Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop an unsupervised deep learning method to solve the barrier options under the Bergomi model. The neural networks serve as the approximate option surfaces and are trained to satisfy the PDE ...

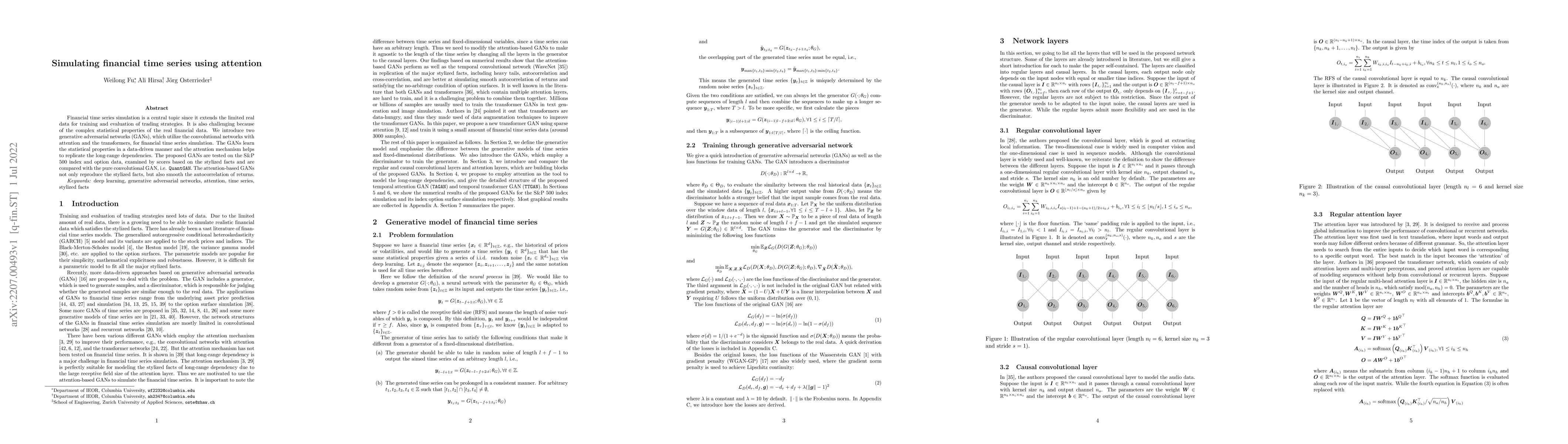

Financial time series simulation is a central topic since it extends the limited real data for training and evaluation of trading strategies. It is also challenging because of the complex statistica...

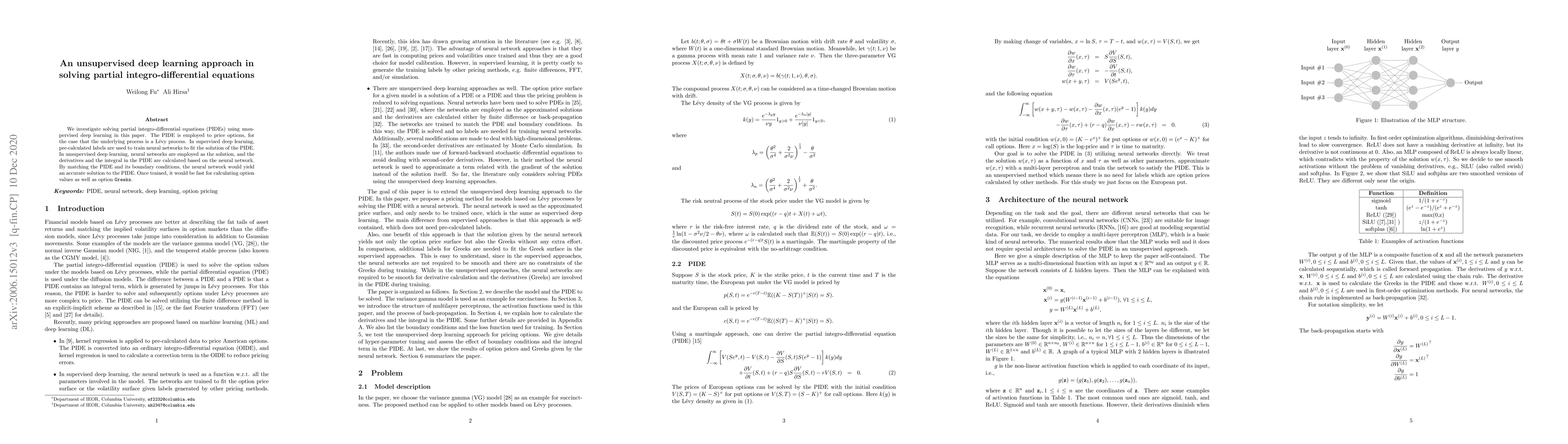

We investigate solving partial integro-differential equations (PIDEs) using unsupervised deep learning in this paper. To price options, assuming underlying processes follow Levy processes, we requir...

Proteins are the major building blocks of life, and actuators of almost all chemical and biophysical events in living organisms. Their native structures in turn enable their biological functions whi...

We investigate methods for pricing American options under the variance gamma model. The variance gamma process is a pure jump process which is constructed by replacing the calendar time by the gamma...

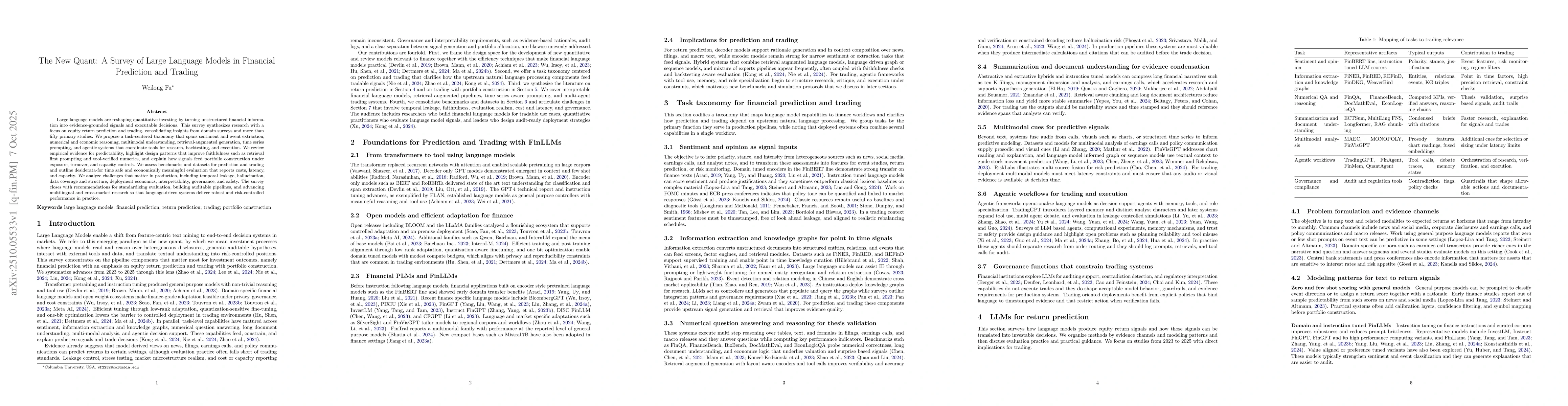

Large language models are reshaping quantitative investing by turning unstructured financial information into evidence-grounded signals and executable decisions. This survey synthesizes research with ...