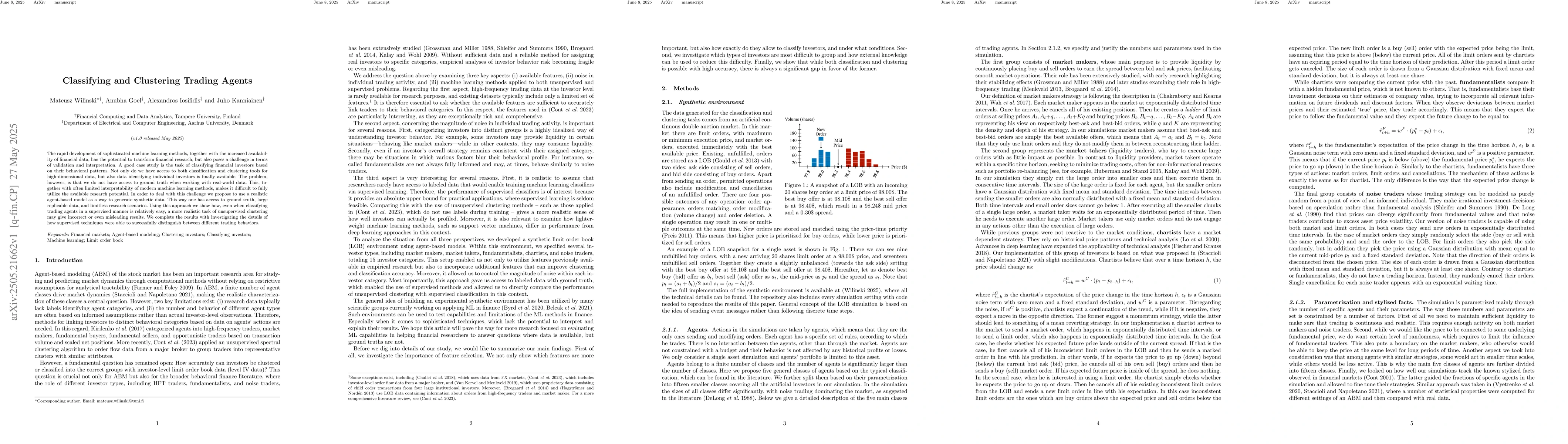

The rapid development of sophisticated machine learning methods, together

with the increased availability of financial data, has the potential to

transform financial research, but also poses a challenge in terms of validation

and interpretation. A good case study is the task of classifying financial

investors based on their behavioral patterns. Not only do we have access to

both classification and clustering tools for high-dimensional data, but also

data identifying individual investors is finally available. The problem,

however, is that we do not have access to ground truth when working with

real-world data. This, together with often limited interpretability of modern

machine learning methods, makes it difficult to fully utilize the available

research potential. In order to deal with this challenge we propose to use a

realistic agent-based model as a way to generate synthetic data. This way one

has access to ground truth, large replicable data, and limitless research

scenarios. Using this approach we show how, even when classifying trading

agents in a supervised manner is relatively easy, a more realistic task of

unsupervised clustering may give incorrect or even misleading results. We

complete the results with investigating the details of how supervised

techniques were able to successfully distinguish between different trading

behaviors.

Discussion 0