Background

Quantitative alpha mining operates in financial environments characterized by high dimensionality, non-stationarity, and heavy-tailed returns. Traditional factor libraries and purely data-driven models often overfit to regime-specific patterns and degrade when market dynamics shift. Recent LLM-driven agentic systems promise automation and interpretability but struggle with drift, lack of traceable lineage, and limited exploration that fails to escape local optima. The need is for a framework that can (i) explore broadly, (ii) preserve validated reasoning across iterations, and (iii) generate interpretable, implementable factors that generalize across markets.

Problem / Research Question

The central question is how to design an alpha mining framework that remains controllable and trustworthy over multi-round exploration in the presence of backtest noise and regime change. Specifically, how can we (a) diversify the initial hypotheses to avoid premature convergence, (b) revise factors without breaking semantic coherence, and (c) recombine high-quality ideas to reuse proven patterns while maintaining interpretability and computational efficiency?

Innovation / Contribution

QuantaAlpha introduces a trajectory-centric evolutionary paradigm for alpha mining. Its key contributions are:

- Diversified Planning Initialization that creates complementary market hypotheses to expand the search frontier.

- Controllable Factor Construction via an intermediate symbolic representation (operator library and AST) that ties hypotheses to transparent, verifiable factor expressions and generated code.

- Consistency Verification that ensures alignment among hypothesis, symbolic form, and implementation, with regeneration when necessary.

- Complexity and Redundancy Controls that enforce parsimony and novelty, reducing crowding and drift.

- Evolutionary Alpha Mining with Mutation and Crossover operating on mining trajectories, enabling trajectory-level self-evolution and reuse of validated patterns.

- A standardized backtesting protocol and a final factor pool that consolidates validated, non-redundant factors for downstream trading.

- Demonstrated cross-market transferability and robustness under regime shifts, surpassing both traditional baselines and prior agentic systems.

Methodology / Approach

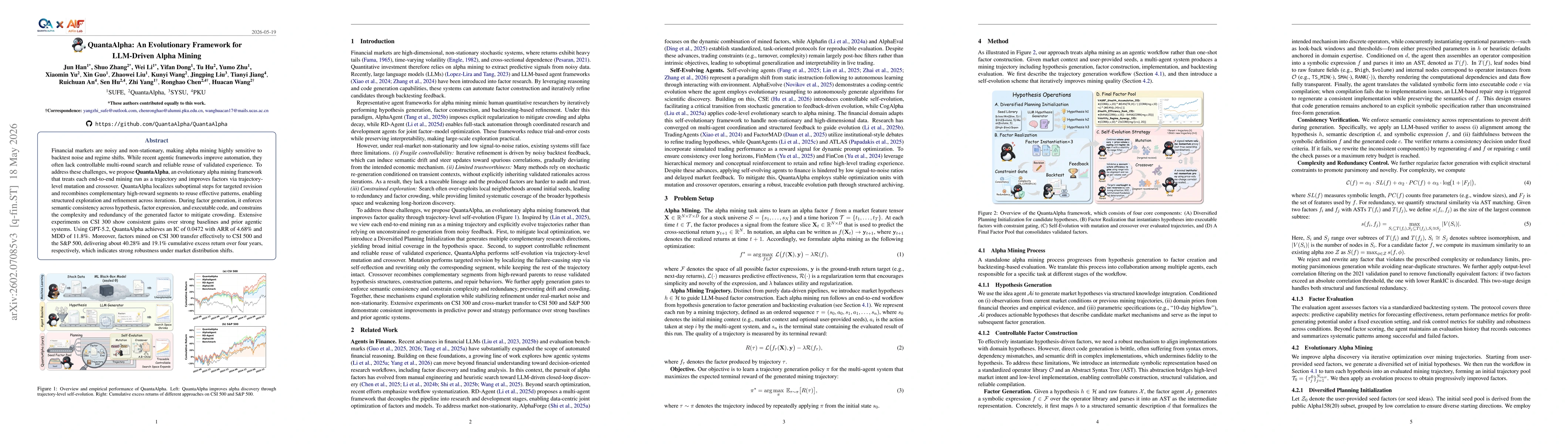

The approach treats an end-to-end mining run as a trajectory τ = (s0, a0, s1, a1, ..., sn) whose terminal reward fτ is derived from the produced factor. The methodology comprises four core components:

- Diversified Planning Initialization: An inspiration agent proposes multiple market hypotheses by blending domain priors, market observations, and parameterized constructs; each hypothesis seeds a complete mining workflow to produce an initial trajectory.

- Controllable Factor Construction: Given a hypothesis, a factor agent creates a symbolic expression over a standardized operator library; this is parsed into an AST and compiled to executable code with a repair step if needed. A separate verifier checks semantic fidelity across h, d, f, and c.

- Complexity and Redundancy Control: The framework enforces symbol length, base features, and a measured redundancy via AST isomorphism; factors exceeding thresholds are rewritten.

- Self-Evolution (Mutation and Crossover): Mutation localizes and rewrites the most consequential sub-trajectory to fix failures, while Crossover recombines segments from high-reward parents to synthesize new trajectories. A final factor pool stores diverse, validated factors.

The experimental setup uses CSI 300 data with cross-market validation to CSI 500 and S&P 500, with backtesting conducted in a standardized Qlib-based pipeline. LLM backbones include multiple options, with GPT-5.2 yielding the strongest performance in reported results.

Experiments / Evaluation

The authors benchmark QuantaAlpha against four baselines: traditional ML models, deep learning time-series models, classical factor libraries, and other LLM-based agents. They measure factor predictive power (IC, Rank IC, ICIR, Rank ICIR) and strategy performance (ARR, IR, MDD, CR), computed on excess returns after costs. Experiments cover CSI 300, with transfer tests to CSI 500 and S&P 500.

Across networks and baselines, QuantaAlpha consistently improves factor predictiveness and strategy outcomes, with the GPT-5.2 run achieving IC = 0.1501 and ARR = 27.75% with MDD = 7.98%. Ablation studies show planning initialization contributes to stable performance, while mutation drives the largest lift in predictive power; crossover further enhances efficiency and stability. An ablation removing all three controls (semantic consistency, complexity, redundancy) degrades results, underscoring the importance of these gates.

The paper includes a case study illustrating how a representative factor evolves through crossover, showing how dual-source momentum signals can be synthesized into a coherent predictor, albeit with some trade-offs in risk metrics that call for regime-aware weighting.

Key Results

Key findings include: (1) Superior IC and Rank IC on CSI 300 relative to baselines, (2) Substantial ARR improvements and manageable MDD, (3) Notable cross-market transferability with large cumulative excess returns on CSI 500 and S&P 500, (4) Clear ablation evidence that diversification, mutation, and crossover each contribute meaningfully to performance, and (5) Evidence that trajectory-level evolution yields more stable exploration with better long-horizon performance than one-shot factor generation.

Practical Applications

QuantaAlpha provides a practical blueprint for integrating controllable, interpretable AI-driven factor mining into quantitative trading workflows. By preserving a verifiable lineage of decisions and enforcing consistency gates, it supports auditable factor development suitable for live risk management and regulatory scrutiny. The cross-market transferability suggests a path toward multi-asset factories where a single evolving framework can adapt to diverse market microstructures while maintaining a consistent factor semantics and trading protocol.

Limitations & Considerations

While the results are promising, several caveats remain. The reliance on backtests and specific market regimes means live performance under unseen shocks remains to be validated at scale. The framework’s computational demands—generating multiple trajectories, running symbolic reconstructions, and backtesting across assets—pose practical deployment considerations. The risk of overfitting to historical regime transitions, as well as sensitivity to the choice of LLM backbone and backtesting assumptions (costs, liquidity, turnover) warrants further study. Finally, integrating dynamic regime-aware weighting into the evolution objective and extending experiments to more asset classes and longer horizons raise important avenues for future work.

Discussion 0