Capturing dynamics of post-earnings-announcement drift using genetic algorithm-optimised supervised learning

Publication

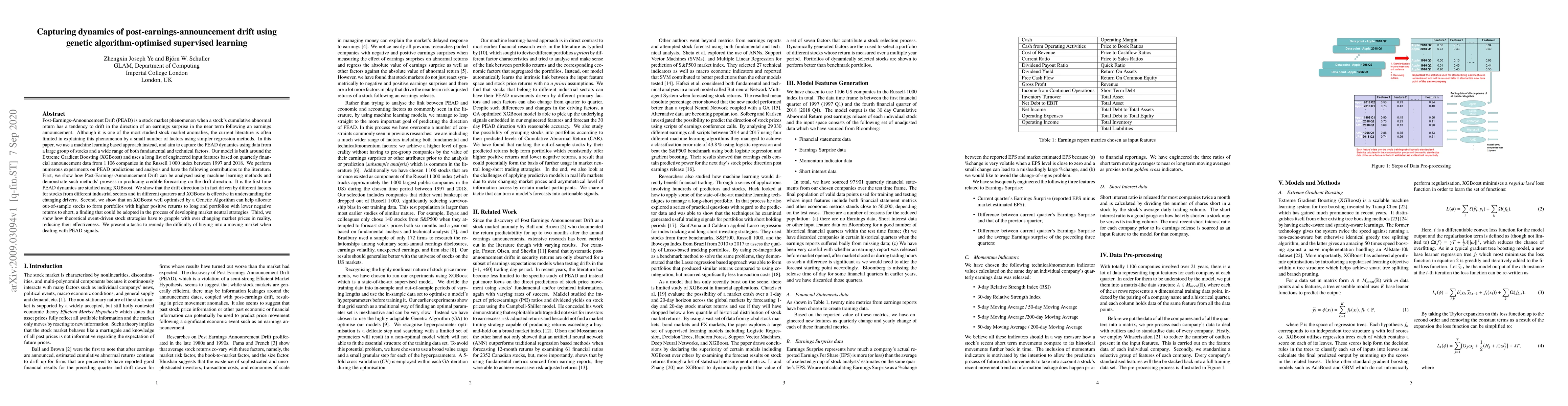

Metrics

AI Quick Summary

This paper employs Extreme Gradient Boosting (XGBoost) optimized by a Genetic Algorithm to analyze Post-Earnings-Announcement Drift (PEAD) using extensive financial data from 1,106 companies. The study demonstrates that machine learning can better capture sector-specific and temporal factors influencing PEAD, leading to improved portfolio allocation strategies.

Paper Preview

Abstract

While Post-Earnings-Announcement Drift (PEAD) is one of the most studied stock market anomalies, the current literature is often limited in explaining this phenomenon by a small number of factors using simpler regression methods. In this paper, we use a machine learning based approach instead, and aim to capture the PEAD dynamics using data from a large group of stocks and a wide range of both fundamental and technical factors. Our model is built around the Extreme Gradient Boosting (XGBoost) and uses a long list of engineered input features based on quarterly financial announcement data from 1,106 companies in the Russell 1000 index between 1997 and 2018. We perform numerous experiments on PEAD predictions and analysis and have the following contributions to the literature. First, we show how Post-Earnings-Announcement Drift can be analysed using machine learning methods and demonstrate such methods' prowess in producing credible forecasting on the drift direction. It is the first time PEAD dynamics are studied using XGBoost. We show that the drift direction is in fact driven by different factors for stocks from different industrial sectors and in different quarters and XGBoost is effective in understanding the changing drivers. Second, we show that an XGBoost well optimised by a Genetic Algorithm can help allocate out-of-sample stocks to form portfolios with higher positive returns to long and portfolios with lower negative returns to short, a finding that could be adopted in the process of developing market neutral strategies. Third, we show how theoretical event-driven stock strategies have to grapple with ever changing market prices in reality, reducing their effectiveness. We present a tactic to remedy the difficulty of buying into a moving market when dealing with PEAD signals.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0