Academic Profile

Statistics

Similar Authors

Papers on arXiv

The primary objective of this paper is to conceive and develop a new methodology to detect notable changes in liquidity within an order-driven market. We study a market liquidity model which allows ...

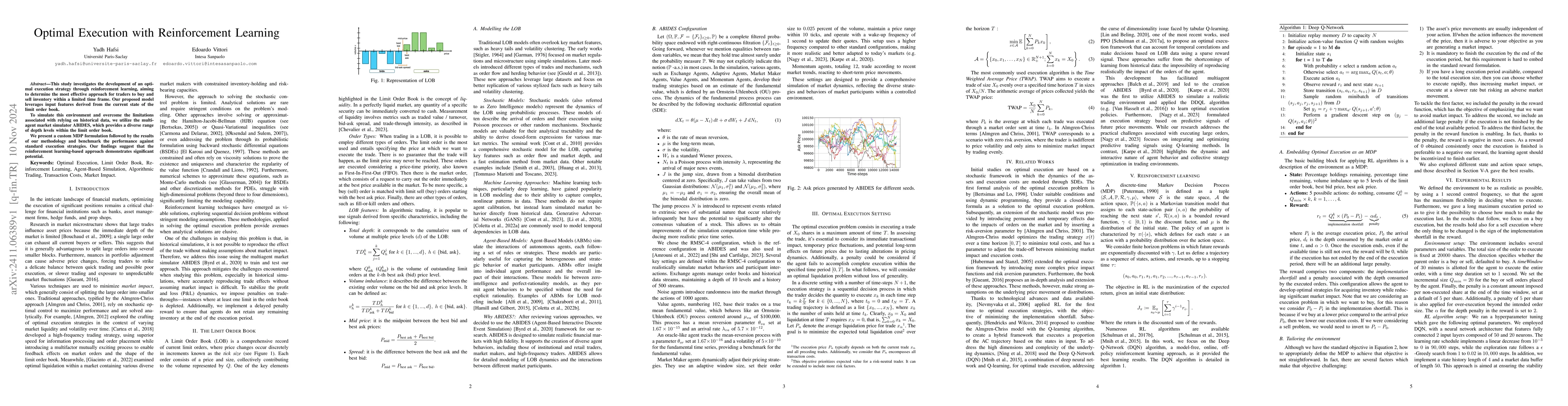

This study investigates the development of an optimal execution strategy through reinforcement learning, aiming to determine the most effective approach for traders to buy and sell inventory within a ...

We study optimal liquidation strategies under partial information for a single asset within a finite time horizon. We propose a model tailored for high-frequency trading, capturing price formation dri...

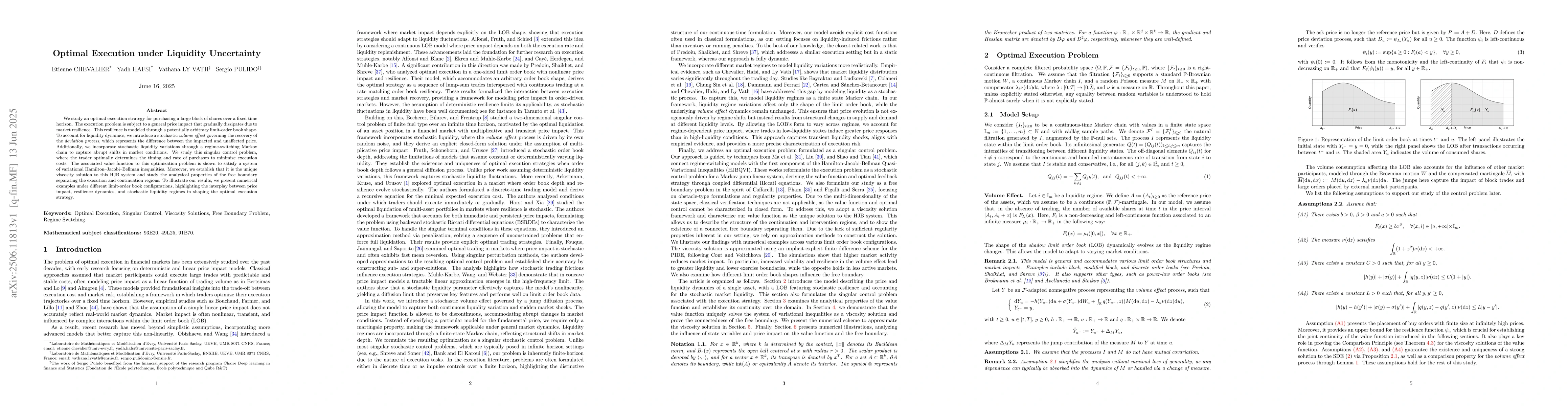

We study an optimal execution strategy for purchasing a large block of shares over a fixed time horizon. The execution problem is subject to a general price impact that gradually dissipates due to mar...

We investigate the use of Reinforcement Learning for the optimal execution of meta-orders, where the objective is to execute incrementally large orders while minimizing implementation shortfall and ma...

We develop a mixed control framework that combines absolutely continuous controls with impulse interventions subject to stochastic execution delays. The model extends current impulse control formulati...

We propose a generative framework for learning stochastic dynamics from endpoint and intermediate distributional observations. The method formulates generation as a McKean-Vlasov control problem in wh...

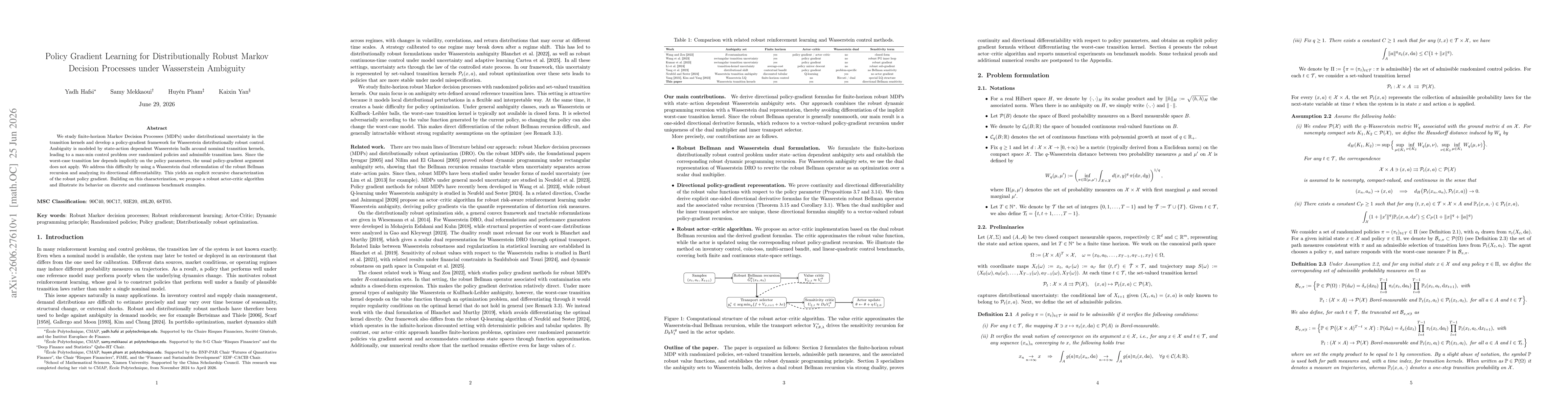

We study finite-horizon Markov Decision Processes (MDPs) under distributional uncertainty in the transition kernels and develop a policy-gradient framework for Wasserstein distributionally robust cont...