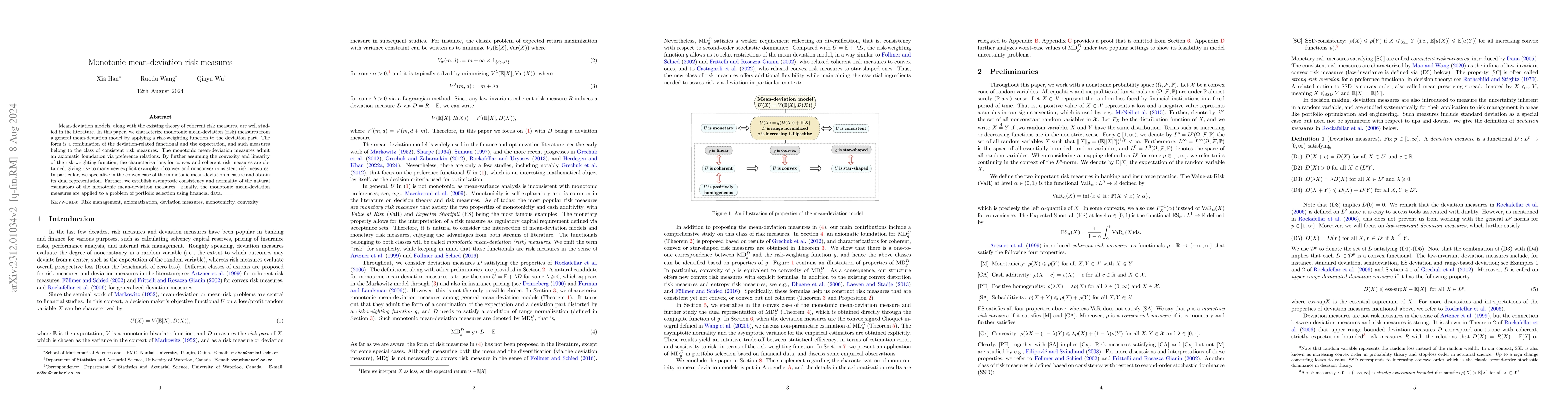

Mean-deviation models, along with the existing theory of coherent risk

measures, are well studied in the literature. In this paper, we characterize

monotonic mean-deviation (risk) measures from a general mean-deviation model by

applying a risk-weighting function to the deviation part. The form is a

combination of the deviation-related functional and the expectation, and such

measures belong to the class of consistent risk measures. The monotonic

mean-deviation measures admit an axiomatic foundation via preference relations.

By further assuming the convexity and linearity of the risk-weighting function,

the characterizations for convex and coherent risk measures are obtained,

giving rise to many new explicit examples of convex and nonconvex consistent

risk measures. Further, we specialize in the convex case of the monotonic

mean-deviation measure and obtain its dual representation. The worst-case

values of the monotonic mean-deviation measures are analyzed under two popular

settings of model uncertainty. Finally, we establish asymptotic consistency and

normality of the natural estimators of the monotonic mean-deviation measures.

Discussion 0