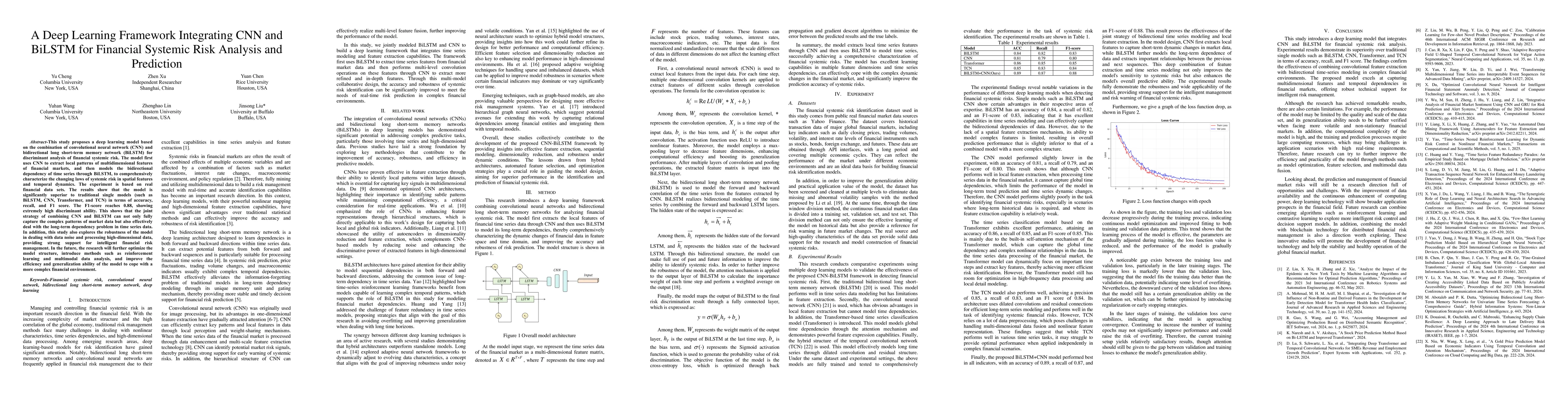

This study proposes a deep learning model based on the combination of

convolutional neural network (CNN) and bidirectional long short-term memory

network (BiLSTM) for discriminant analysis of financial systemic risk. The

model first uses CNN to extract local patterns of multidimensional features of

financial markets, and then models the bidirectional dependency of time series

through BiLSTM, to comprehensively characterize the changing laws of systemic

risk in spatial features and temporal dynamics. The experiment is based on real

financial data sets. The results show that the model is significantly superior

to traditional single models (such as BiLSTM, CNN, Transformer, and TCN) in

terms of accuracy, recall, and F1 score. The F1-score reaches 0.88, showing

extremely high discriminant ability. This shows that the joint strategy of

combining CNN and BiLSTM can not only fully capture the complex patterns of

market data but also effectively deal with the long-term dependency problem in

time series data. In addition, this study also explores the robustness of the

model in dealing with data noise and processing high-dimensional data,

providing strong support for intelligent financial risk management. In the

future, the research will further optimize the model structure, introduce

methods such as reinforcement learning and multimodal data analysis, and

improve the efficiency and generalization ability of the model to cope with a

more complex financial environment.

Discussion 0