Publication

Metrics

Paper Preview

Abstract

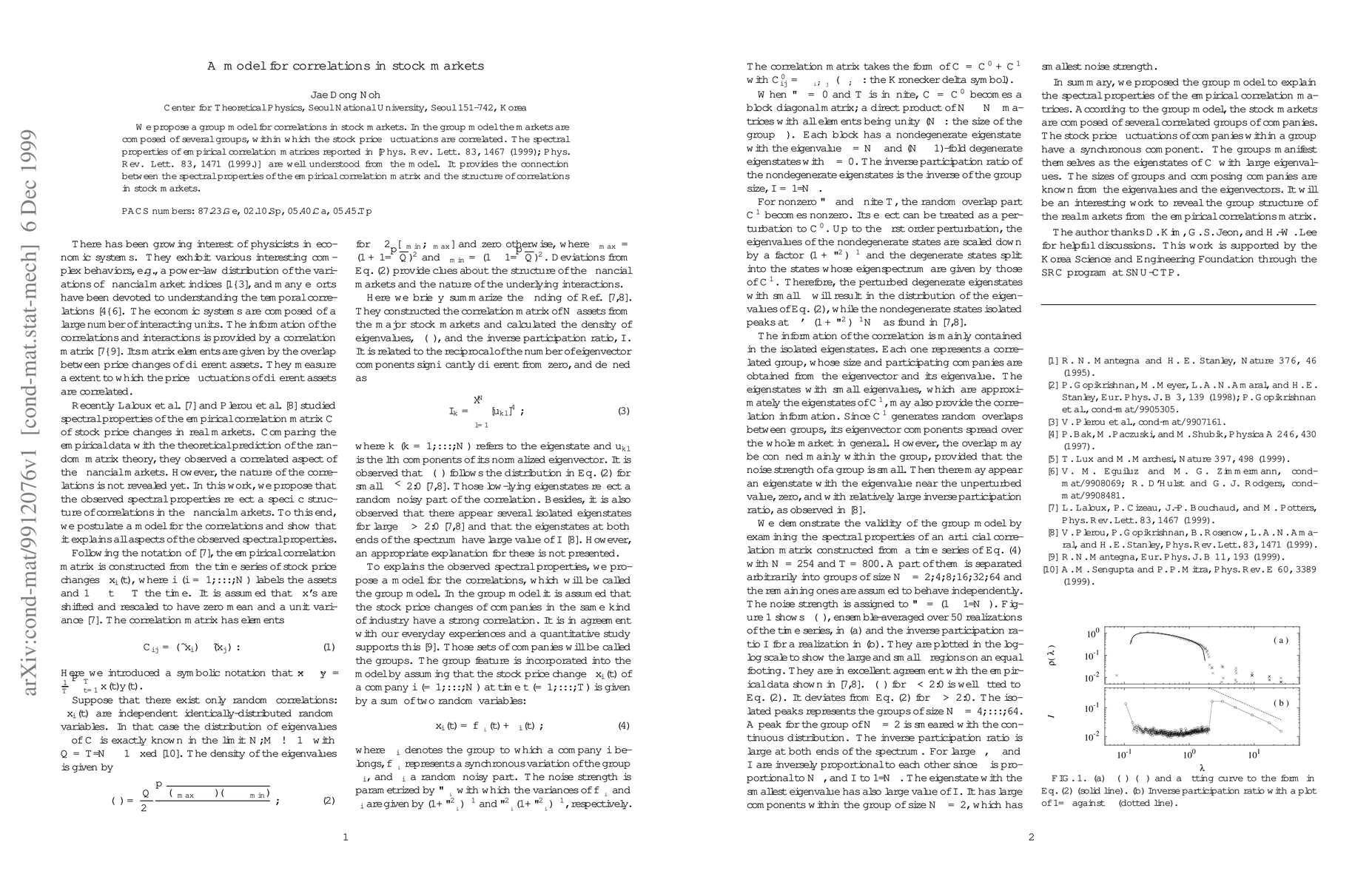

We propose a group model for correlations in stock markets. In the group model the markets are composed of several groups, within which the stock price fluctuations are correlated. The spectral properties of empirical correlation matrices reported in [Phys. Rev. Lett. {\bf 83}, 1467 (1999); Phys. Rev. Lett. {\bf 83}, 1471 (1999.)] are well understood from the model. It provides the connection between the spectral properties of the empirical correlation matrix and the structure of correlations in stock markets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Related Papers

No references found for this paper.

Discussion 0