Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper proposes general methods for the problem of multiple testing of a single hypothesis, with a standard goal of combining a number of p-values without making any assumptions about their depe...

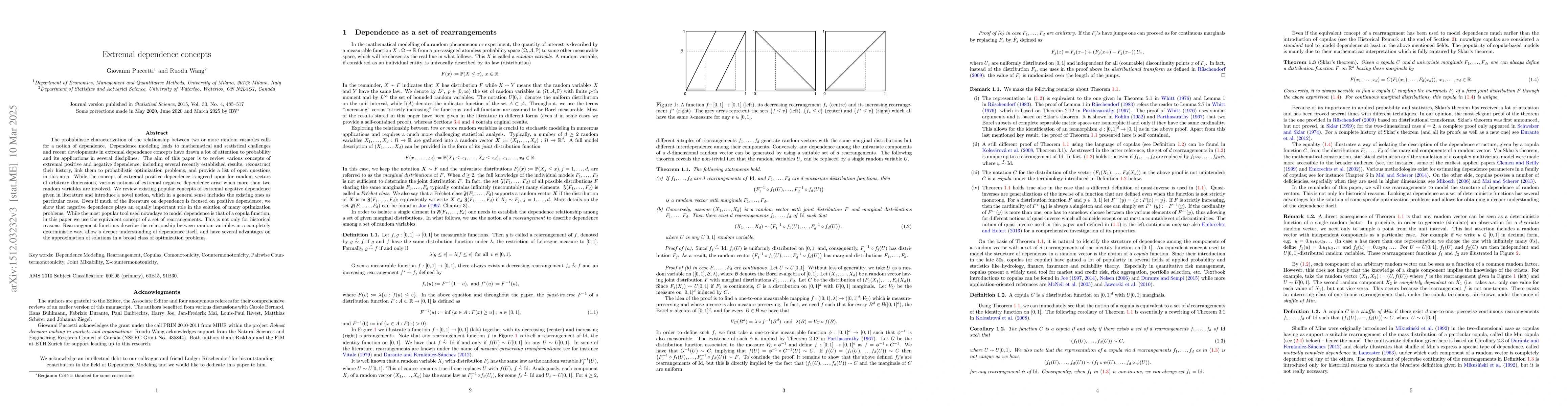

The probabilistic characterization of the relationship between two or more random variables calls for a notion of dependence. Dependence modeling leads to mathematical and statistical challenges, an...

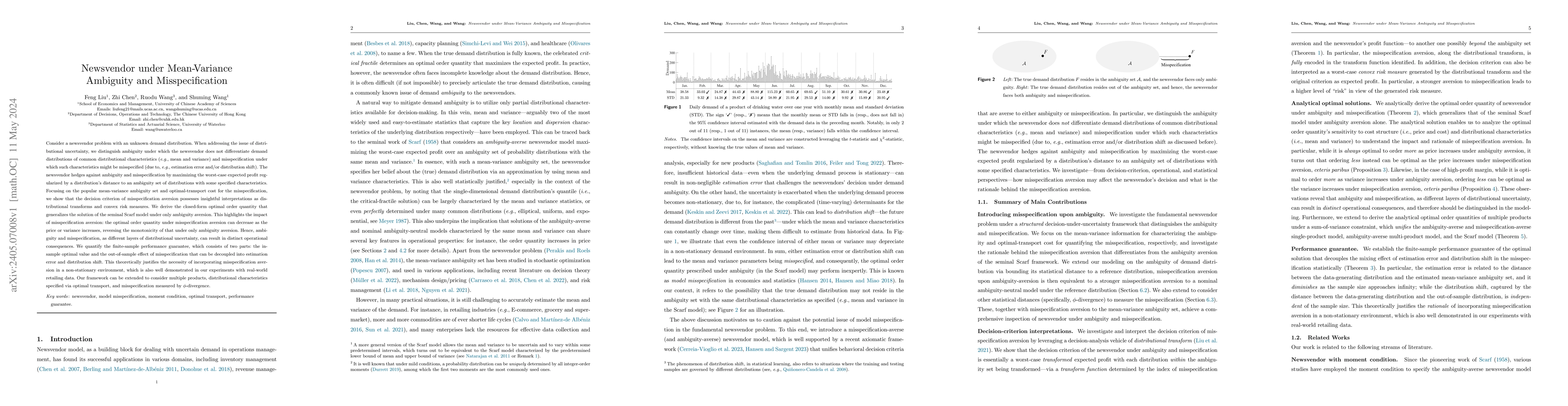

Consider a newsvendor problem with an unknown demand distribution. When addressing the issue of distributional uncertainty, we distinguish ambiguity under which the newsvendor does not differentiate...

We obtain several inequalities on the generalized means of dependent p-values. In particular, the weighted harmonic mean of p-values is strictly sub-uniform under several dependence assumptions of p...

We study stochastic dominance between portfolios of independent and identically distributed (iid) extremely heavy-tailed (i.e., infinite-mean) Pareto random variables. With the notion of majorizatio...

We introduce a novel axiom of co-loss aversion for a preference relation over the space of acts, represented by measurable functions on a suitable measurable space. This axiom means that the decisio...

We study the problem of choosing the copula when the marginal distributions of a random vector are not all continuous. Inspired by three motivating examples including simulation from copulas, stress...

Tail risk measures are fully determined by the distribution of the underlying loss beyond its quantile at a certain level, with Value-at-Risk and Expected Shortfall being prime examples. They are in...

The classical theory of efficient allocations of an aggregate endowment in a pure-exchange economy has hitherto primarily focused on the Pareto-efficiency of allocations, under the implicit assumpti...

We establish a profound connection between coherent risk measures, a prominent object in quantitative finance, and uniform integrability, a fundamental concept in probability theory. Instead of work...

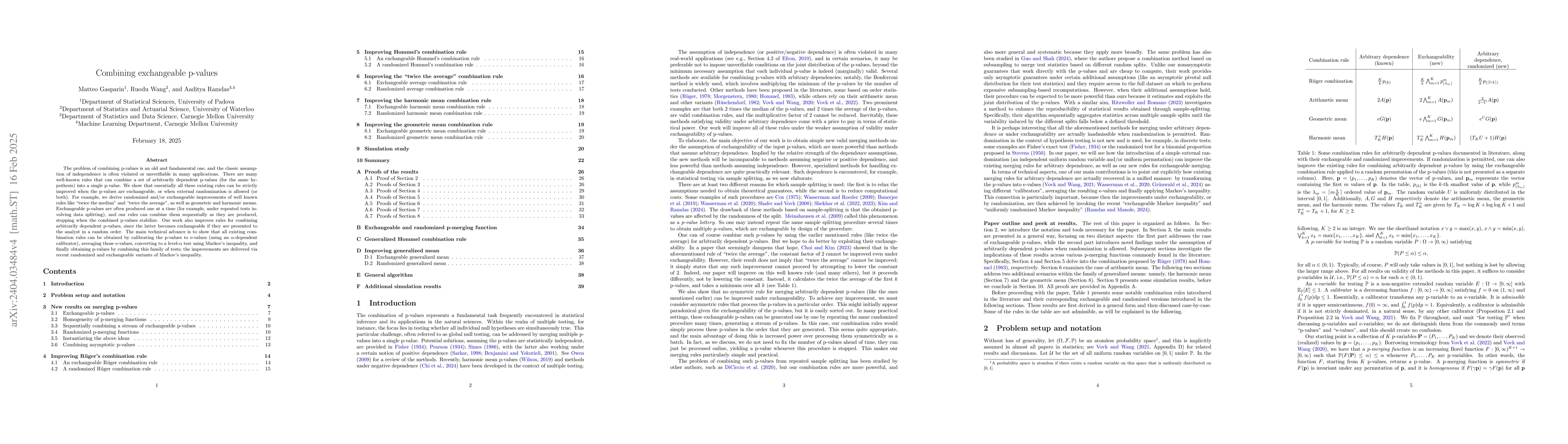

The problem of combining p-values is an old and fundamental one, and the classic assumption of independence is often violated or unverifiable in many applications. There are many well-known rules th...

We study the optimal decisions of agents who aim to minimize their risks by allocating their positions over extremely heavy-tailed (i.e., infinite-mean) and possibly dependent losses. The loss distr...

Max-stability is the property that taking a maximum between two inputs results in a maximum between two outputs. We investigate max-stability with respect to first-order stochastic dominance, the mo...

We provide a new characterization of second-order stochastic dominance, also known as increasing concave order. The result has an intuitive interpretation that adding a risk with negative expected v...

We introduce the concept of partial law invariance, generalizing the concepts of law invariance and probabilistic sophistication widely used in decision theory, as well as statistical and financial ...

We analyze the problem of optimally sharing risk using allocations that exhibit counter-monotonicity, the most extreme form of negative dependence. Counter-monotonic allocations take the form of eit...

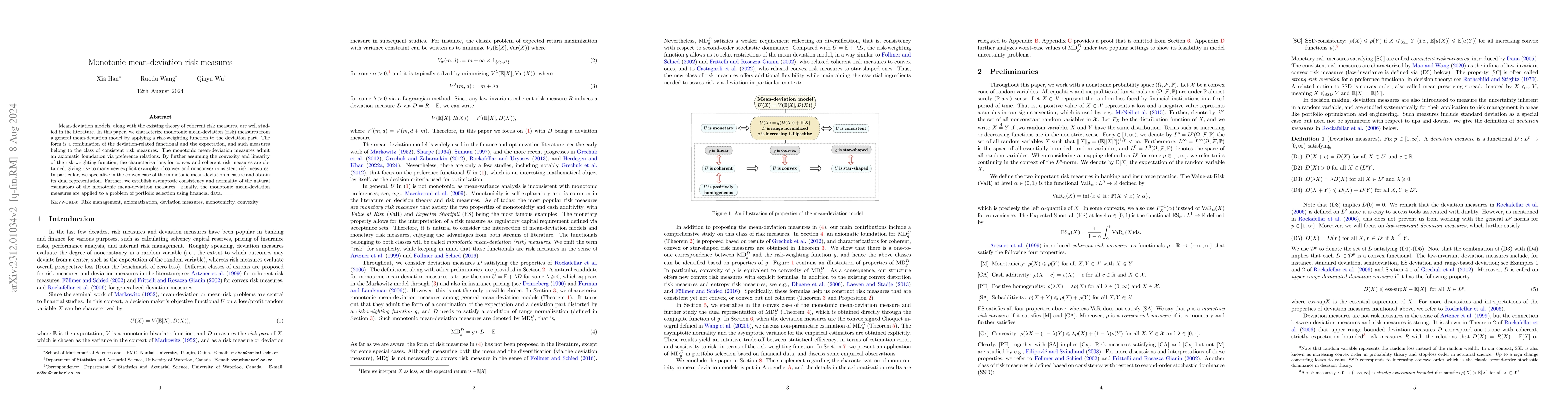

Mean-deviation models, along with the existing theory of coherent risk measures, are well studied in the literature. In this paper, we characterize monotonic mean-deviation (risk) measures from a ge...

We provide a new foundation of risk aversion by showing that the propension to exploit insurance opportunities fully describes this attitude. Our foundation, which applies to any probabilistically s...

In this paper, we establish a mathematical duality between utility transforms and probability distortions. These transforms play a central role in decision under risk by forming the foundation for t...

Classic optimal transport theory is built on minimizing the expected cost between two given distributions. We propose the framework of distorted optimal transport by minimizing a distorted expected ...

A useful property of independent samples is that their correlation remains the same after applying marginal transforms. This invariance property plays a fundamental role in statistical inference, bu...

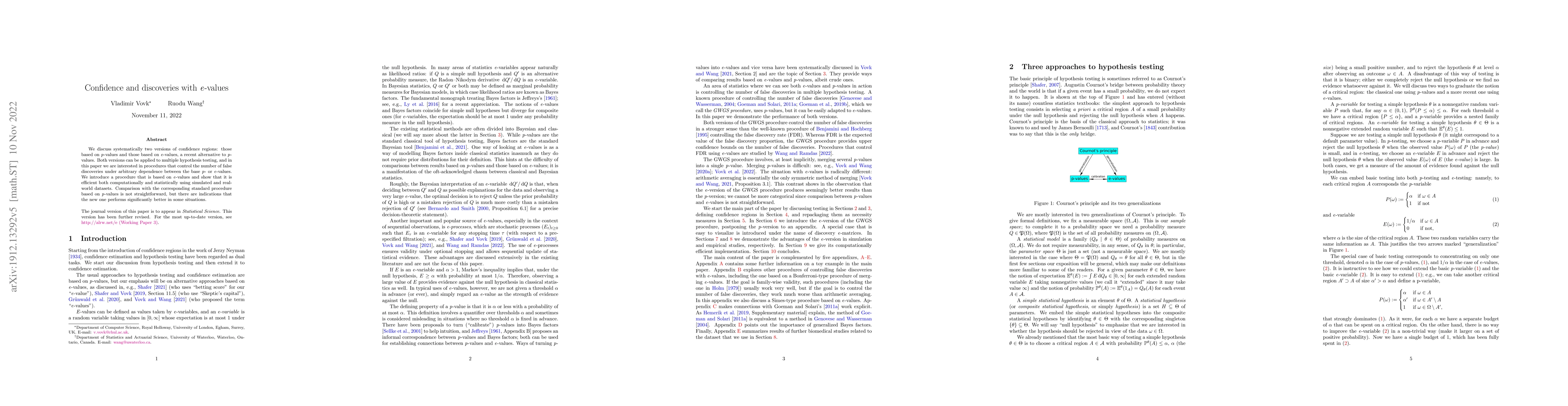

Given a composite null $ \mathcal P$ and composite alternative $ \mathcal Q$, when and how can we construct a p-value whose distribution is exactly uniform under the null, and stochastically smaller...

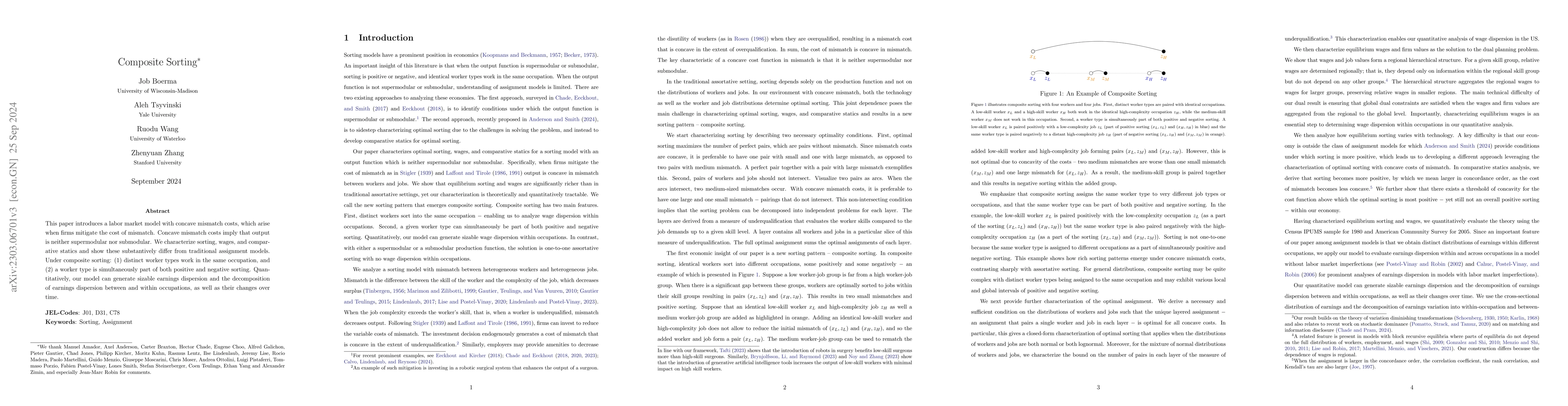

We propose a new sorting framework: composite sorting. Composite sorting comprises of (1) distinct worker types assigned to the same occupation, and (2) a given worker type simultaneously being part...

We systematically study pairwise counter-monotonicity, an extremal notion of negative dependence. A stochastic representation and an invariance property are established for this dependence structure...

We address the problem of sharing risk among agents with preferences modelled by a general class of comonotonic additive and law-based functionals that need not be either monotone or convex. Such fu...

We address the problem of testing conditional mean and conditional variance for non-stationary data. We build e-values and p-values for four types of non-parametric composite hypotheses with specifi...

The diversification quotient (DQ) is recently introduced for quantifying the degree of diversification of a stochastic portfolio model. It has an axiomatic foundation and can be defined through a pa...

The multiple testing literature has primarily dealt with three types of dependence assumptions between p-values: independence, positive regression dependence, and arbitrary dependence. In this paper...

It is well known that martingale transport plans between marginals $\mu\neq\nu$ are never given by Monge maps -- with the understanding that the map is over the first marginal $\mu$, or forward in t...

In the recent Basel Accords, the Expected Shortfall (ES) replaces the Value-at-Risk (VaR) as the standard risk measure for market risk in the banking sector, making it the most important risk measur...

The notion of an e-value has been recently proposed as a possible alternative to critical regions and p-values in statistical hypothesis testing. In this paper we consider testing the nonparametric ...

We propose \emph{Choquet regularizers} to measure and manage the level of exploration for reinforcement learning (RL), and reformulate the continuous-time entropy-regularized RL problem of Wang et a...

We find the perhaps surprising inequality that the weighted average of independent and identically distributed Pareto random variables with infinite mean is larger than one such random variable in t...

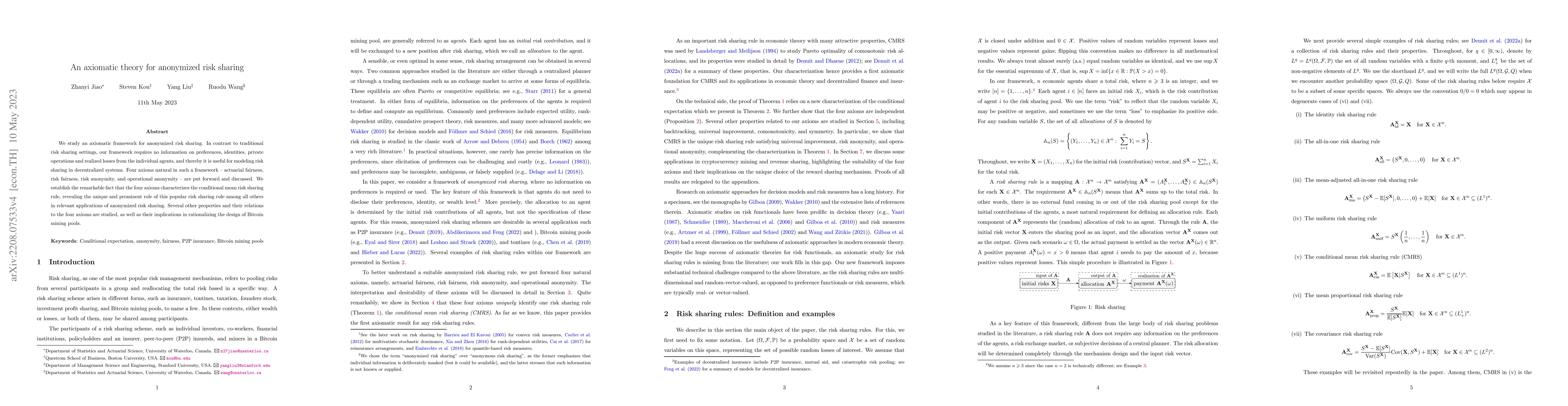

We study an axiomatic framework for anonymized risk sharing. In contrast to traditional risk sharing settings, our framework requires no information on preferences, identities, private operations an...

We establish the first axiomatic theory for diversification indices using six intuitive axioms: non-negativity, location invariance, scale invariance, rationality, normalization, and continuity. The...

We study how to combine p-values and e-values, and design multiple testing procedures where both p-values and e-values are available for every hypothesis. Our results provide a new perspective on mu...

A joint mix is a random vector with a constant component-wise sum. The dependence structure of a joint mix minimizes some common objectives such as the variance of the component-wise sum, and it is ...

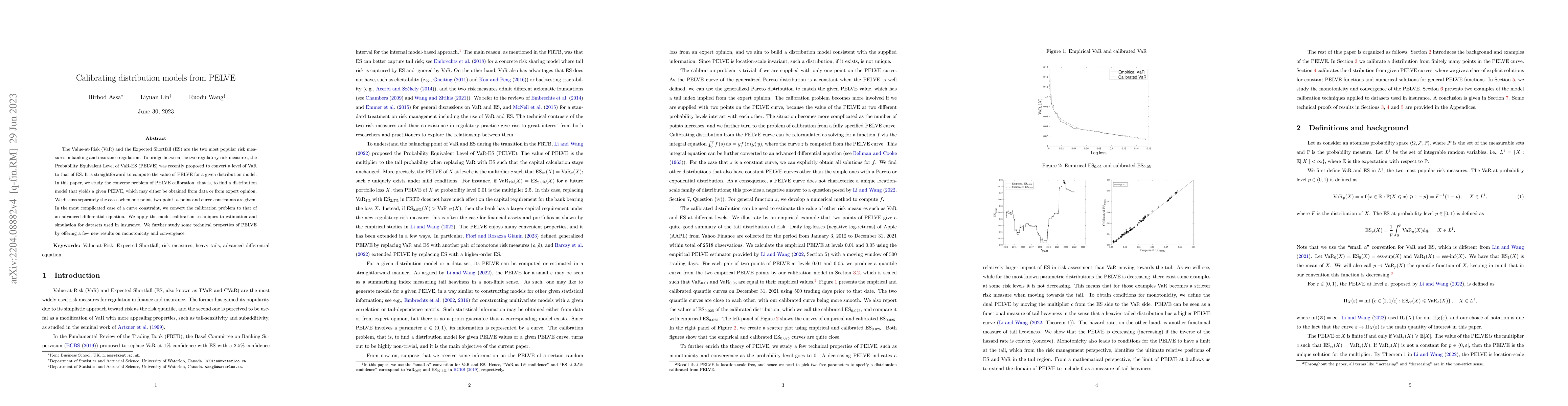

The Value-at-Risk (VaR) and the Expected Shortfall (ES) are the two most popular risk measures in banking and insurance regulation. To bridge between the two regulatory risk measures, the Probabilit...

Suppose that one can construct a valid $(1-\delta)$-confidence interval (CI) for each of $K$ parameters of potential interest. If a data analyst uses an arbitrary data-dependent criterion to select ...

The celebrated Expected Shortfall (ES) optimization formula implies that ES at a fixed probability level is the minimum of a linear real function plus a scaled mean excess function. We establish a r...

We collect self-contained elementary proofs of four results in the literature on the false discovery rate of the Benjamini-Hochberg (BH) procedure for independent or positive-regression dependent p-...

We introduce a new approach for prudent risk evaluation based on stochastic dominance, which will be called the model aggregation (MA) approach. In contrast to the classic worst-case risk (WR) appro...

We propose a general framework of mass transport between vector-valued measures, which will be called simultaneous optimal transport (SOT). The new framework is motivated by the need to transport re...

In the literature of risk measures, cash subadditivity was proposed to replace cash additivity, motivated by the presence of stochastic or ambiguous interest rates and defaultable contingent claims....

A risk analyst assesses potential financial losses based on multiple sources of information. Often, the assessment does not only depend on the specification of the loss random variable but also vari...

The Expected Shortfall (ES) is one of the most important regulatory risk measures in finance, insurance, and statistics, which has recently been characterized via sets of axioms from perspectives of...

Expected Shortfall (ES, also known as CVaR) is the most important coherent risk measure in finance, insurance, risk management, and engineering. Recently, Wang and Zitikis (2021) put forward four ec...

In bandit multiple hypothesis testing, each arm corresponds to a different null hypothesis that we wish to test, and the goal is to design adaptive algorithms that correctly identify large set of in...

In this paper, we study an optimal insurance problem for a risk-averse individual who seeks to maximize the rank-dependent expected utility (RDEU) of her terminal wealth, and insurance is priced via...

We study the aggregation of two risks when the marginal distributions are known and the dependence structure is unknown, under the additional constraint that one risk is smaller than or equal to the...

In this paper monetary risk measures that are positively superhomogeneous, called star-shaped risk measures, are characterized and their properties studied. The measures in this class, which arise w...

We present a general framework for a comparative theory of variability measures, with a particular focus on the recently introduced one-parameter families of inter-Expected Shortfall differences and...

Optimization of distortion riskmetrics with distributional uncertainty has wide applications in finance and operations research. Distortion riskmetrics include many commonly applied risk measures an...

We introduce the notion of p*-values (p*-variables), which generalizes p-values (p-variables) in several senses. The new notion has four natural interpretations: operational, probabilistic, Bayesian...

E-values have gained attention as potential alternatives to p-values as measures of uncertainty, significance and evidence. In brief, e-values are realized by random variables with expectation at mo...

Methods of merging several p-values into a single p-value are important in their own right and widely used in multiple hypothesis testing. This paper is the first to systematically study the admissi...

Aggregation sets, which represent model uncertainty due to unknown dependence, are an important object in the study of robust risk aggregation. In this paper, we investigate ordering relations betwe...

Quantile aggregation with dependence uncertainty has a long history in probability theory with wide applications in finance, risk management, statistics, and operations research. Using a recent resu...

We introduce and study the main properties of a class of convex risk measures that refine Expected Shortfall by simultaneously controlling the expected losses associated with different portions of t...

We study the problem of merging sequential or independent e-values into one e-value or e-process. We describe a class of e-value merging functions via martingales and show that it dominates all merg...

We introduce a constrained optimal transport problem where origins $x$ can only be transported to destinations $y\geq x$. Our statistical motivation is to describe the sharp upper bound for the vari...

We discuss systematically two versions of confidence regions: those based on p-values and those based on e-values, a recent alternative to p-values. Both versions can be applied to multiple hypothes...

Multiple testing of a single hypothesis and testing multiple hypotheses are usually done in terms of p-values. In this paper we replace p-values with their natural competitor, e-values, which are cl...

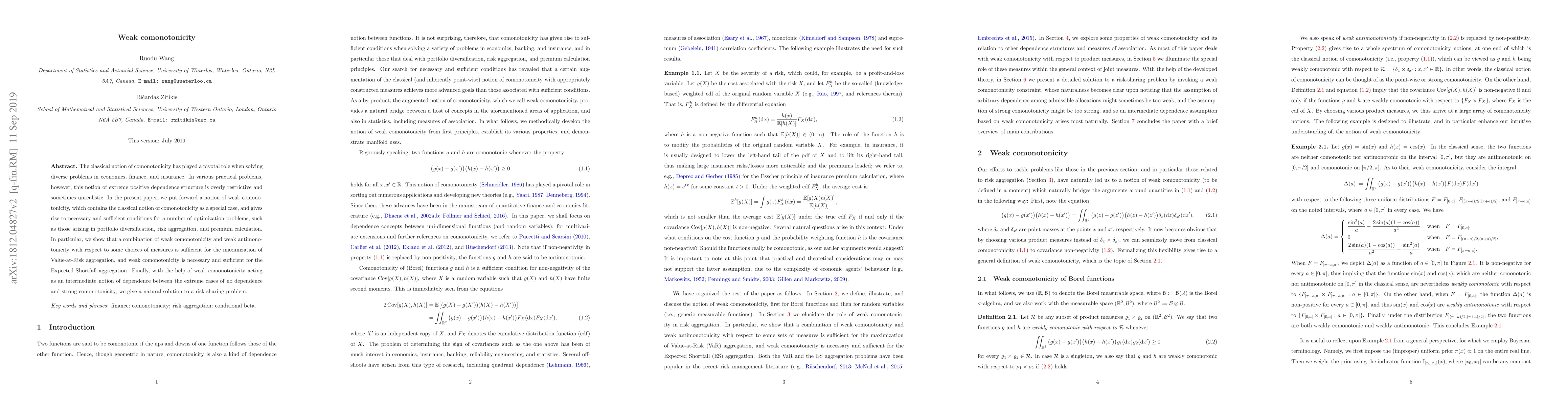

The classical notion of comonotonicity has played a pivotal role when solving diverse problems in economics, finance, and insurance. In various practical problems, however, this notion of extreme po...

In this paper, we analyze the set of all possible aggregate distributions of the sum of standard uniform random variables, a simply stated yet challenging problem in the literature of distributions ...

We study issues of robustness in the context of Quantitative Risk Management and Optimization. We develop a general methodology for determining whether a given risk measurement related optimization ...

Risk measures such as Expected Shortfall (ES) and Value-at-Risk (VaR) have been prominent in banking regulation and financial risk management. Motivated by practical considerations in the assessment...

Given two random variables taking values in a bounded interval, we study whether one dominates the other in higher-order stochastic dominance depends on the reference interval in the model setting. We...

This book is written to offer a humble, but unified, treatment of e-values in hypothesis testing. The book is organized into three parts: Fundamental Concepts, Core Ideas, and Advanced Topics. The fir...

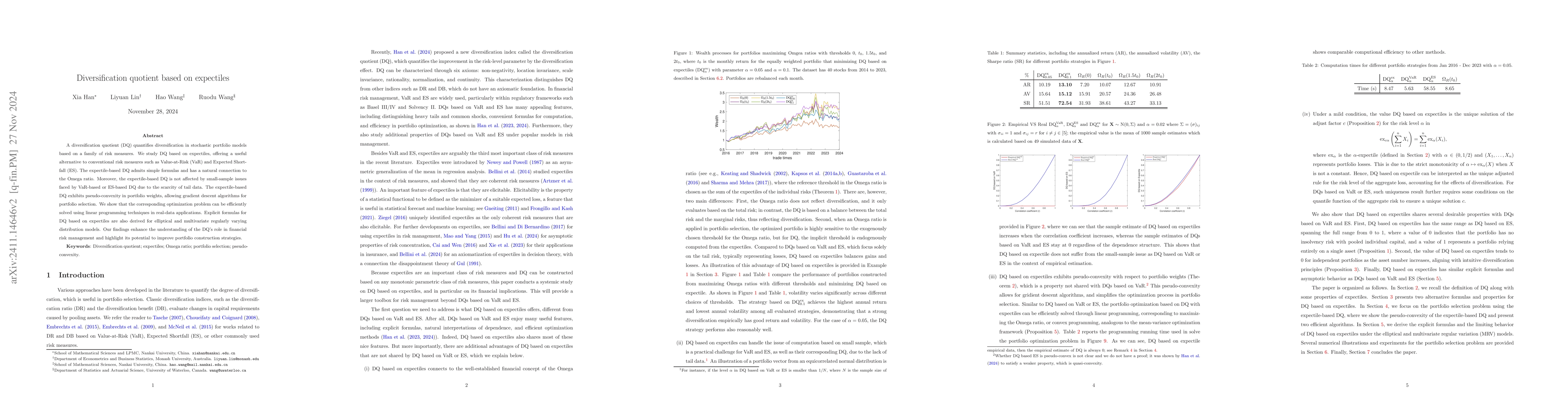

A diversification quotient (DQ) quantifies diversification in stochastic portfolio models based on a family of risk measures. We study DQ based on expectiles, offering a useful alternative to conventi...

We study risk sharing among agents with preferences modeled by heterogeneous distortion risk measures, who are not necessarily risk averse. Pareto optimality for agents using risk measures is often st...

In statistical analysis, many classic results require the assumption that models have finite mean or variance, including the most standard versions of the laws of large numbers and the central limit t...

In risk-sharing markets with aggregate uncertainty, characterizing Pareto-optimal allocations when agents might not be risk averse is a challenging task, and the literature has only provided limited e...

We explicitly define the notion of (exact or approximate) compound e-values which have been implicitly presented and extensively used in the recent multiple testing literature. We show that every FDR ...

We prove that the only admissible way of merging e-values is to use a weighted arithmetic average. This result completes the picture of merging methods for e-values, and generalizes the result of Vovk...

The rejection threshold used for e-values and e-processes is by default set to $1/\alpha$ for a guaranteed type-I error control at $\alpha$, based on Markov's and Ville's inequalities. This threshold ...

Choquet capacities and integrals are central concepts in decision making under ambiguity or model uncertainty, pioneered by Schmeidler. Motivated by risk optimization problems for quantiles under ambi...

We obtain a full characterization of consistency with respect to higher-order stochastic dominance within the rank-dependent utility model. Different from the results in the literature, we do not assu...

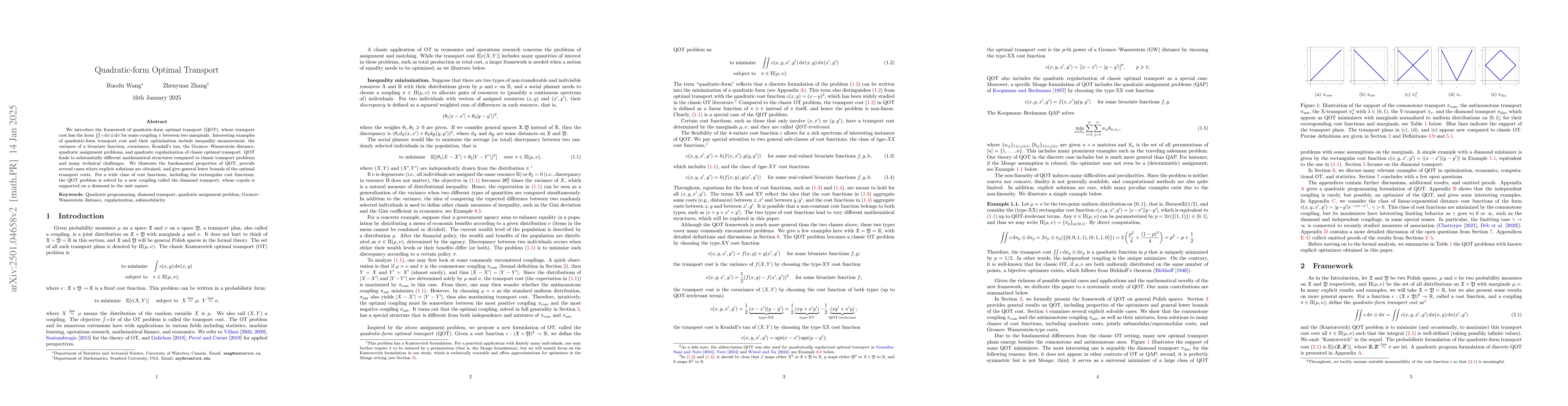

We introduce the framework of quadratic-form optimal transport (QOT), whose transport cost has the form $\iint c\,\mathrm{d}\pi \otimes\mathrm{d}\pi$ for some coupling $\pi$ between two marginals. Int...

Many results on the convex order in the literature were stated for random variables with finite mean. For instance, a fundamental result in dependence modeling is that the sum of a pair of random rand...

Credit ratings are widely used by investors as a screening device. We introduce and study several natural notions of risk consistency that promote prudent investment decisions in the framework of Choq...

Law-invariant functionals are central to risk management and assign identical values to random prospects sharing the same distribution under an atomless reference probability measure. This measure is ...

This paper recasts Gul (1991)'s theory of disappointment aversion in a Savage framework, with general outcomes, new explicit axioms of disappointment aversion, and novel explicit representations. Thes...

Heavy-tailed combination tests, such as the Cauchy combination test and harmonic mean p-value method, are widely used for testing global null hypotheses by aggregating dependent p-values. However, the...

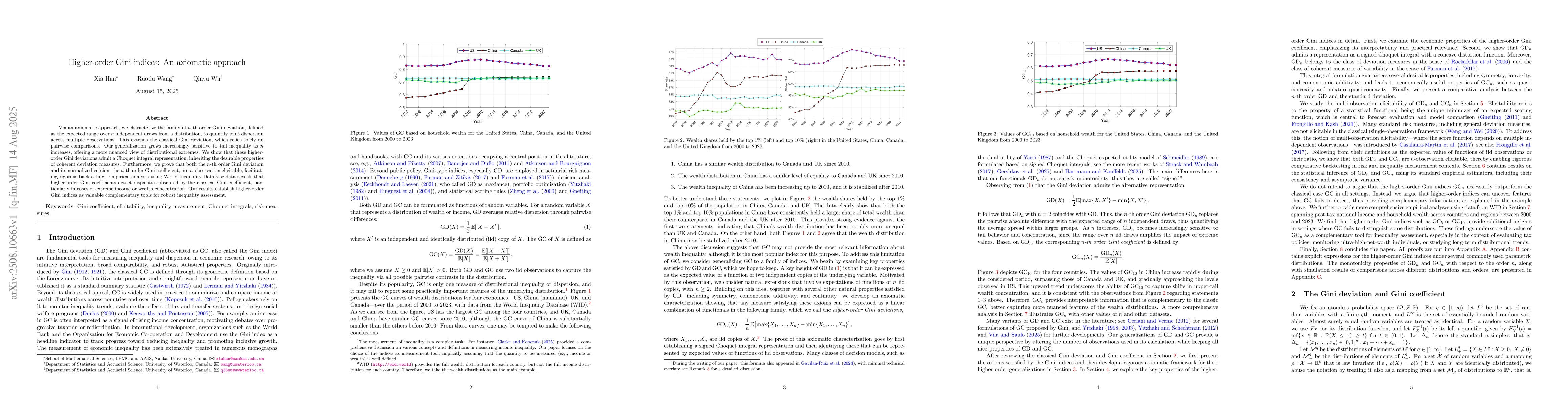

Via an axiomatic approach, we characterize the family of n-th order Gini deviation, defined as the expected range over n independent draws from a distribution, to quantify joint dispersion across mult...

We propose a new decision model under ambiguity, called the Choquet rank-dependent utility model. The model extends the Choquet expected utility model by allowing for the reduction to the rank-depende...

A common theme underlying many problems in statistics and economics involves the determination of a systematic method of selecting a joint distribution consistent with a specified list of categorical ...

We study Pareto-optimal risk sharing in economies with heterogeneous attitudes toward risk, where agents' preferences are modeled by distortion risk measures. Building on comonotonic and counter-monot...

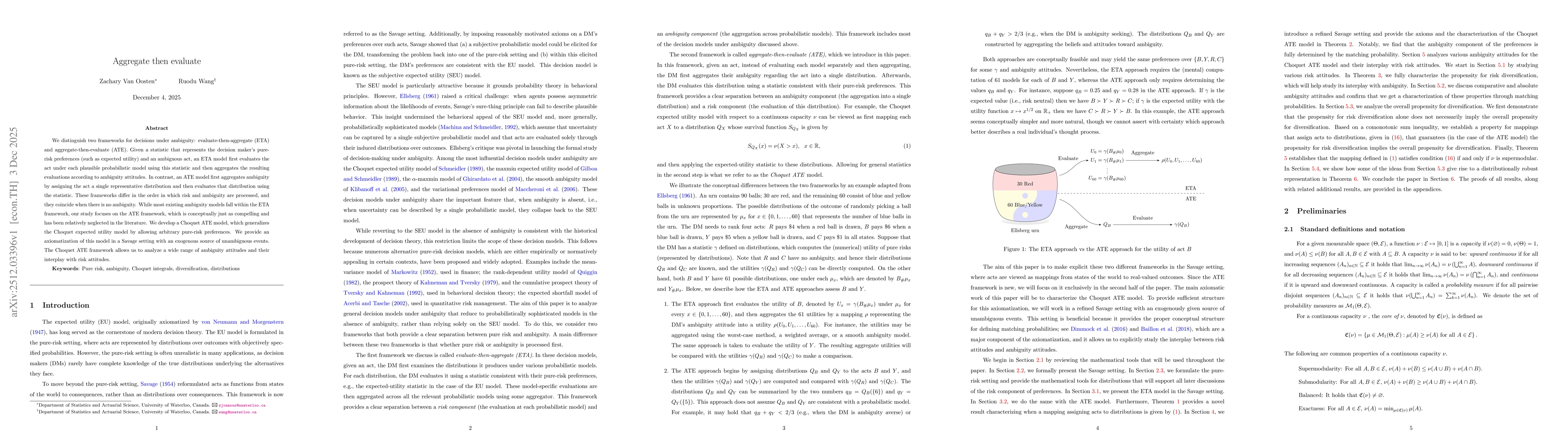

We distinguish two frameworks for decisions under ambiguity: evaluate-then-aggregate (ETA) and aggregate-then-evaluate (ATE). Given a statistic that represents the decision maker's pure-risk preferenc...

Risk aversion and insurance are two prominent and interconnected concepts in economics and finance. To explore their fundamental connection, we introduce risk-insurance parity, which associates variou...

The Lambda Value-at-Risk (Lambda$-VaR) is a generalization of the Value-at-Risk (VaR), which has been actively studied in quantitative finance. Over the past two decades, the Expected Shortfall (ES) h...

Portfolio diversification is a cornerstone of modern finance, while risk aversion is central to decision theory; both concepts are long-standing and foundational. We investigate their connections by s...

We study the problem of online monotone density estimation, where density estimators must be constructed in a predictable manner from sequentially observed data. We propose two online estimators: an o...

Watermarking for large language models (LLMs) has emerged as an effective tool for distinguishing AI-generated text from human-written content. Statistically, watermark schemes induce dependence betwe...

We study submodularity for law-invariant functionals, with special attention to convex risk measures. Expected losses are modular, and certainty equivalents are submodular if and only if the underlyin...

Risk forecasts in financial regulation and internal management are calculated through historical data. The unknown structural changes of financial data poses a substantial challenge in selecting an ap...

We show that a class of optimized e-value combinations, arising from a standard construction of e-processes, remains valid even when the tuning parameter is optimized based on the data. This result ho...

This note extends conformal e-prediction to cover the case where there is observed confounding between the random object $X$ and its label $Y$. We consider both the case where the observed data is IID...

We study distributionally robust quantile regression using type-$p$ Wasserstein ambiguity sets. We derive a closed-form expression for the worst-case quantile regression loss under general $p$-Wassers...

After the seminal Benjamini-Hochberg (BH) procedure for controlling the false discovery rate (FDR) was proposed, dozens of papers have attempted to improve its power by adapting to the unknown proport...

We derive confidence intervals and confidence sequences for causal effects in situations where the back-door or front-door criteria are applicable. Our tightest confidence intervals hold in the standa...

Value-at-Risk (VaR) is a standard regulatory risk measure, and its failure of subadditivity is well known. Much less appreciated is that for sufficiently heavy-tailed losses, VaR can be superadditive ...

The false discovery rate (FDR) is the most widely used error metric in modern multiple testing. We provide the first comprehensive analysis of the admissibility of e-value-based procedures with FDR co...

Experiments may, by design, prevent one from observing on a single subject both the response to a treatment and to its absence. Because of this, marginal distributions for both cases may be observable...

Given observations $\mathbf x=(x_1,\dots,x_n)$, Gaffke (2005) defined \[ K_n(\mathbf x)=\mathbb{P}_{\mathbf D}\!\left\{\sum_{i=1}^n x_iD_i\le 1\right\}, \qquad (D_0,D_1,\ldots,D_n)\sim\mathrm{Dirichle...