Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper offers a mathematical invention that shows how to convert integrated quantiles, which often appear in risk measures, into integrated cumulative distribution functions, which are technical...

We present a general framework for a comparative theory of variability measures, with a particular focus on the recently introduced one-parameter families of inter-Expected Shortfall differences and...

We introduce a novel class of systemic risk measures, the Vulnerability Conditional risk measures, which try to capture the "tail risk" of a risky position in scenarios where one or more market partic...

In this paper, we study the risk sharing problem among multiple agents using Lambda Value-at-Risk as their preference functional, under heterogeneous beliefs, where beliefs are represented by several ...

This paper introduces an innovative framework for the periodic evaluation of defined-contribution pension funds. The performance of the pension fund is evaluated not only at retirement, but also withi...

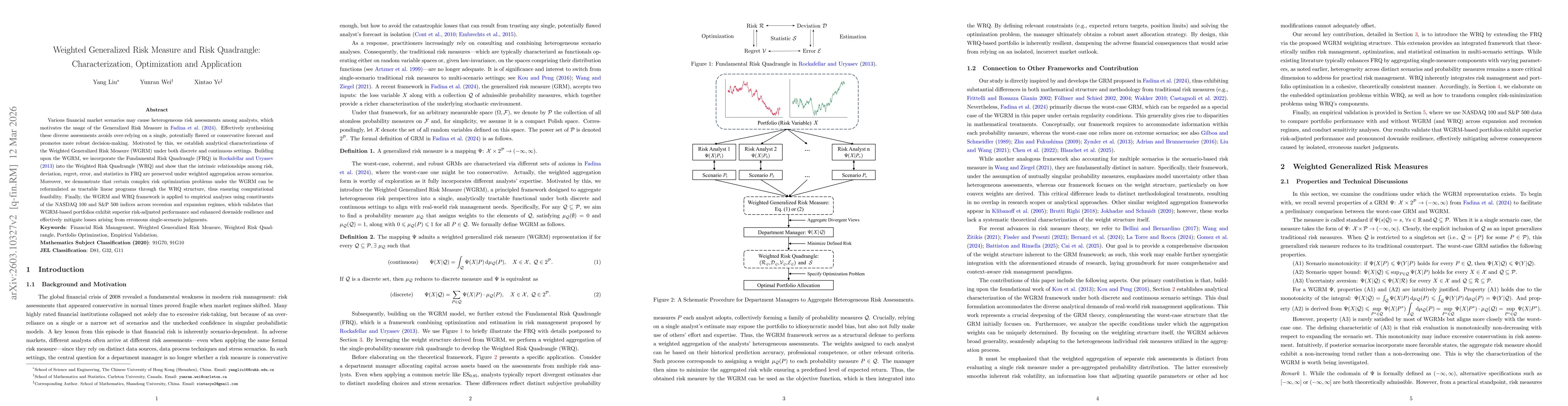

Various financial market scenarios may cause heterogeneous risk assessments among analysts, which motivates the usage of the Generalized Risk Measure in Fadina et al. (2024, Finance and Stochastics). ...

We propose a noise-robust elicit-to-optimize framework that integrates inverse reinforcement learning (IRL) and reinforcement learning (RL) for eliciting agents' risk preferences and optimizing polici...