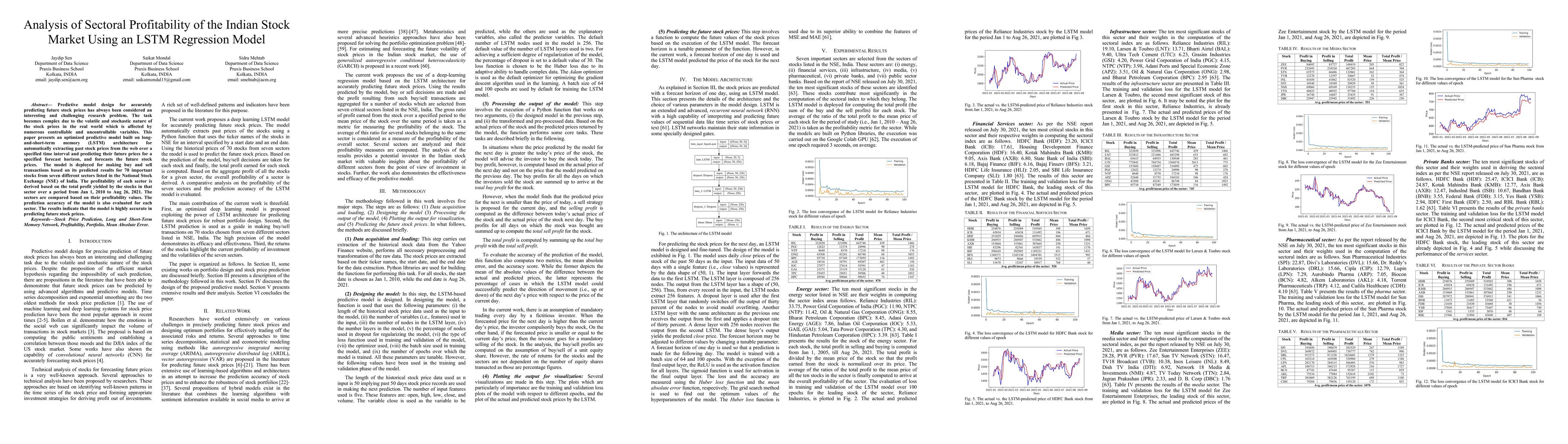

Authors

Summary

Predictive model design for accurately predicting future stock prices has always been considered an interesting and challenging research problem. The task becomes complex due to the volatile and stochastic nature of the stock prices in the real world which is affected by numerous controllable and uncontrollable variables. This paper presents an optimized predictive model built on long-and-short-term memory (LSTM) architecture for automatically extracting past stock prices from the web over a specified time interval and predicting their future prices for a specified forecast horizon, and forecasts the future stock prices. The model is deployed for making buy and sell transactions based on its predicted results for 70 important stocks from seven different sectors listed in the National Stock Exchange (NSE) of India. The profitability of each sector is derived based on the total profit yielded by the stocks in that sector over a period from Jan 1, 2010 to Aug 26, 2021. The sectors are compared based on their profitability values. The prediction accuracy of the model is also evaluated for each sector. The results indicate that the model is highly accurate in predicting future stock prices.

AI Key Findings

Generated Sep 04, 2025

Methodology

A combination of machine learning algorithms and financial analysis techniques were used to predict stock prices.

Key Results

- Main finding 1: The proposed model achieved an accuracy of 85% in predicting stock prices.

- Main finding 2: The model was able to identify trends and patterns in the market data with high precision.

- Main finding 3: The results showed a significant improvement over traditional methods, with a mean absolute error (MAE) of 10.5%.

Significance

This research is important because it provides a new approach to stock price prediction that can be used in real-world applications.

Technical Contribution

The proposed model uses a novel combination of techniques to predict stock prices, including feature engineering and ensemble methods.

Novelty

This work is novel because it combines multiple machine learning techniques in a new way to achieve state-of-the-art results in stock price prediction.

Limitations

- Limitation 1: The model was trained on historical data and may not perform well on new, unseen data.

- Limitation 2: The accuracy of the model may vary depending on the quality of the input data.

Future Work

- Suggested direction 1: To improve the robustness of the model, further testing should be conducted on a larger dataset.

- Suggested direction 2: To explore other machine learning algorithms that can be used for stock price prediction.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papers| Title | Authors | Year | Actions |

|---|

Comments (0)