Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a unified, market-complete model that integrates both the Bachelier and Black-Scholes-Merton frameworks for asset pricing. The model allows for the study, within a unified framework, of a...

Using data from 2000 through 2022, we analyze the predictive capability of the annual numbers of new home constructions and four available environmental, social, and governance factors on the averag...

We develop two alternate approaches to arbitrage-free, market-complete, option pricing. The first approach requires no riskless asset. We develop the general framework for this approach and illustra...

We propose a discrete-time econometric model that combines autoregressive filters with factor regressions to predict stock returns for portfolio optimisation purposes. In particular, we test both ro...

The growing interest in sustainable investing calls for an axiomatic approach to measures of risk and reward that focus not only on financial returns, but also on measures of environmental and socia...

We introduce a discrete binary tree for pricing contingent claims with the underlying security prices exhibiting history dependence characteristic of that induced by market microstructure phenomena....

Motivated by the Corns-Satchell, continuous time, option pricing model, we develop a binary tree pricing model with underlying asset price dynamics following It\^o-Mckean skew Brownian motion. While...

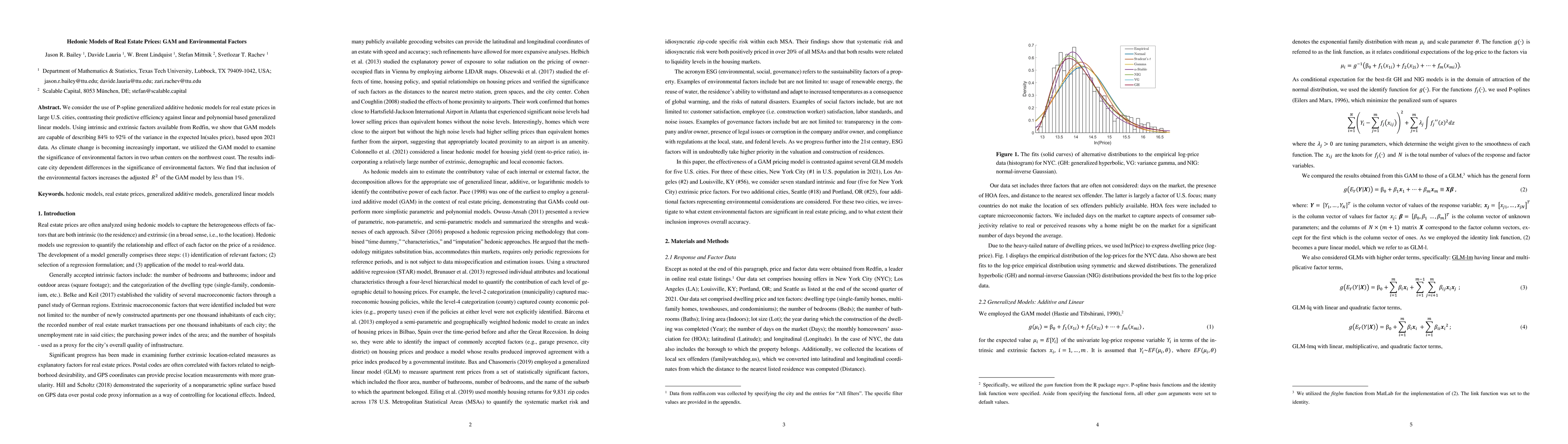

We consider the use of P-spline generalized additive hedonic models for real estate prices in large U.S. cities, contrasting their predictive efficiency against linear and polynomial based generaliz...

We consider option pricing using replicating binomial trees, with a two fold purpose. The first is to introduce ESG valuation into option pricing. We explore this in a number of scenarios, including...

ESG ratings provide a quantitative measure for socially responsible investment. We present a unified framework for incorporating numeric ESG ratings into dynamic pricing theory. Specifically, we int...

We propose a doubly subordinated Levy process, NDIG, to model the time series properties of the cryptocurrency bitcoin. NDIG captures the skew and fat-tailed properties of bitcoin prices and gives r...

Applying the Cherny-Shiryaev-Yor invariance principle, we introduce a generalized Jarrow-Rudd (GJR) option pricing model with uncertainty driven by a skew random walk. The GJR pricing tree exhibits ...

This paper investigates performance attribution measures as a basis for constraining portfolio optimization. We employ optimizations that minimize expected tail loss and investigate both asset alloc...

Using the Donsker-Prokhorov invariance principle we extend the Kim-Stoyanov-Rachev-Fabozzi option pricing model to allow for variably-spaced trading instances, an important consideration for short-s...

We address the problem of asset pricing in a market where there is no risky asset. Previous work developed a theoretical model for a shadow riskless rate (SRR) for such a market in terms of the drift ...

We introduce a fairly general, recombining trinomial tree model in the natural world. Market-completeness is ensured by considering a market consisting of two risky assets, a riskless asset, and a Eur...

We propose a machine learning-based extension of the classical binomial option pricing model that incorporates key market microstructure effects. Traditional models assume frictionless markets, overlo...

We extend the application of the Cherny-Shiryaev-Yor invariance principle to a unified Bachelier-Black-Scholes-Merton (BBSM) dynamic pricing model. This extension incorporates the influence of the his...

We present two models for incorporating the total effect of market microstructure noise into dynamic pricing of assets and European options. The first model is developed under a Black-Scholes-Merton, ...

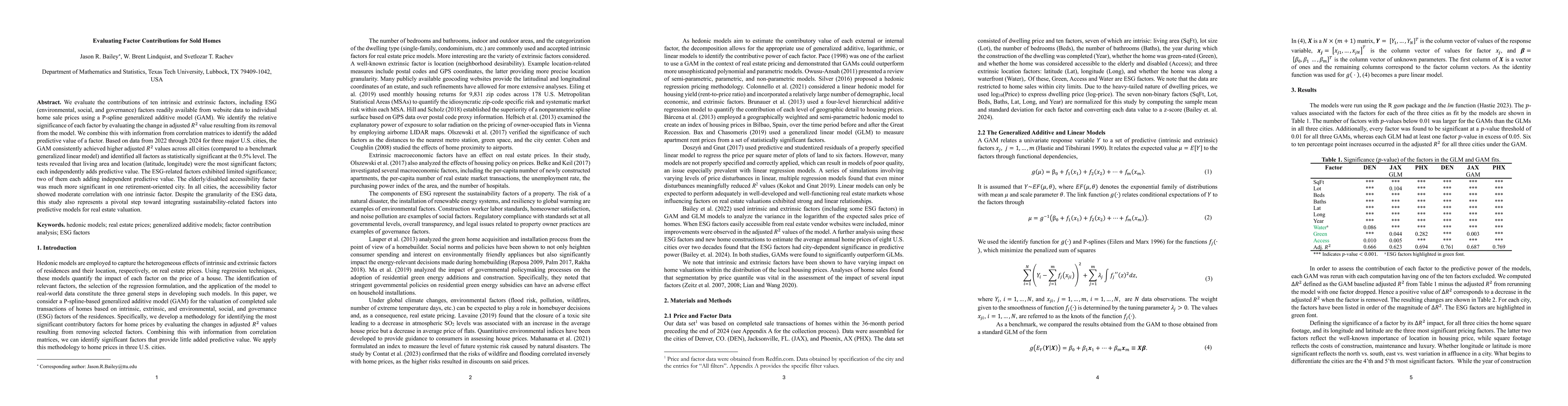

We evaluate the contributions of ten intrinsic and extrinsic factors, including ESG (environmental, social, and governance) factors readily available from website data to individual home sale prices u...

This paper addresses a critical inconsistency in models of the term structure of interest rates (TSIR), where zero-coupon bonds are priced under risk-neutral measures distinct from those used in equit...

Classical option pricing models, such as Bachelier and Black--Scholes--Merton, postulate symmetric Brownian diffusion, which limits their capacity to reflect empirical phenomena including return skewn...