Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we investigate the robust models for $\Lambda$-quantiles with partial information regarding the loss distribution, where $\Lambda$-quantiles extend the classical quantiles by replacin...

This paper studies an optimal insurance contracting problem in which the preferences of the decision maker given by the sum of the expected loss and a convex, increasing function of a deviation meas...

Mean-deviation models, along with the existing theory of coherent risk measures, are well studied in the literature. In this paper, we characterize monotonic mean-deviation (risk) measures from a ge...

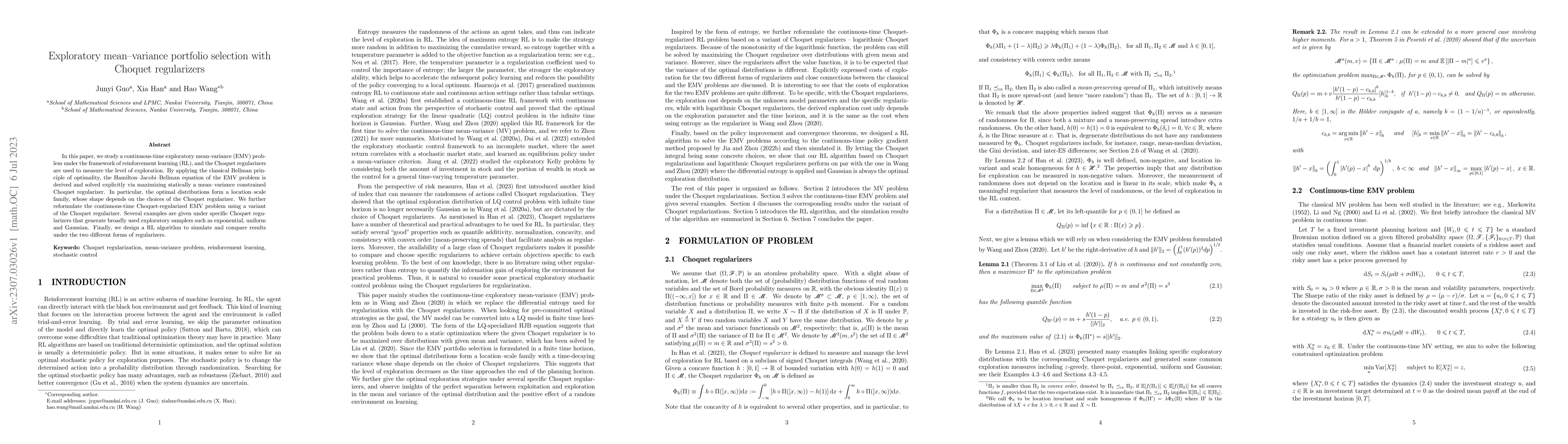

In this paper, we study a continuous-time exploratory mean-variance (EMV) problem under the framework of reinforcement learning (RL), and the Choquet regularizers are used to measure the level of ex...

In this paper, we first introduce several new classes of weighted amalgam spaces. Then we discuss both strong type and weak type estimates for certain multilinear $\theta$-type Calder\'on--Zygmund o...

In this paper, we consider the boundedness properties of multilinear $\theta$-type Calder\'on--Zygmund operators $T_\theta$ recently introduced in the literature. First, we prove strong type and wea...

The diversification quotient (DQ) is recently introduced for quantifying the degree of diversification of a stochastic portfolio model. It has an axiomatic foundation and can be defined through a pa...

We propose \emph{Choquet regularizers} to measure and manage the level of exploration for reinforcement learning (RL), and reformulate the continuous-time entropy-regularized RL problem of Wang et a...

We establish the first axiomatic theory for diversification indices using six intuitive axioms: non-negativity, location invariance, scale invariance, rationality, normalization, and continuity. The...

In the literature of risk measures, cash subadditivity was proposed to replace cash additivity, motivated by the presence of stochastic or ambiguous interest rates and defaultable contingent claims....

Expected Shortfall (ES, also known as CVaR) is the most important coherent risk measure in finance, insurance, risk management, and engineering. Recently, Wang and Zitikis (2021) put forward four ec...

In this paper, we study an optimal reinsurance-investment problem in a risk model with two dependent classes of insurance business, where the two claim number processes are correlated through a comm...

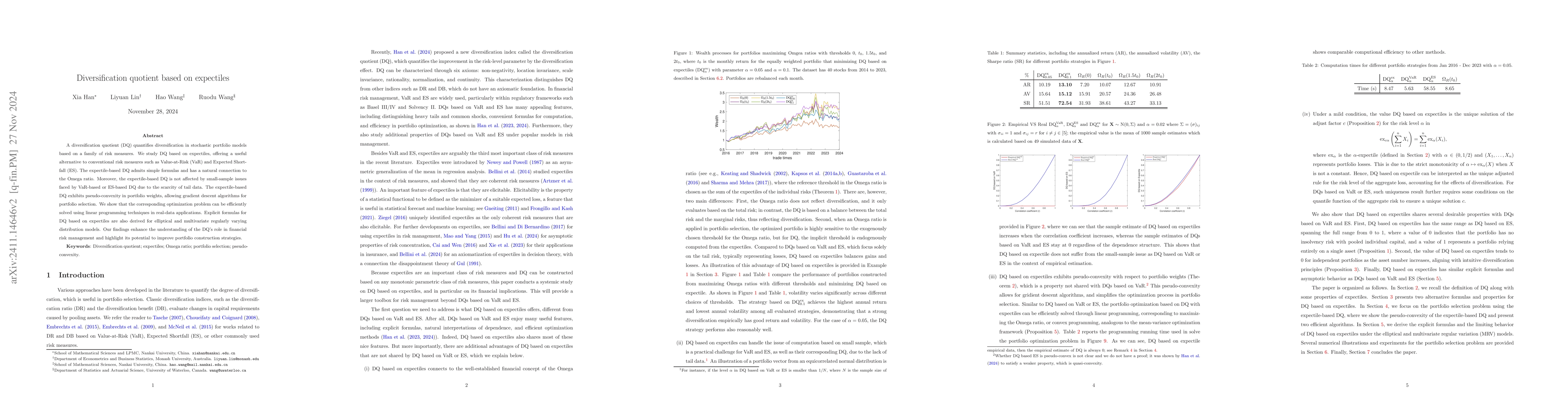

A diversification quotient (DQ) quantifies diversification in stochastic portfolio models based on a family of risk measures. We study DQ based on expectiles, offering a useful alternative to conventi...

This paper explores optimal insurance solutions based on the Lambda-Value-at-Risk ($\Lambda\VaR$). If the expected value premium principle is used, our findings confirm that, similar to the VaR model,...

This paper investigates the dynamic reinsurance design problem under the mean-variance criterion, incorporating heterogeneous beliefs between the insurer and the reinsurer, and introducing an incentiv...

In this paper, we investigate a competitive market involving two agents who consider both their own wealth and the wealth gap with their opponent. Both agents can invest in a financial market consisti...

The Diversification Quotient (DQ), introduced by Han et al. (2025), is a recently proposed measure of portfolio diversification that quantifies the reduction in a portfolio's risk-level parameter attr...

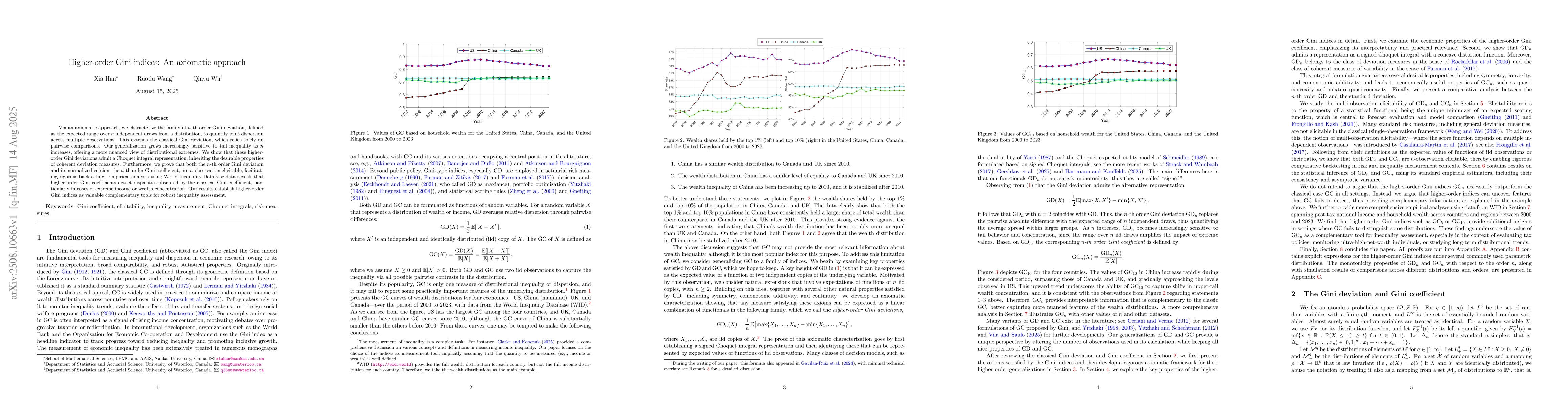

Via an axiomatic approach, we characterize the family of n-th order Gini deviation, defined as the expected range over n independent draws from a distribution, to quantify joint dispersion across mult...

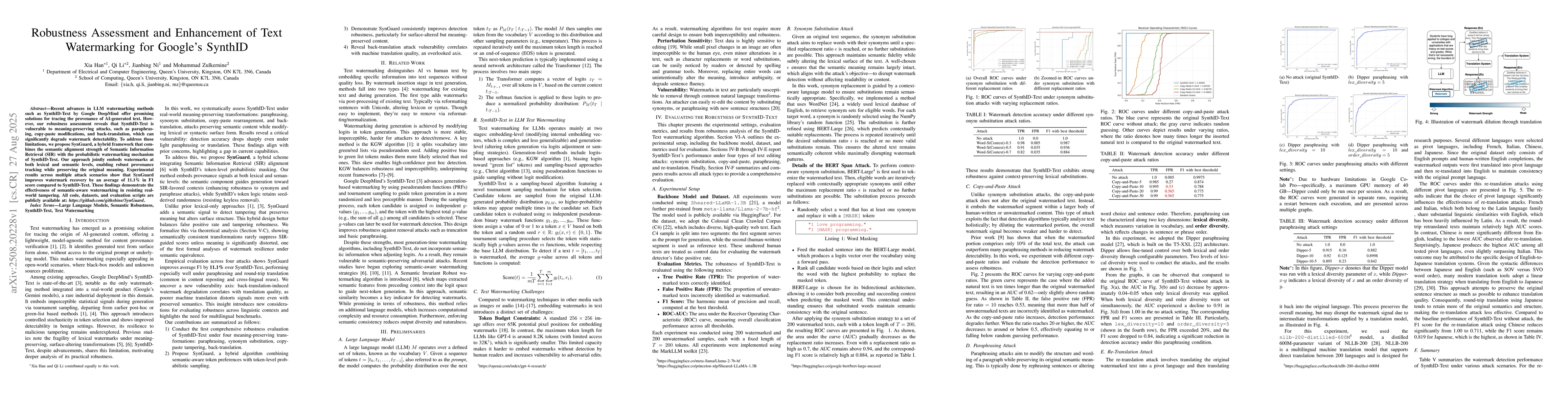

Recent advances in LLM watermarking methods such as SynthID-Text by Google DeepMind offer promising solutions for tracing the provenance of AI-generated text. However, our robustness assessment reveal...

This paper studies Pareto-optimal reinsurance design in a monopolistic market with multiple primary insurers and a single reinsurer, all with heterogeneous risk preferences. The risk preferences are c...

This paper studies optimal insurance design under asymmetric information in a Stackelberg framework, where a monopolistic insurer faces uncertainty about both the insured's risk attitude, captured by ...