Academic Profile

Statistics

Similar Authors

Papers on arXiv

Recent advances in deep learning for solving partial differential equations (PDEs) have introduced physics-informed neural networks (PINNs), which integrate machine learning with physical laws. Physic...

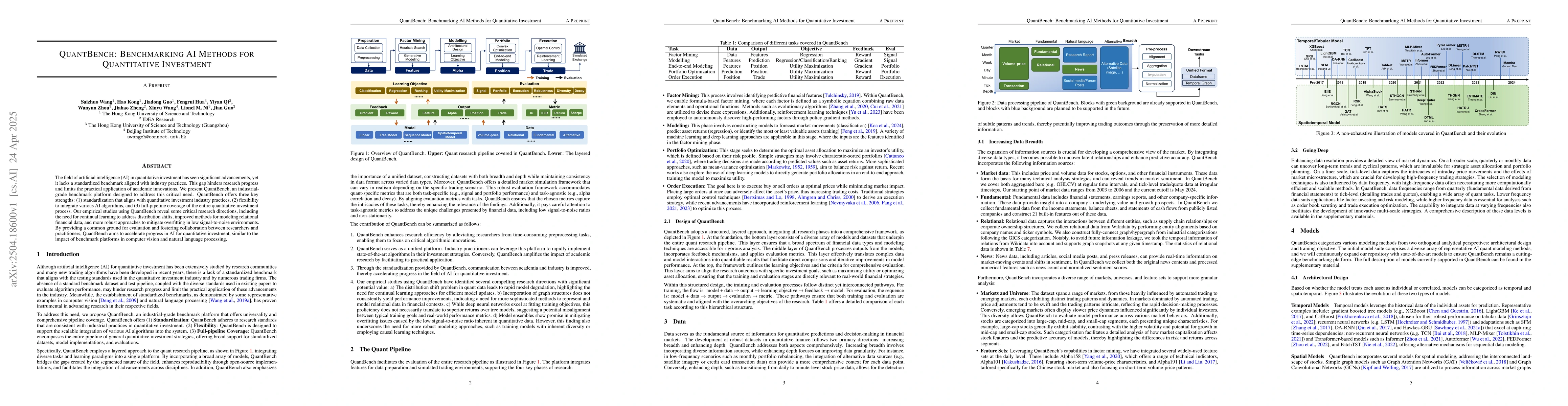

The field of artificial intelligence (AI) in quantitative investment has seen significant advancements, yet it lacks a standardized benchmark aligned with industry practices. This gap hinders research...

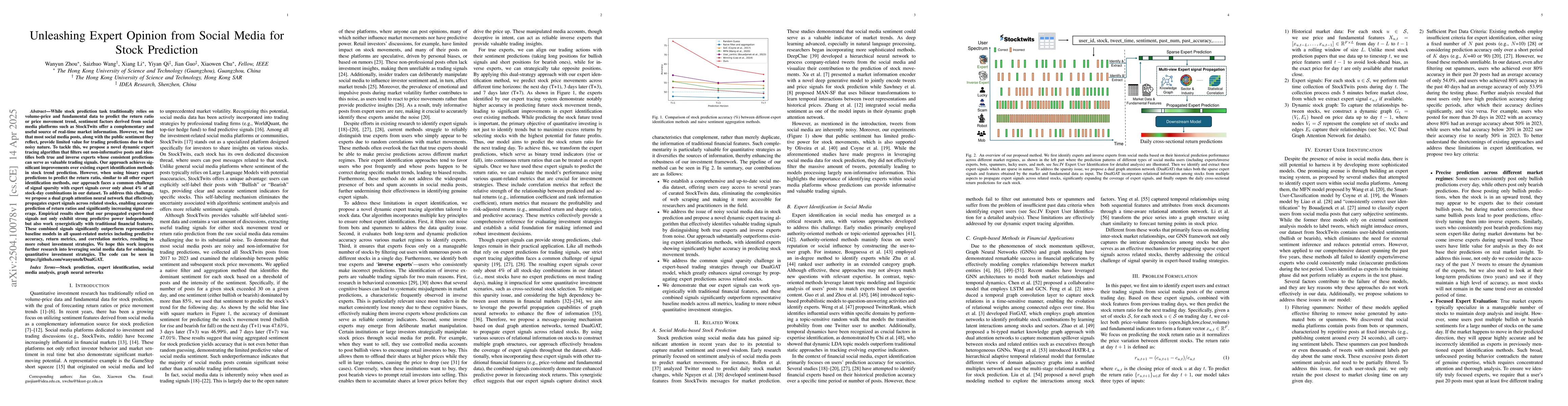

While stock prediction task traditionally relies on volume-price and fundamental data to predict the return ratio or price movement trend, sentiment factors derived from social media platforms such as...

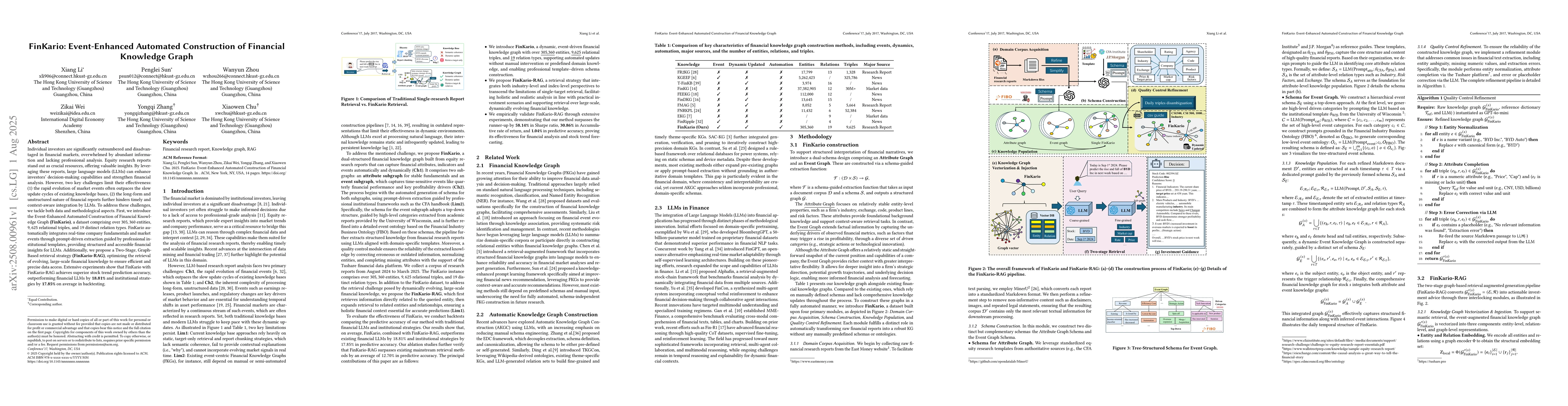

Individual investors are significantly outnumbered and disadvantaged in financial markets, overwhelmed by abundant information and lacking professional analysis. Equity research reports stand out as c...

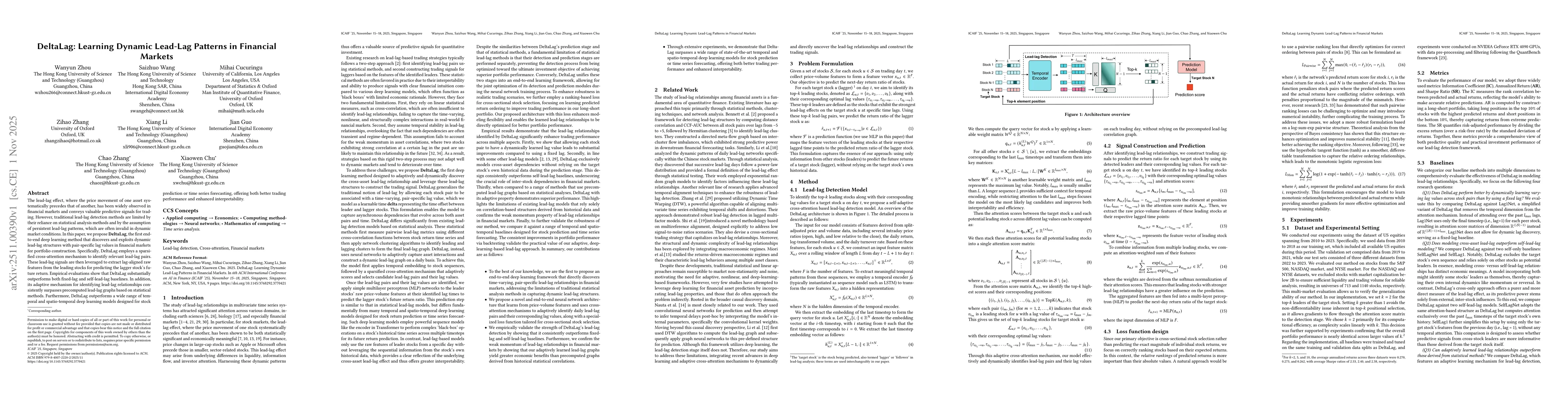

The lead-lag effect, where the price movement of one asset systematically precedes that of another, has been widely observed in financial markets and conveys valuable predictive signals for trading. H...

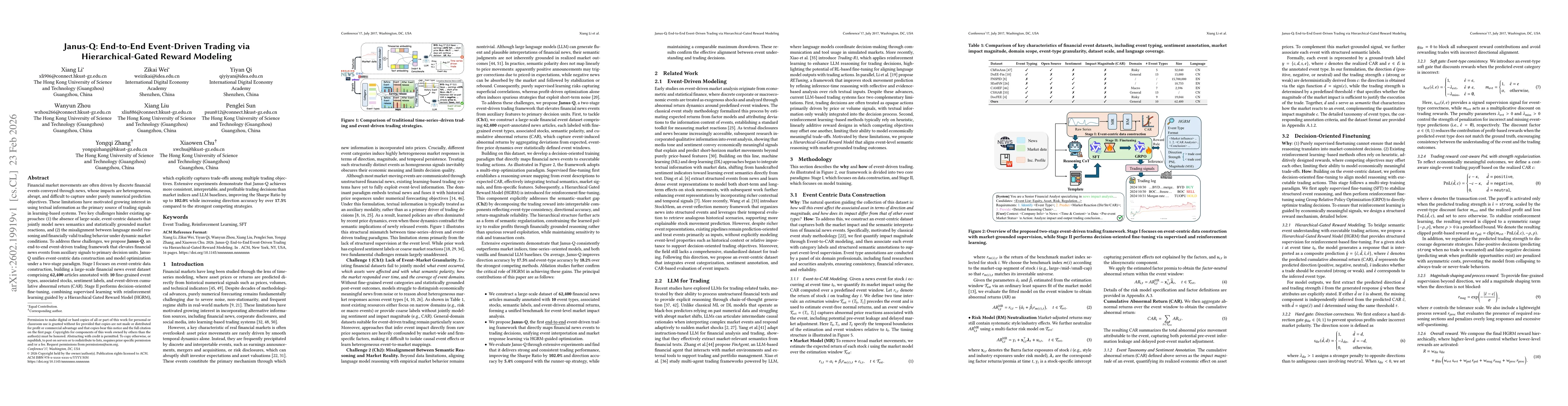

Financial market movements are often driven by discrete financial events conveyed through news, whose impacts are heterogeneous, abrupt, and difficult to capture under purely numerical prediction obje...