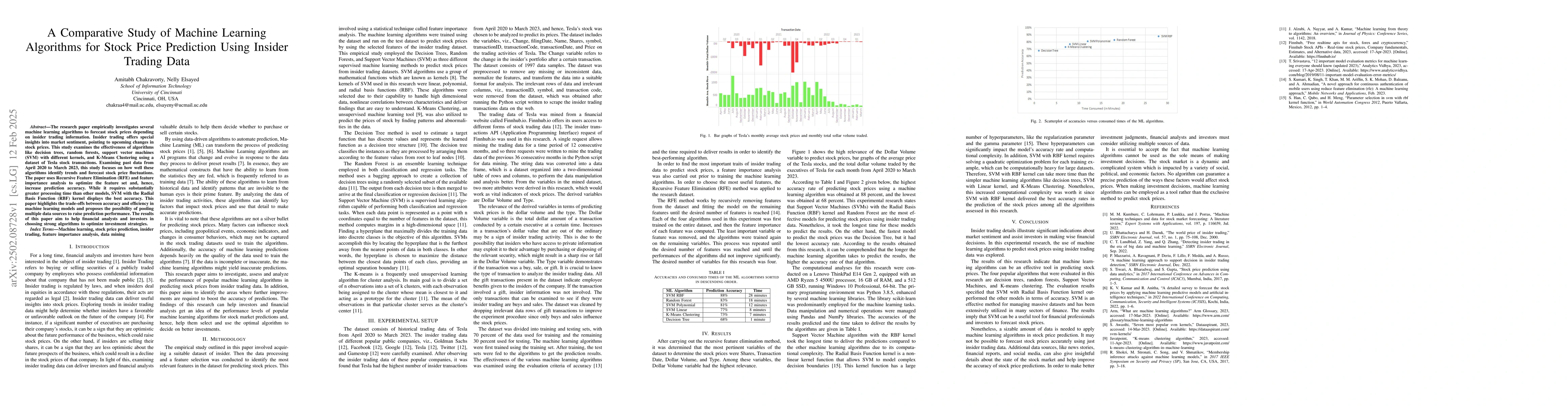

The research paper empirically investigates several machine learning

algorithms to forecast stock prices depending on insider trading information.

Insider trading offers special insights into market sentiment, pointing to

upcoming changes in stock prices. This study examines the effectiveness of

algorithms like decision trees, random forests, support vector machines (SVM)

with different kernels, and K-Means Clustering using a dataset of Tesla stock

transactions. Examining past data from April 2020 to March 2023, this study

focuses on how well these algorithms identify trends and forecast stock price

fluctuations. The paper uses Recursive Feature Elimination (RFE) and feature

importance analysis to optimize the feature set and, hence, increase prediction

accuracy. While it requires substantially greater processing time than other

models, SVM with the Radial Basis Function (RBF) kernel displays the best

accuracy. This paper highlights the trade-offs between accuracy and efficiency

in machine learning models and proposes the possibility of pooling multiple

data sources to raise prediction performance. The results of this paper aim to

help financial analysts and investors in choosing strong algorithms to optimize

investment strategies.

Discussion 0