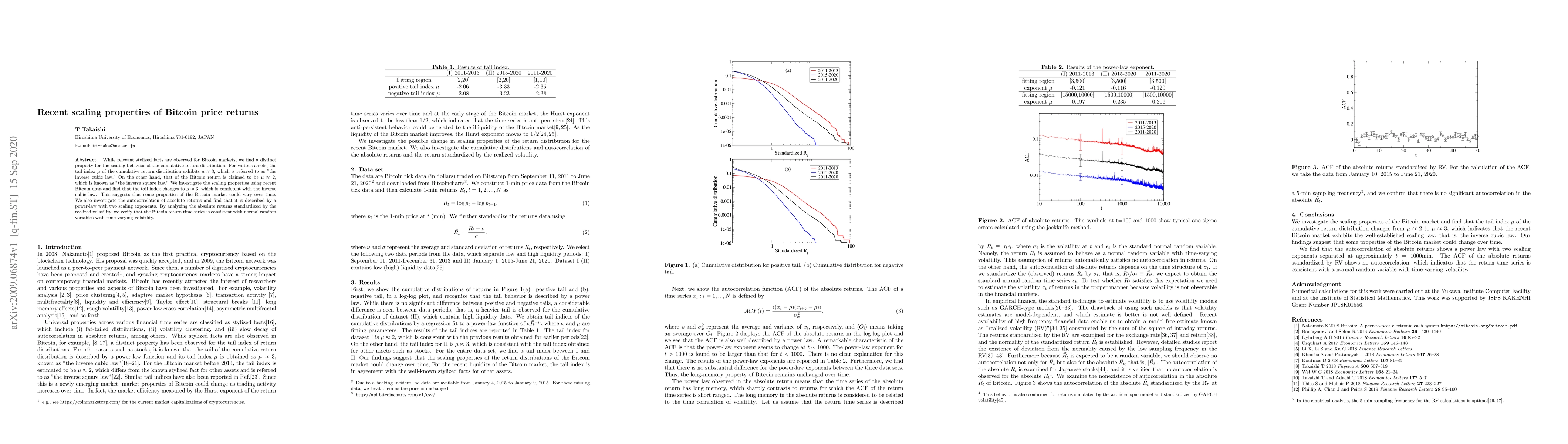

While relevant stylized facts are observed for Bitcoin markets, we find a distinct property for the scaling behavior of the cumulative return distribution. For various assets, the tail index $\mu$ o...

Recent studies have found that the log-volatility of asset returns exhibit roughness. This study investigates roughness or the anti-persistence of Bitcoin volatility. Using the multifractal detrende...

This letter investigates the dynamic relationship between market efficiency, liquidity, and multifractality of Bitcoin. We find that before 2013 liquidity is low and the Hurst exponent is less than ...

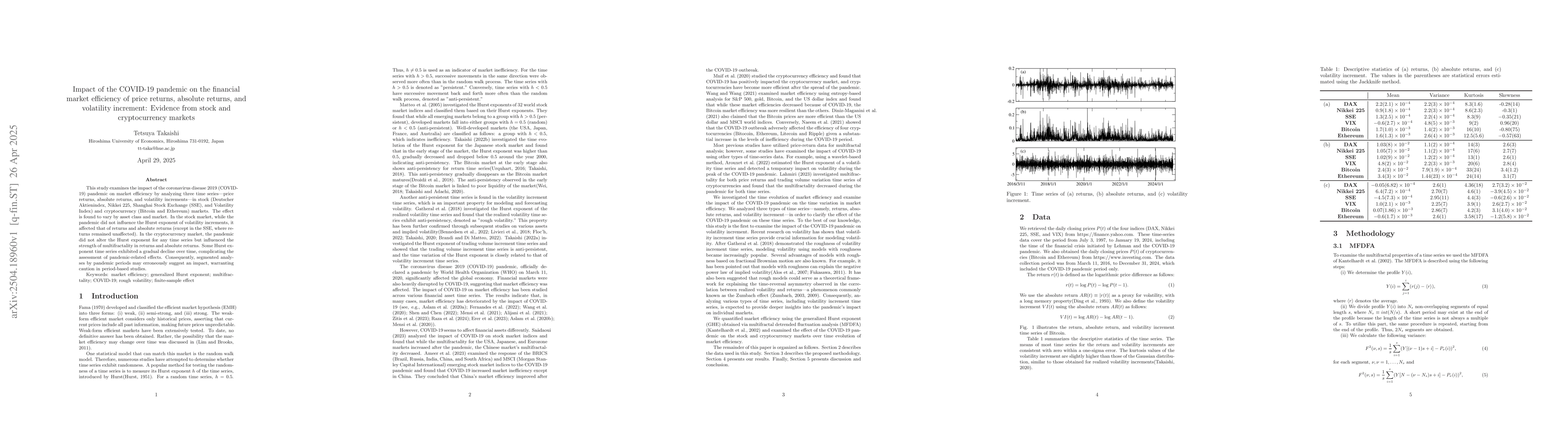

This study examines the impact of the coronavirus disease 2019 (COVID-19) pandemic on market efficiency by analyzing three time series -- price returns, absolute returns, and volatility increments -- ...

The finite sample effect on the Hurst exponent (HE) of realized volatility time series is examined using Bitcoin data. This study finds that the HE decreases as the sampling period $Δ$ increases and a...

We employ single-qubit quantum circuit learning (QCL) to model the dynamics of volatility time series. To assess its effectiveness, we generate synthetic data using the Rational GARCH model, which is ...

This study examines the effects of Trump-era tariffs on financial market efficiency by applying multifractal detrended fluctuation analysis to the return and absolute return time series of six major f...