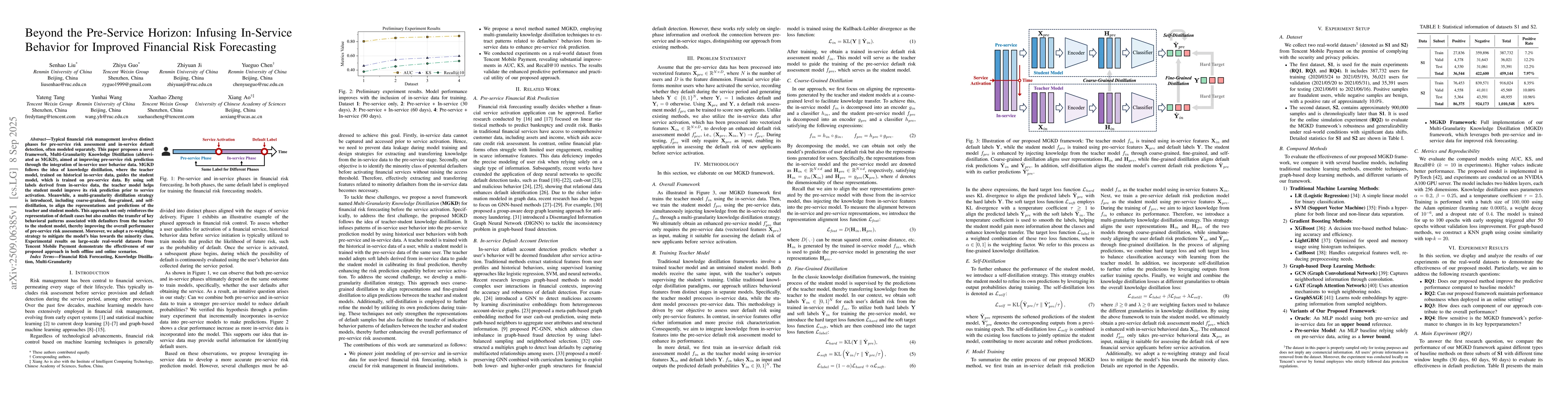

Typical financial risk management involves distinct phases for pre-service

risk assessment and in-service default detection, often modeled separately.

This paper proposes a novel framework, Multi-Granularity Knowledge Distillation

(abbreviated as MGKD), aimed at improving pre-service risk prediction through

the integration of in-service user behavior data. MGKD follows the idea of

knowledge distillation, where the teacher model, trained on historical

in-service data, guides the student model, which is trained on pre-service

data. By using soft labels derived from in-service data, the teacher model

helps the student model improve its risk prediction prior to service

activation. Meanwhile, a multi-granularity distillation strategy is introduced,

including coarse-grained, fine-grained, and self-distillation, to align the

representations and predictions of the teacher and student models. This

approach not only reinforces the representation of default cases but also

enables the transfer of key behavioral patterns associated with defaulters from

the teacher to the student model, thereby improving the overall performance of

pre-service risk assessment. Moreover, we adopt a re-weighting strategy to

mitigate the model's bias towards the minority class. Experimental results on

large-scale real-world datasets from Tencent Mobile Payment demonstrate the

effectiveness of our proposed approach in both offline and online scenarios.

Discussion 0