Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel axiom of co-loss aversion for a preference relation over the space of acts, represented by measurable functions on a suitable measurable space. This axiom means that the decisio...

Wasserstein distributionally robust optimization (DRO) has found success in operations research and machine learning applications as a powerful means to obtain solutions with favourable out-of-sampl...

Data-driven distributionally robust optimization is a recently emerging paradigm aimed at finding a solution that is driven by sample data but is protected against sampling errors. An increasingly p...

We introduce a new approach for prudent risk evaluation based on stochastic dominance, which will be called the model aggregation (MA) approach. In contrast to the classic worst-case risk (WR) appro...

In this paper, we analyze the set of all possible aggregate distributions of the sum of standard uniform random variables, a simply stated yet challenging problem in the literature of distributions ...

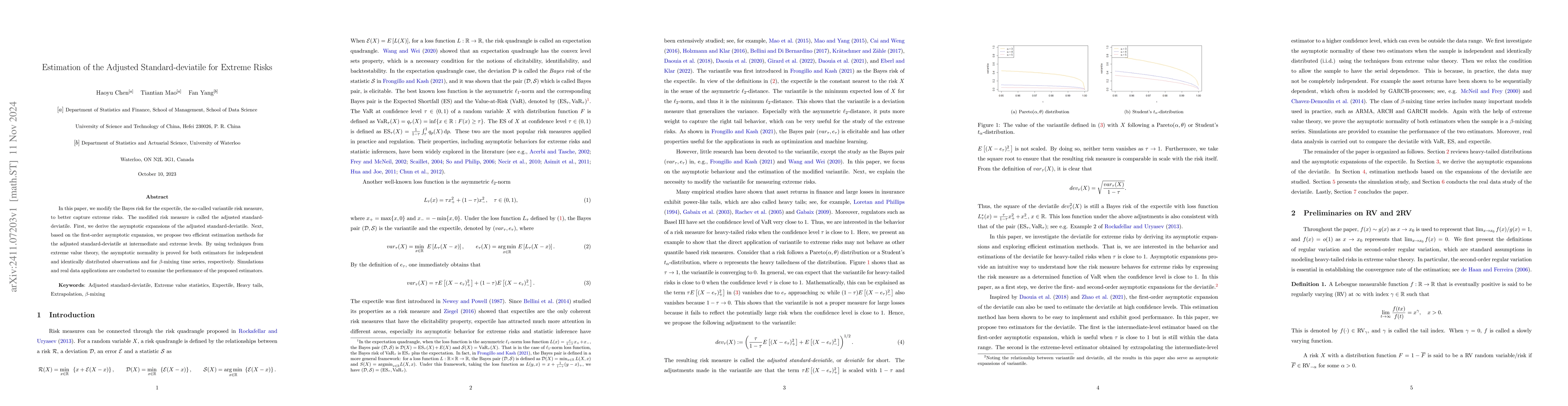

In this paper, we modify the Bayes risk for the expectile, the so-called variantile risk measure, to better capture extreme risks. The modified risk measure is called the adjusted standard-deviatile. ...

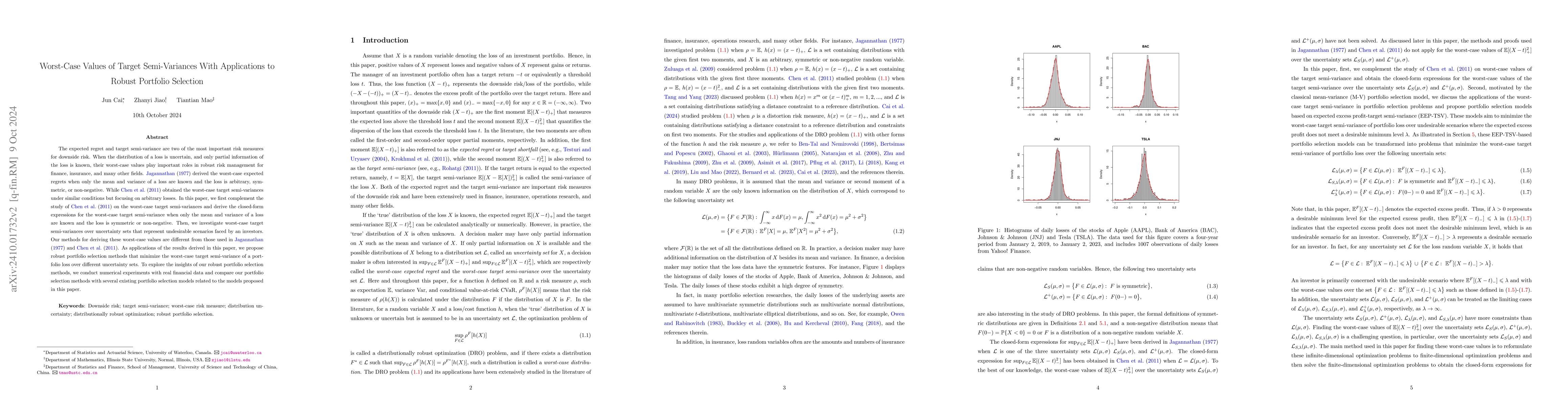

The expected regret and target semi-variance are two of the most important risk measures for downside risk. When the distribution of a loss is uncertain, and only partial information of the loss is kn...

We study a general risk measure called the generalized shortfall risk measure, which was first introduced in Mao and Cai (2018). It is proposed under the rank-dependent expected utility framework, or ...

Choquet capacities and integrals are central concepts in decision making under ambiguity or model uncertainty, pioneered by Schmeidler. Motivated by risk optimization problems for quantiles under ambi...

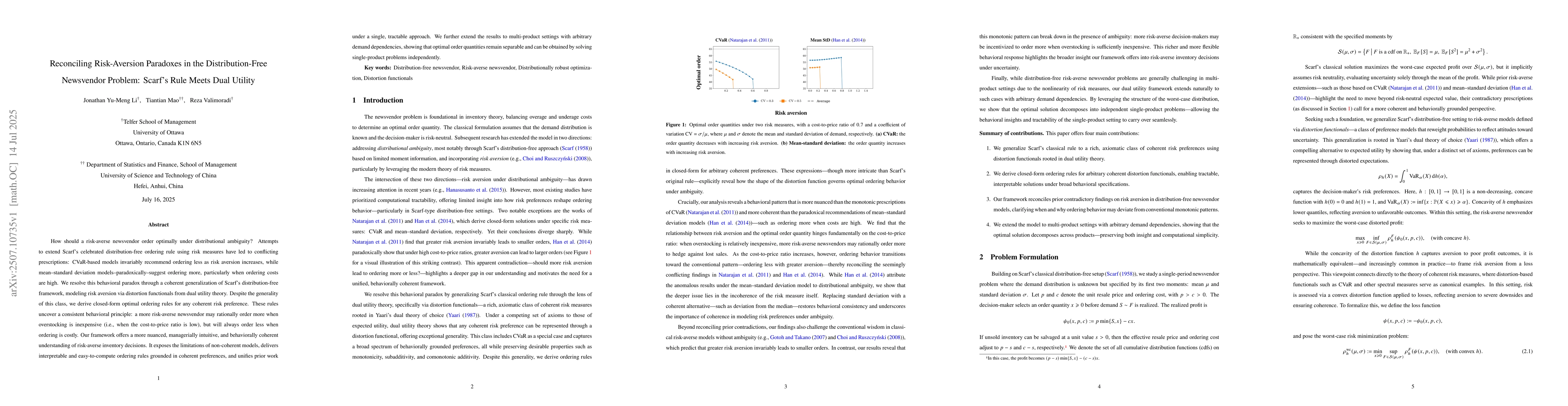

How should a risk-averse newsvendor order optimally under distributional ambiguity? Attempts to extend Scarf's celebrated distribution-free ordering rule using risk measures have led to conflicting pr...

This paper recasts Gul (1991)'s theory of disappointment aversion in a Savage framework, with general outcomes, new explicit axioms of disappointment aversion, and novel explicit representations. Thes...

Heavy-tailed combination tests, such as the Cauchy combination test and harmonic mean p-value method, are widely used for testing global null hypotheses by aggregating dependent p-values. However, the...

We study distributionally robust quantile regression using type-$p$ Wasserstein ambiguity sets. We derive a closed-form expression for the worst-case quantile regression loss under general $p$-Wassers...

We study asymptotic probabilities of attaining the maximum in heterogeneous Gaussian samples. In the two-group setting, the first sample has variance $1$ and size $n_1$, while the second has variance ...

In this paper, we introduce a class of preference robust risk measures-\emph{robust optimized certainty equivalents} (ROCE)-which encompasses several widely used measures, including Conditional Value-...