Xinbing Kong

9 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Manifold Principle Component Analysis for Large-Dimensional Matrix Elliptical Factor Model

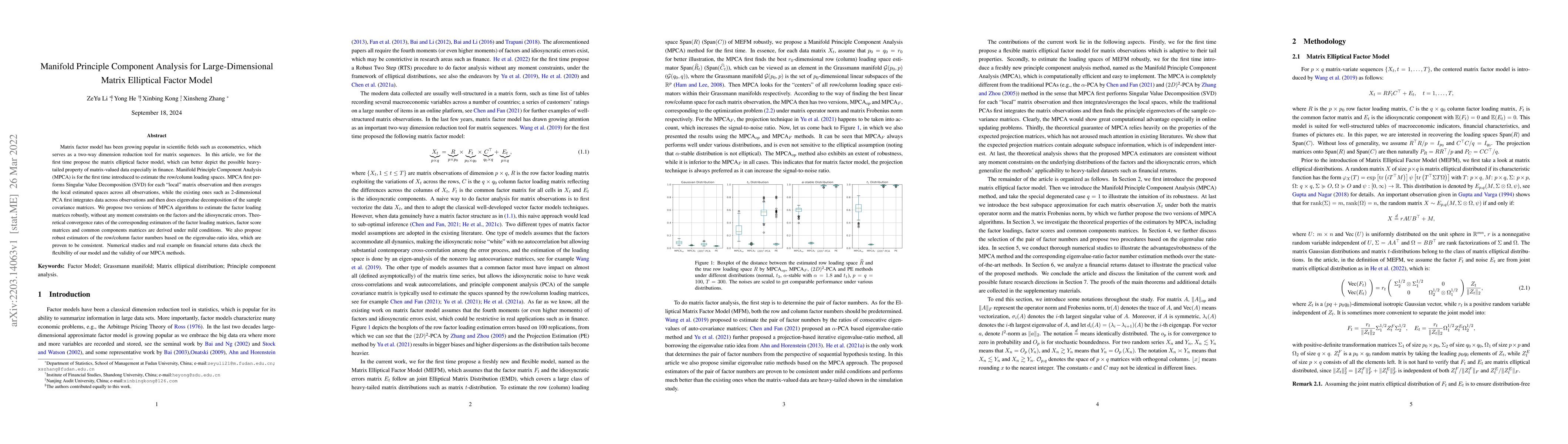

Matrix factor model has been growing popular in scientific fields such as econometrics, which serves as a two-way dimension reduction tool for matrix sequences. In this article, we for the first tim...

Matrix Factor Analysis: From Least Squares to Iterative Projection

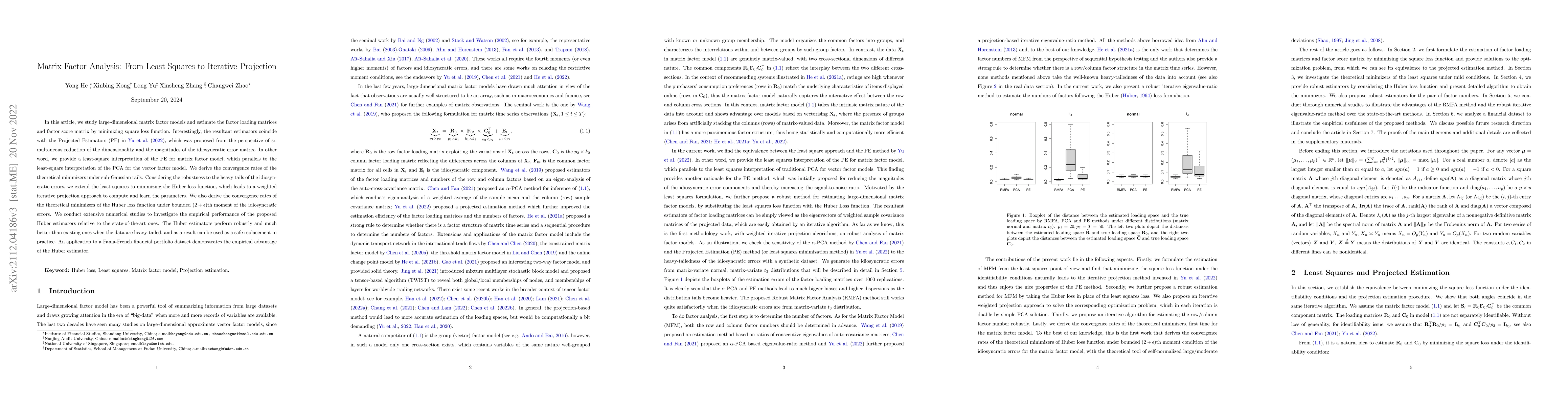

In this article, we study large-dimensional matrix factor models and estimate the factor loading matrices and factor score matrix by minimizing square loss function. Interestingly, the resultant est...

Large-dimensional Factor Analysis without Moment Constraints

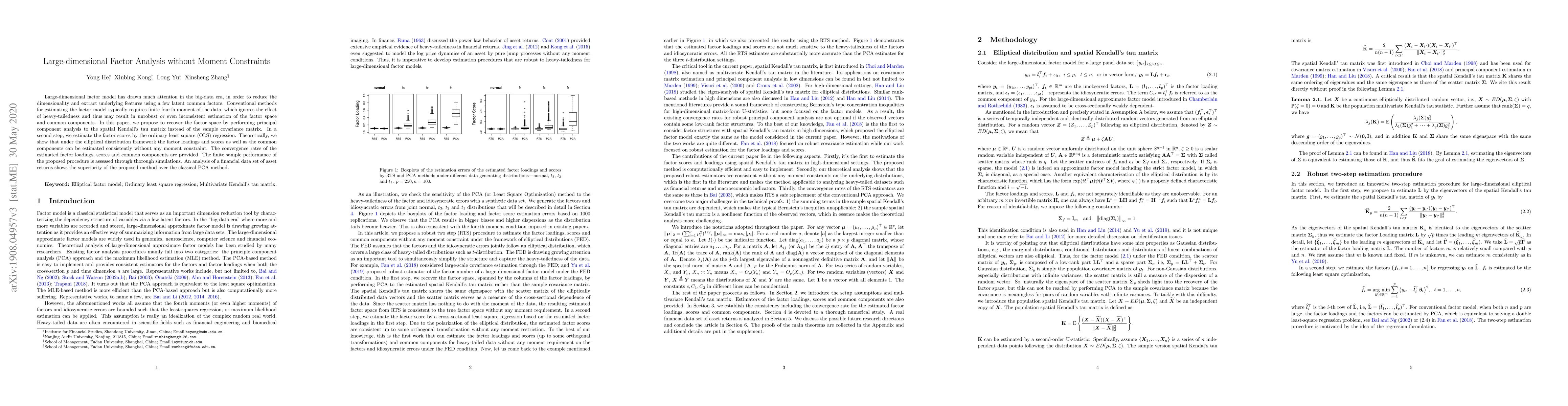

Large-dimensional factor model has drawn much attention in the big-data era, in order to reduce the dimensionality and extract underlying features using a few latent common factors. Conventional met...

Generalized Matrix Factor Model

This article introduces a nonlinear generalized matrix factor model (GMFM) that allows for mixed-type variables, extending the scope of linear matrix factor models (LMFM) that are so far limited to ha...

High-Dimensional Binary Variates: Maximum Likelihood Estimation with Nonstationary Covariates and Factors

This paper introduces a high-dimensional binary variate model that accommodates nonstationary covariates and factors, and studies their asymptotic theory. This framework encompasses scenarios where si...

Data Synchronization at High Frequencies

Asynchronous trading in high-frequency financial markets introduces significant biases into econometric analysis, distorting risk estimates and leading to suboptimal portfolio decisions. Existing sync...

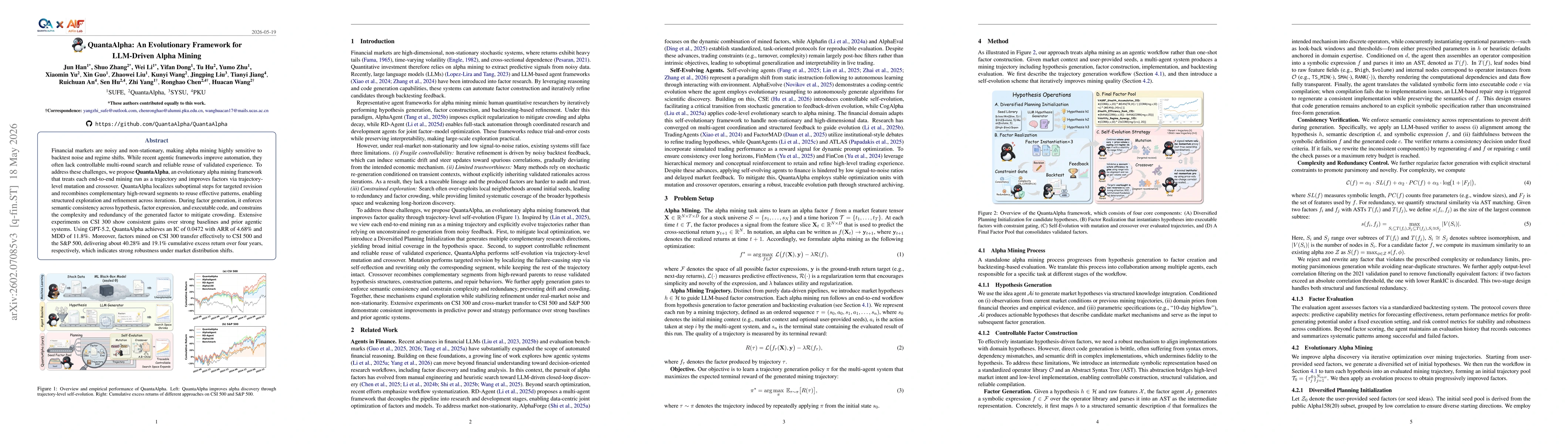

QuantaAlpha: An Evolutionary Framework for LLM-Driven Alpha Mining

Financial markets are noisy and non-stationary, making alpha mining highly sensitive to noise in backtesting results and sudden market regime shifts. While recent agentic frameworks improve alpha mini...

Tucker Diffusion Model for High-dimensional Tensor Generation

Statistical inference on large-dimensional tensor data has been extensively studied in the literature and widely used in economics, biology, machine learning, and other fields, but how to generate a s...

Expected Shortfall Panel Regression

Expected Shortfall (ES) is a coherent measure of tail risk that captures the average loss beyond a quantile threshold. Despite the growing literature on ES regression conditional on covariates, no exi...