Academic Profile

Statistics

Similar Authors

Papers on arXiv

This study explores the innovative use of Large Language Models (LLMs) as analytical tools for interpreting complex financial regulations. The primary objective is to design effective prompts that gui...

Systemic risk refers to the risk that the financial system is susceptible to failures due to the characteristics of the system itself. The tremendous cost of systemic risk requires the design and im...

We build a balance sheet-based model to capture run risk, i.e., a reduced potential to raise capital from liquidity buffers under stress, driven by depositor scrutiny and further fueled by fire sale...

In this paper, we introduce a novel centrality measure to evaluate shock propagation on financial networks capturing a notion of contagion and systemic risk contributions. In comparison to many popu...

Price-mediated contagion occurs when a positive feedback loop develops following a drop in asset prices which forces banks and other financial institutions to sell their holdings. Prior studies of s...

In Feinstein and Rudloff (2023), it was shown that the set of Nash equilibria for any non-cooperative $N$ player game coincides with the set of Pareto optimal points of a certain vector optimization...

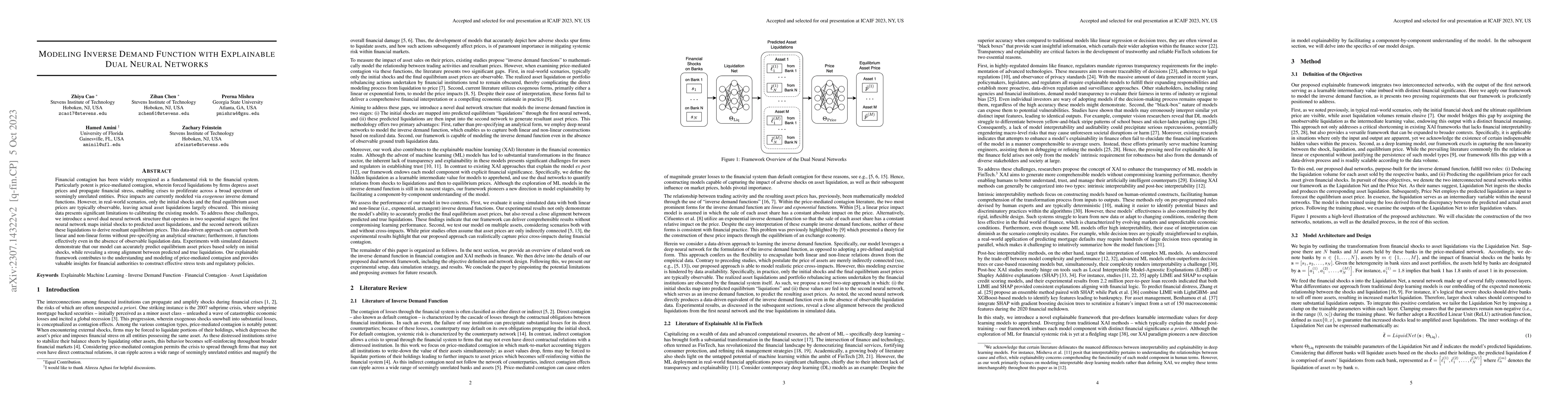

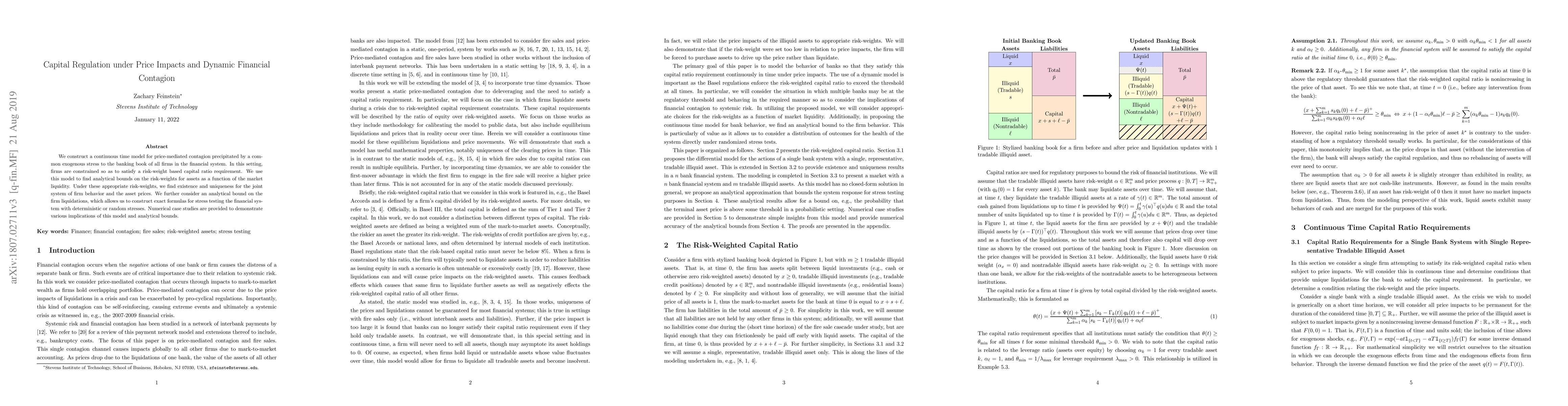

Financial contagion has been widely recognized as a fundamental risk to the financial system. Particularly potent is price-mediated contagion, wherein forced liquidations by firms depress asset pric...

Prediction markets allow traders to bet on potential future outcomes. These markets exist for weather, political, sports, and economic forecasting. Within this work we consider a decentralized frame...

We introduce a rigorous framework for stochastic cell transmission models for general traffic networks. The performance of traffic systems is evaluated based on preference functionals and acceptable...

Within this work we consider an axiomatic framework for Automated Market Makers (AMMs). By imposing reasonable axioms on the underlying utility function, we are able to characterize the properties o...

In this paper, we design a neural network architecture to approximate the weakly efficient frontier of convex vector optimization problems (CVOP) satisfying Slater's condition. The proposed machine ...

Nash equilibria and Pareto optimality are two distinct concepts when dealing with multiple criteria. It is well known that the two concepts do not coincide. However, in this work we show that it is ...

In this paper, we construct a decentralized clearing mechanism which endogenously and automatically provides a claims resolution procedure. This mechanism can be used to clear a network of obligatio...

We introduce a heterogeneous formulation of a contagious McKean-Vlasov system, whose inherent heterogeneity comes from asymmetric interactions with a natural and highly tractable structure. It is sh...

The relationship between set-valued risk measures for processes and vectors on the optional filtration is investigated. The equivalence of risk measures for processes and vectors and the equivalence...

In this paper, we propose a clearing model for prices in a financial markets due to margin calls on short sold assets. In doing so, we construct an explicit formulation for the prices that would res...

In this work we present an equilibrium formulation for price impacts. This is motivated by the Buhlmann equilibrium in which assets are sold into a system of market participants, e.g. a fire sale in...

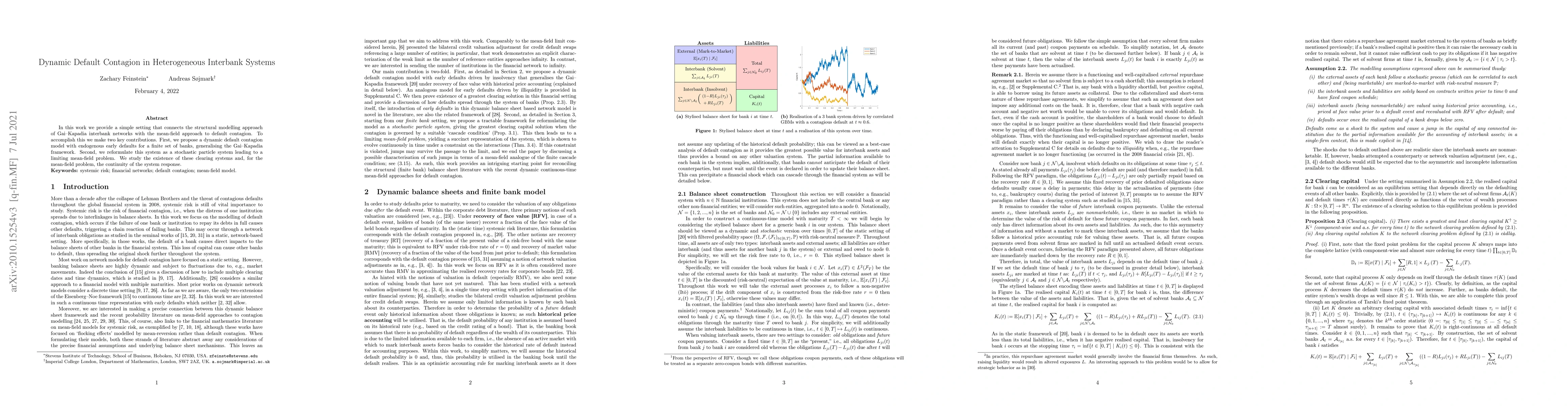

In this work we provide a simple setting that connects the structural modelling approach of Gai-Kapadia interbank networks with the mean-field approach to default contagion. To accomplish this we ma...

This paper introduces a formulation of the optimal network compression problem for financial systems. This general formulation is presented for different levels of network compression or rerouting a...

In this paper we consider continuity of the set of Nash equilibria and approximate Nash equilibria for parameterized games. For parameterized games with unique Nash equilibria, the continuity of thi...

This paper investigates whether a financial system can be made more stable if financial institutions share risk by exchanging contingent convertible (CoCo) debt obligations. The question is framed i...

We consider a network of banks that optimally choose a strategy of asset liquidations and borrowing in order to cover short term obligations. The borrowing is done in the form of collateralized repu...

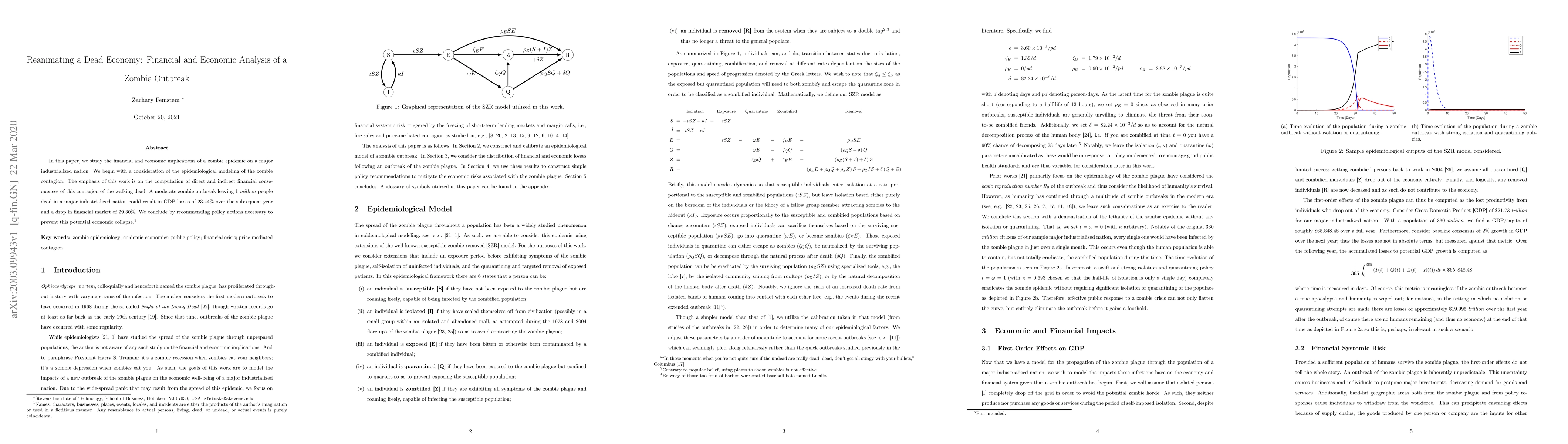

In this paper, we study the financial and economic implications of a zombie epidemic on a major industrialized nation. We begin with a consideration of the epidemiological modeling of the zombie con...

Nonzero sum games typically have multiple Nash equilibriums (or no equilibrium), and unlike the zero sum case, they may have different values at different equilibriums. Instead of focusing on the ex...

In this work we introduce a model of default contagion that combines the approaches of Eisenberg-Noe interbank networks and dynamic mean field interactions. The proposed contagion mechanism provides...

In this paper we present results on dynamic multivariate scalar risk measures, which arise in markets with transaction costs and systemic risk. Dual representations of such risk measures are present...

In this paper we present results on scalar risk measures in markets with transaction costs. Such risk measures are defined as the minimal capital requirements in the cash asset. First, some results ...

We construct a continuous time model for price-mediated contagion precipitated by a common exogenous stress to the banking book of all firms in the financial system. In this setting, firms are const...

In this paper we introduce a generalized extension of the Eisenberg-Noe model of financial contagion to allow for time dynamics of the interbank liabilities, including a dynamic examination of defau...

Empirically, the prevailing market prices for liquidity tokens of the constant product market maker (CPMM) -- as offered in practice by companies such as Uniswap -- readily permit arbitrage opportunit...

Risk measures for random vectors have been considered in multi-asset markets with transaction costs and financial networks in the literature. While the theory of set-valued risk measures provide an ax...

Systemic risk measures aggregate the risks from multiple financial institutions to find system-wide capital requirements. Though much attention has been given to assessing the level of systemic risk, ...

Environmental, Social, and Governance (ESG) factors aim to provide non-financial insights into corporations. In this study, we investigate whether we can extract relevant ESG variables to assess corpo...

We study constrained bi-matrix games, with a particular focus on low-rank games. Our main contribution is a framework that reduces low-rank games to smaller, equivalent constrained games, along with a...

An automated market maker (AMM) provides a method for creating a decentralized exchange on the blockchain. For this purpose, individual investors lend liquidity to the AMM pool in exchange for a strea...

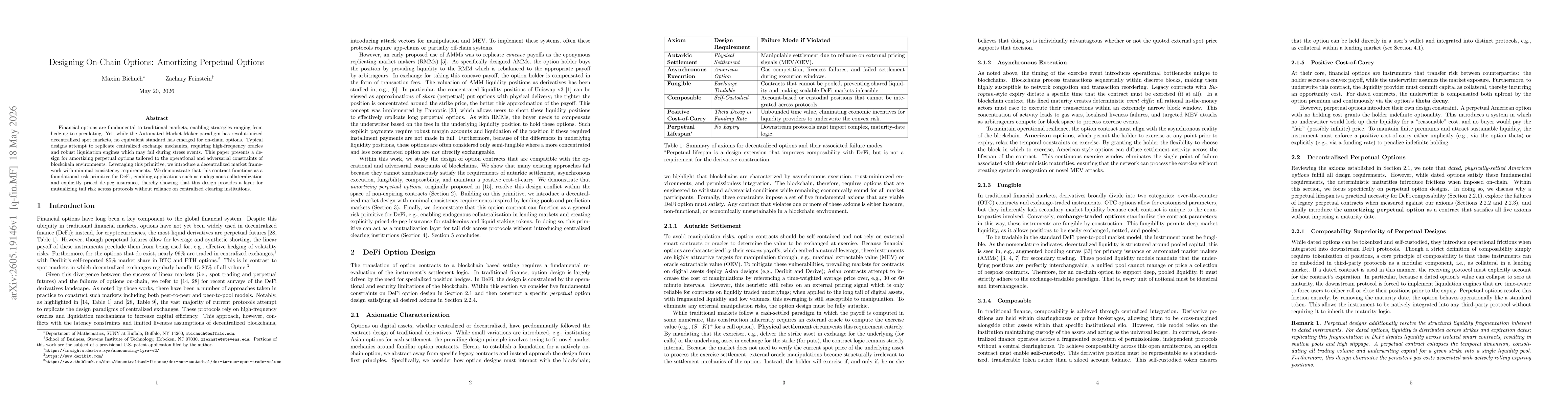

In this work, we introduce amortizing perpetual options (AmPOs), a fungible variant of continuous-installment options suitable for exchange-based trading. Traditional installment options lapse when ho...

Liquidation of collateral are the primary safeguard for solvency of lending protocols in decentralized finance. However, the mechanics of liquidations expose these protocols to predatory price manipul...

Financial options are fundamental to traditional markets, enabling strategies ranging from hedging to speculating. Yet, while the Automated Market Maker paradigm has revolutionized decentralized spot ...