Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a comprehensive framework for policy gradient methods tailored to continuous time reinforcement learning. This is based on the connection between stochastic control problems and randomise...

We study deterministic optimal control problems for differential games with finite horizon. We propose new approximations of the strategies in feedback form, and show error estimates and a convergen...

In this paper, we introduce various machine learning solvers for (coupled) forward-backward systems of stochastic differential equations (FBSDEs) driven by a Brownian motion and a Poisson random mea...

We develop a new policy gradient and actor-critic algorithm for solving mean-field control problems within a continuous time reinforcement learning setting. Our approach leverages a gradient-based r...

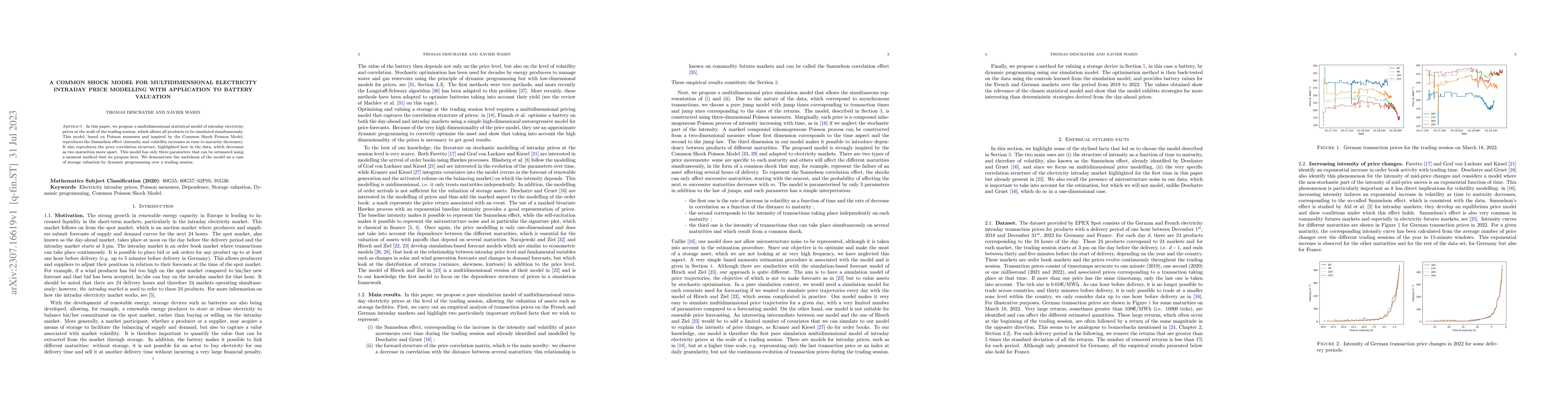

In this paper, we propose a multidimensional statistical model of intraday electricity prices at the scale of the trading session, which allows all products to be simulated simultaneously. This mode...

We study news neural networks to approximate function of distributions in a probability space. Two classes of neural networks based on quantile and moment approximation are proposed to learn these f...

This paper is devoted to the numerical resolution of McKean-Vlasov control problems via the class of mean-field neural networks introduced in our companion paper [25] in order to learn the solution ...

We study the machine learning task for models with operators mapping between the Wasserstein space of probability measures and a space of functions, like e.g. in mean-field games/control problems. T...

We consider a deterministic optimal control problem with a maximum running cost functional, in a finite horizon context, and propose deep neural network approximations for Bellman's dynamic programm...

We present a new neural network to approximate convex functions. This network has the particularity to approximate the function with cuts and can be easily adapted to partial convexity. We give an u...

We consider the control of McKean-Vlasov dynamics (or mean-field control) with probabilistic state constraints. We rely on a level-set approach which provides a representation of the constrained pro...

After showing the efficiency of feedforward networks to estimate control in high dimension in the global optimization of some storages problems, we develop a modification of an algorithm based on so...

Machine learning methods for solving nonlinear partial differential equations (PDEs) are hot topical issues, and different algorithms proposed in the literature show efficient numerical approximatio...

We prove a rate of convergence for the $N$-particle approximation of a second-order partial differential equation in the space of probability measures, like the Master equation or Bellman equation o...

We propose deep neural network algorithms to calculate efficient frontier in some Mean-Variance and Mean-CVaR portfolio optimization problems. We show that we are able to deal with such problems whe...

In this work, we provide a general mathematical formalism to study the optimal control of an epidemic, such as the COVID-19 pandemic, via incentives to lockdown and testing. In particular, we model ...

We study the approximation of backward stochastic differential equations (BSDEs for short) with a constraint on the gains process. We first discretize the constraint by applying a so-called facelift...

We propose several algorithms to solve McKean-Vlasov Forward Backward Stochastic Differential Equations. Our schemes rely on the approximating power of neural networks to estimate the solution or it...

We propose a numerical method for solving high dimensional fully nonlinear partial differential equations (PDEs). Our algorithm estimates simultaneously by backward time induction the solution and i...

We propose some machine-learning-based algorithms to solve hedging problems in incomplete markets. Sources of incompleteness cover illiquidity, untradable risk factors, discrete hedging dates and tr...

We propose new machine learning schemes for solving high dimensional nonlinear partial differential equations (PDEs). Relying on the classical backward stochastic differential equation (BSDE) repres...

Multi stage stochastic programs arise in many applications from engineering whenever a set of inventories or stocks has to be valued. Such is the case in seasonal storage valuation of a set of casca...

A new Kolmogorov-Arnold network (KAN) is proposed to approximate potentially irregular functions in high dimension. We show that it outperforms multilayer perceptrons in terms of accuracy and converge...

Rahimi and Recht [31] introduced the idea of decomposing shift-invariant kernels by randomly sampling from their spectral distribution. This famous technique, known as Random Fourier Features (RFF), i...

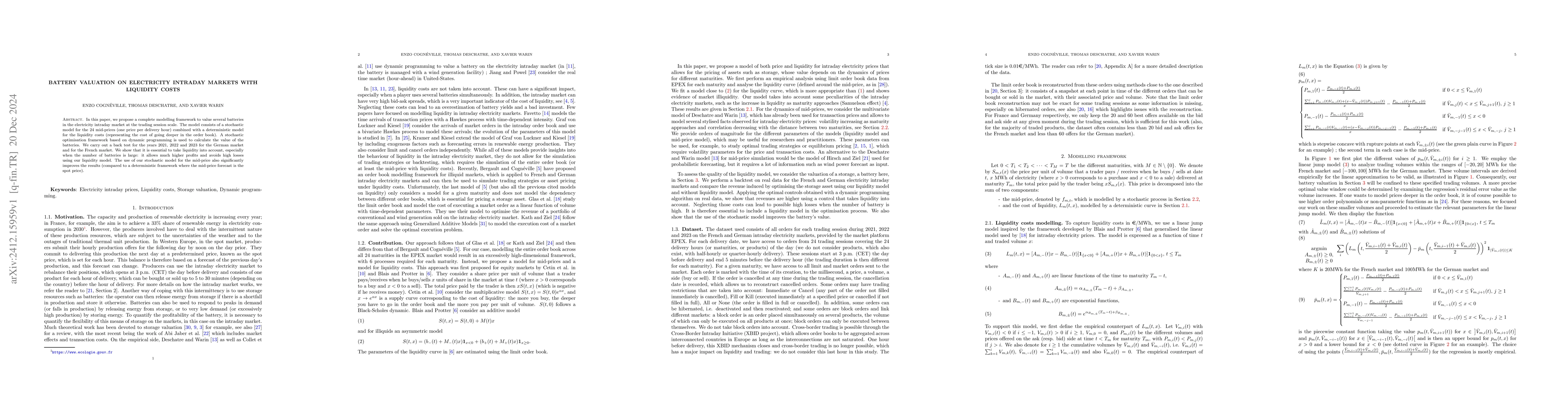

In this paper, we propose a complete modelling framework to value several batteries in the electricity intraday market at the trading session scale. The model consists of a stochastic model for the 24...

This article introduces a novel mean-field game model for multi-sector economic growth in which a dynamically evolving externality, influenced by the collective actions of agents, plays a central role...

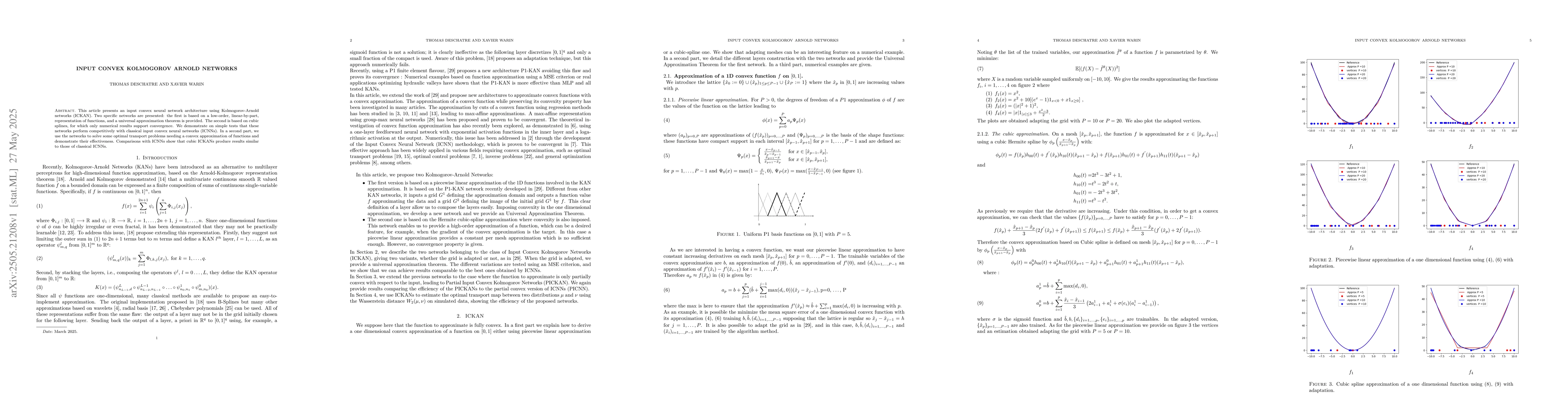

This article presents an input convex neural network architecture using Kolmogorov-Arnold networks (ICKAN). Two specific networks are presented: the first is based on a low-order, linear-by-part, repr...

To speed up Gaussian process inference, a number of fast kernel matrix-vector multiplication (MVM) approximation algorithms have been proposed over the years. In this paper, we establish an exact fast...

We study the approximation of operators acting on probability measures on a product space with prescribed marginal. Let $I$ be a label space endowed with a reference measure $λ$, and define $\cal M_λ$...

Saddle-point models arise throughout optimization, optimal transport, robust learning, and control. In many applications, the relevant function f(x,y) is convex in x and concave in y, and preserving t...