Investment style groups investment approaches to predict portfolio return

variations. This study examines the relationship between investment style,

style consistency, and risk-adjusted returns of Indian equity mutual funds. The

methodology involves estimating size and style beta coefficients, identifying

breakpoints, analysing investment styles, and assessing risk-shifting

intensity. Funds transition across styles over time, reflecting rotation,

drift, or strengthening trends. Many Mid Blend funds remain in the same

category, while others shift to Large Blend or Mid Value, indicating

value-oriented strategies or large-cap exposure. Some funds adopt high-return

styles like Small Value and Small Blend, aiming for alpha through small-cap

equities. Performance changes following risk structure shifts are analyzed by

comparing pre- and post-shift metrics, showing that style adjustments can

enhance returns based on market conditions. This study contributes to mutual

fund evaluation literature by highlighting the impact of style transitions on

returns.

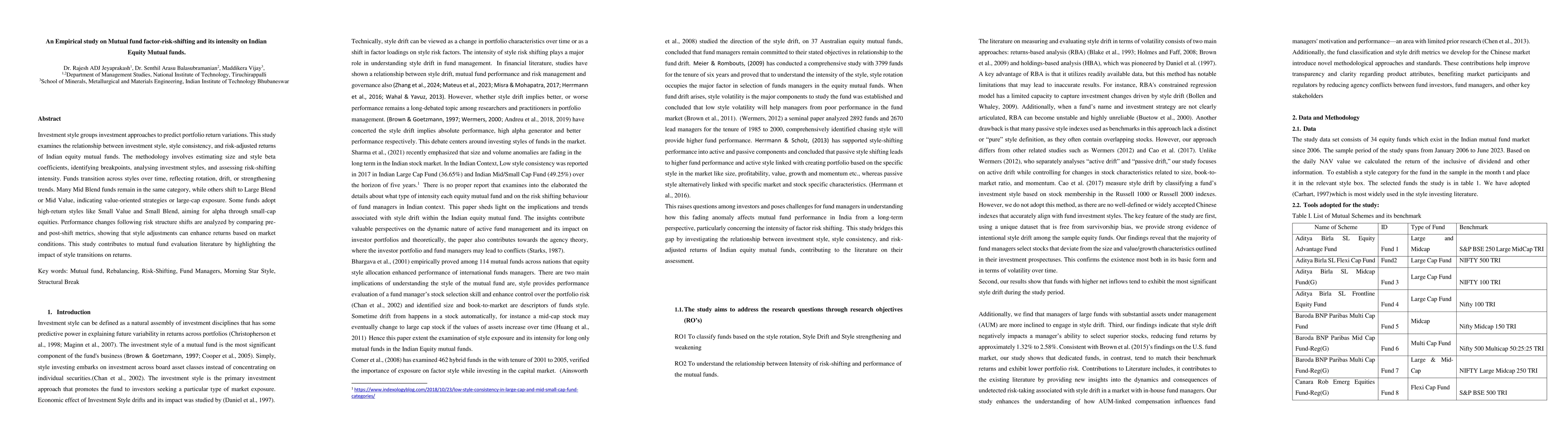

Discussion 0