Academic Profile

Statistics

Similar Authors

Papers on arXiv

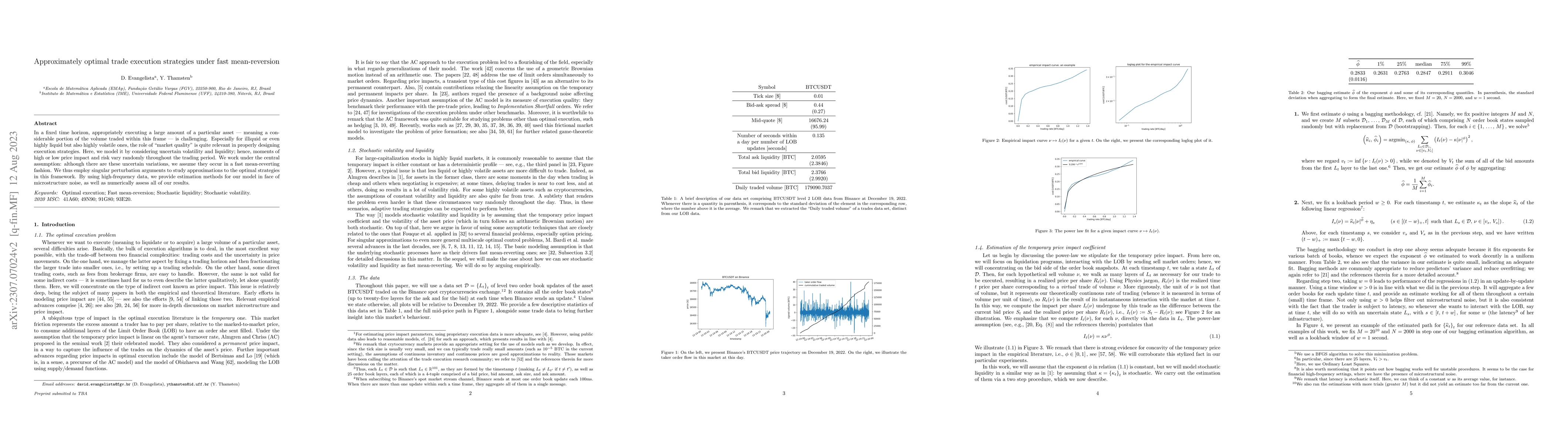

In a fixed time horizon, appropriately executing a large amount of a particular asset -- meaning a considerable portion of the volume traded within this frame -- is challenging. Especially for illiq...

We investigate Pareto equilibria for bi-objective optimal control problems. Our framework comprises the situation in which an agent acts with a distributed control in a portion of a given domain, an...

We investigate the null controllability property of systems that mathematically describe the dynamics of some non-Newtonian incompressible viscous flows. The principal model we study was proposed by...

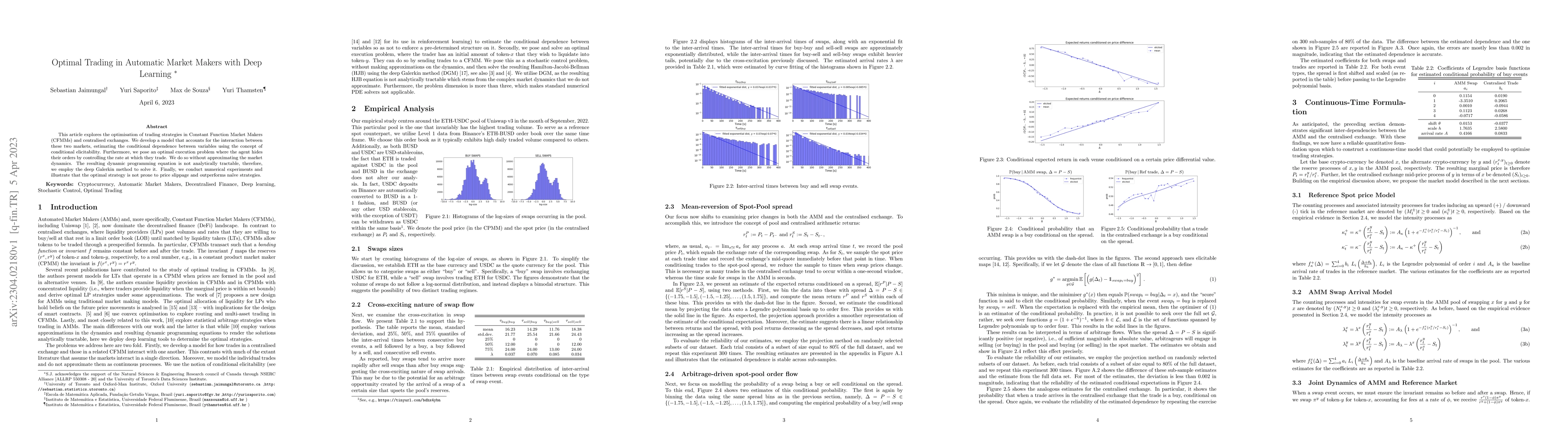

This article explores the optimisation of trading strategies in Constant Function Market Makers (CFMMs) and centralised exchanges. We develop a model that accounts for the interaction between these ...

Modeling social interactions is a challenging task that requires flexible frameworks. For instance, dissimulation and externalities are relevant features influencing such systems -- elements that ar...

We propose two novel frameworks to study the price formation of an asset negotiated in an order book. Specifically, we develop a game-theoretic model in many-person games and mean-field games, consi...

We investigate the portfolio execution problem under a framework in which volatility and liquidity are both uncertain. In our model, we assume that a multidimensional Markovian stochastic factor dri...

We investigate stochastic differential games of optimal trading comprising a finite population. There are market frictions in the present framework, which take the form of stochastic permanent and t...