Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we introduce the Detachment Problem. It can be seen as a generalized Vaccination Problem. The aim is to optimally cut the individuals' ties to circles that connect them to others, to ...

In this research, we introduce a novel methodology for the index tracking problem with sparse portfolios by leveraging topological data analysis (TDA). Utilizing persistence homology to measure the ...

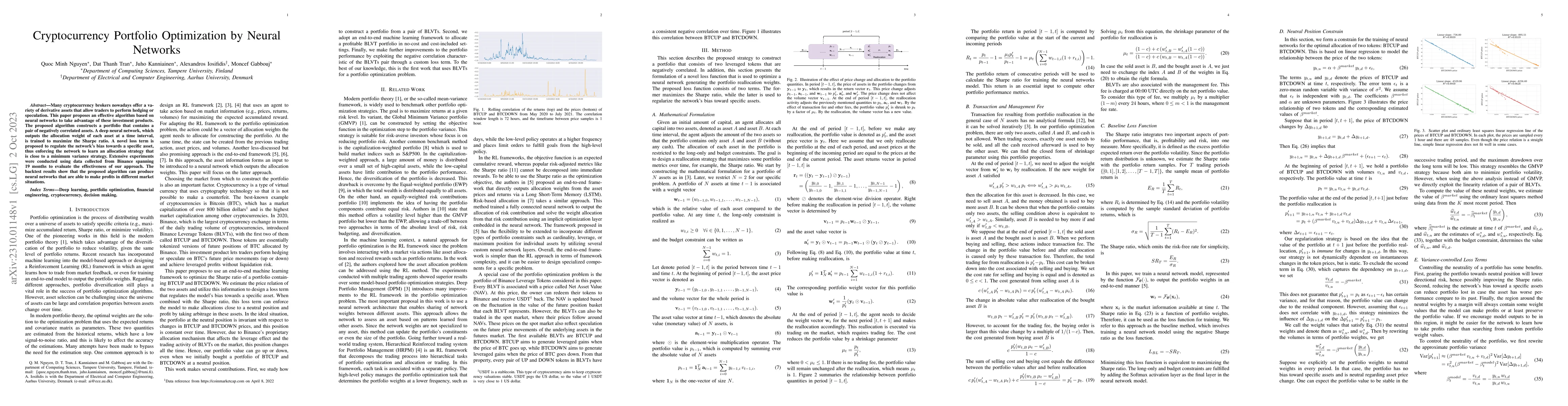

Many cryptocurrency brokers nowadays offer a variety of derivative assets that allow traders to perform hedging or speculation. This paper proposes an effective algorithm based on neural networks to...

In an increasingly digitalized commerce landscape, the proliferation of credit card fraud and the evolution of sophisticated fraudulent techniques have led to substantial financial losses. Automatin...

Emergency department (ED) crowding is a significant threat to patient safety and it has been repeatedly associated with increased mortality. Forecasting future service demand has the potential patie...

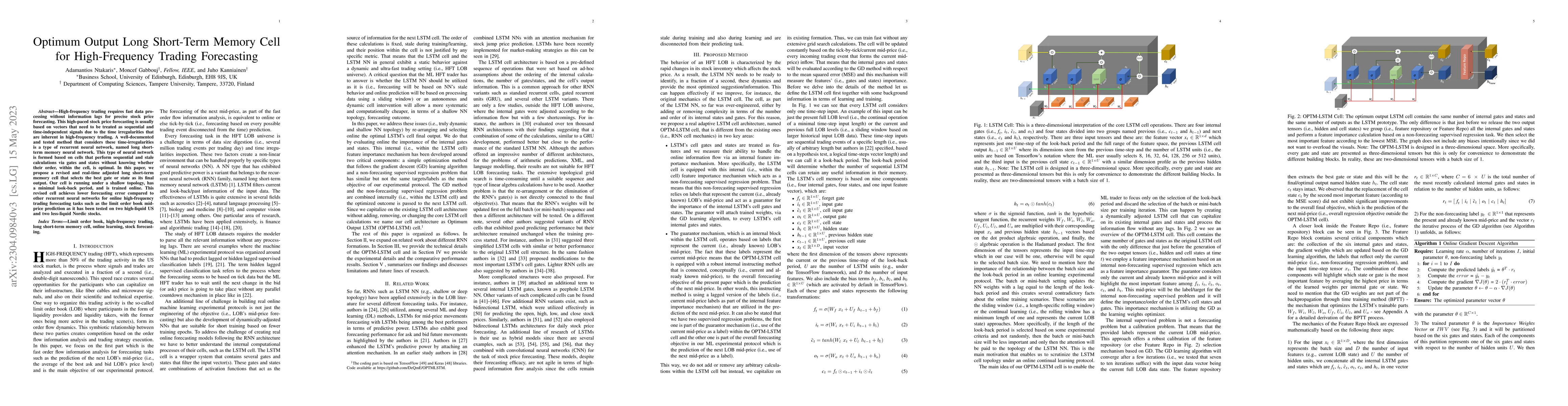

High-frequency trading requires fast data processing without information lags for precise stock price forecasting. This high-paced stock price forecasting is usually based on vectors that need to be...

Emergency department (ED) crowding is a well-recognized threat to patient safety and it has been repeatedly associated with increased mortality. Accurate forecasts of future service demand could lea...

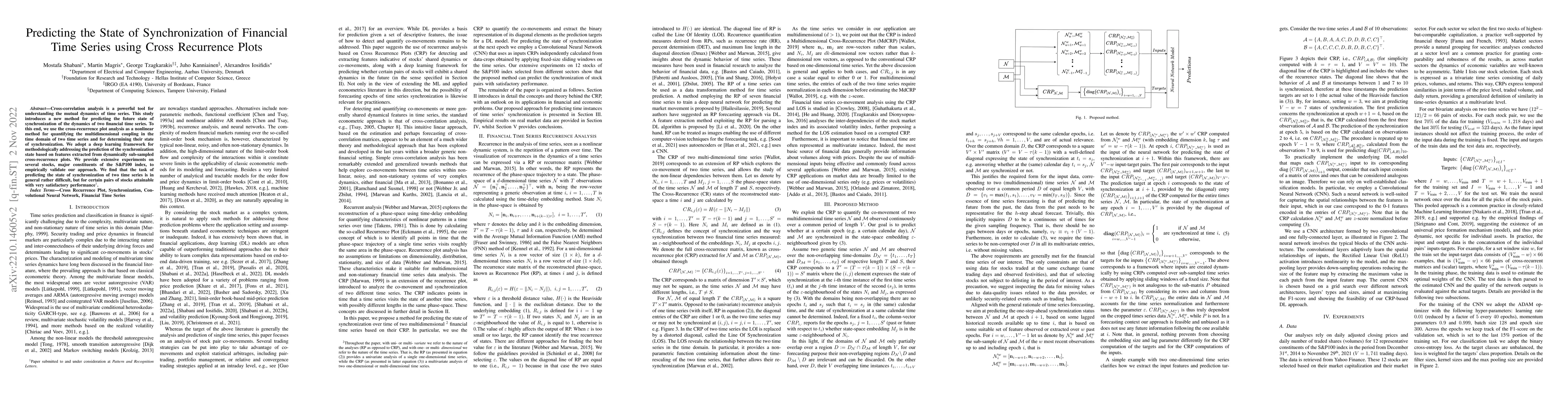

Cross-correlation analysis is a powerful tool for understanding the mutual dynamics of time series. This study introduces a new method for predicting the future state of synchronization of the dynam...

Deep Learning models have become dominant in tackling financial time-series analysis problems, overturning conventional machine learning and statistical methods. Most often, a model trained for one ...

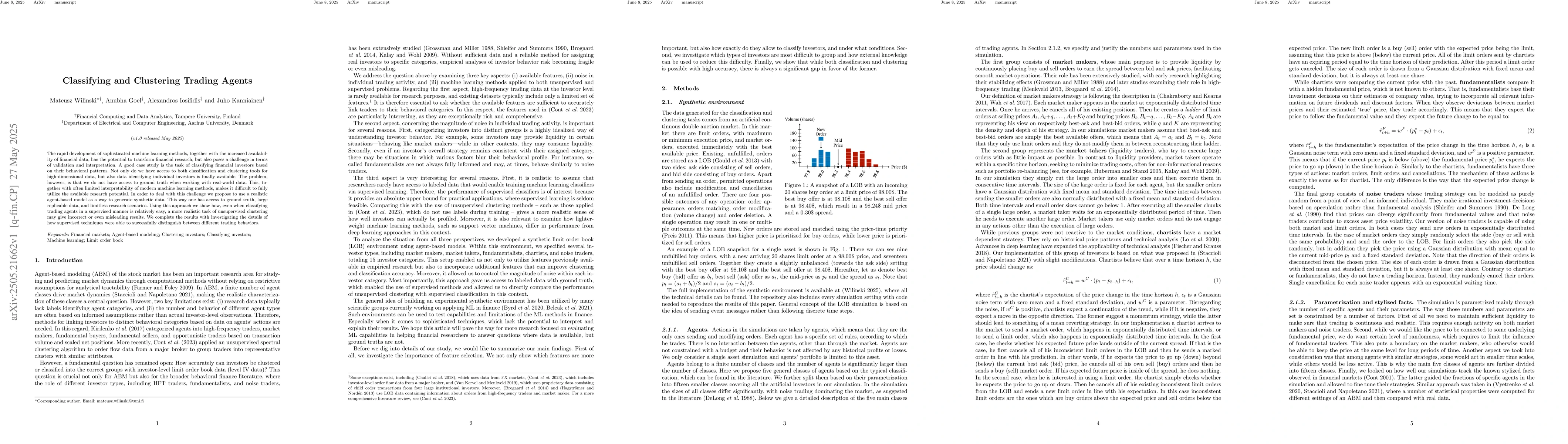

Research on limit order book markets has been rapidly growing and nowadays high-frequency full order book data is widely available for researchers and practitioners. However, it is common that resea...

Financial time-series forecasting is one of the most challenging domains in the field of time-series analysis. This is mostly due to the highly non-stationary and noisy nature of financial time-seri...

Data normalization is one of the most important preprocessing steps when building a machine learning model, especially when the model of interest is a deep neural network. This is because deep neura...

Stock price prediction is a challenging task, but machine learning methods have recently been used successfully for this purpose. In this paper, we extract over 270 hand-crafted features (factors) i...

The complex networks approach has been gaining popularity in analysing investor behaviour and stock markets, but within this approach, initial public offerings (IPO) have barely been explored. We fi...

Mid-price movement prediction based on limit order book (LOB) data is a challenging task due to the complexity and dynamics of the LOB. So far, there have been very limited attempts for extracting r...

Deep Learning (DL) models can be used to tackle time series analysis tasks with great success. However, the performance of DL models can degenerate rapidly if the data are not appropriately normaliz...

The existing literature provides evidence that limit order book data can be used to predict short-term price movements in stock markets. This paper proposes a new neural network architecture for pre...

Financial time-series forecasting has long been a challenging problem because of the inherently noisy and stochastic nature of the market. In the High-Frequency Trading (HFT), forecasting for tradin...

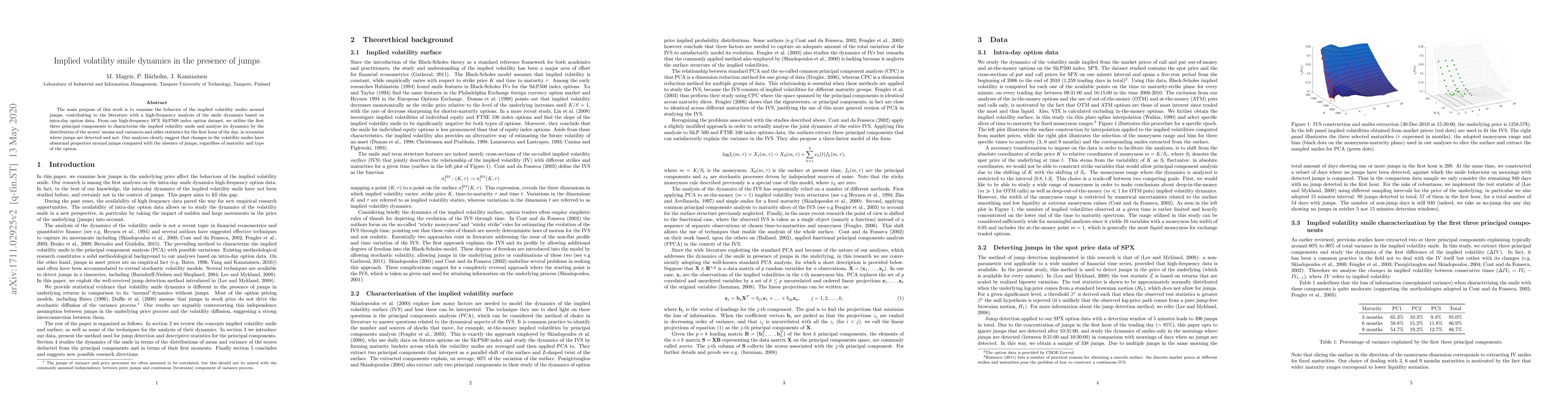

The main purpose of this work is to examine the behavior of the implied volatility smiles around jumps, contributing to the literature with a high-frequency analysis of the smile dynamics based on i...

Emergency department (ED) crowding is a global public health issue that has been repeatedly associated with increased mortality. Predicting future service demand would enable preventative measures aim...

This study is the first to explore the application of a time-series foundation model for VaR estimation. Foundation models, pre-trained on vast and varied datasets, can be used in a zero-shot setting ...

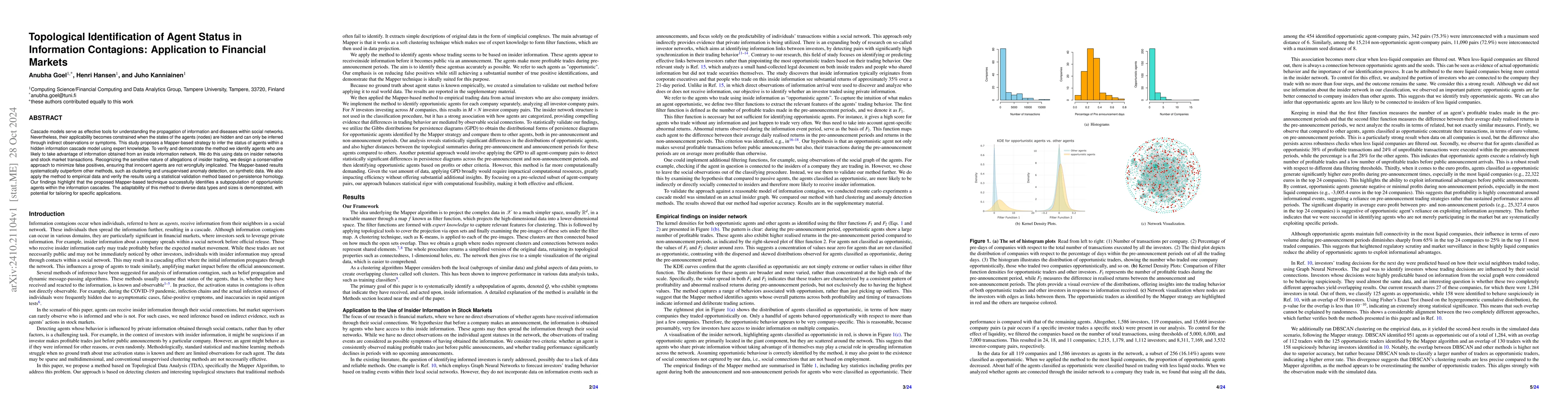

Cascade models serve as effective tools for understanding the propagation of information and diseases within social networks. Nevertheless, their applicability becomes constrained when the states of t...

The rapid development of sophisticated machine learning methods, together with the increased availability of financial data, has the potential to transform financial research, but also poses a challen...

Time series foundation models (FMs) have emerged as a popular paradigm for zero-shot multi-domain forecasting. These models are trained on numerous diverse datasets and claim to be effective forecaste...

The spreading dynamics in social networks are often studied under the assumption that individuals' statuses, whether informed or infected, are fully observable. However, in many real-world situations,...

Estimation of model uncertainty can help improve the explainability of Graph Convolutional Networks and the accuracy of the models at the same time. Uncertainty can also be used in critical applicatio...

In this work we show how generative tools, which were successfully applied to limit order book data, can be utilized for the task of imitating trading agents. To this end, we propose a modified genera...

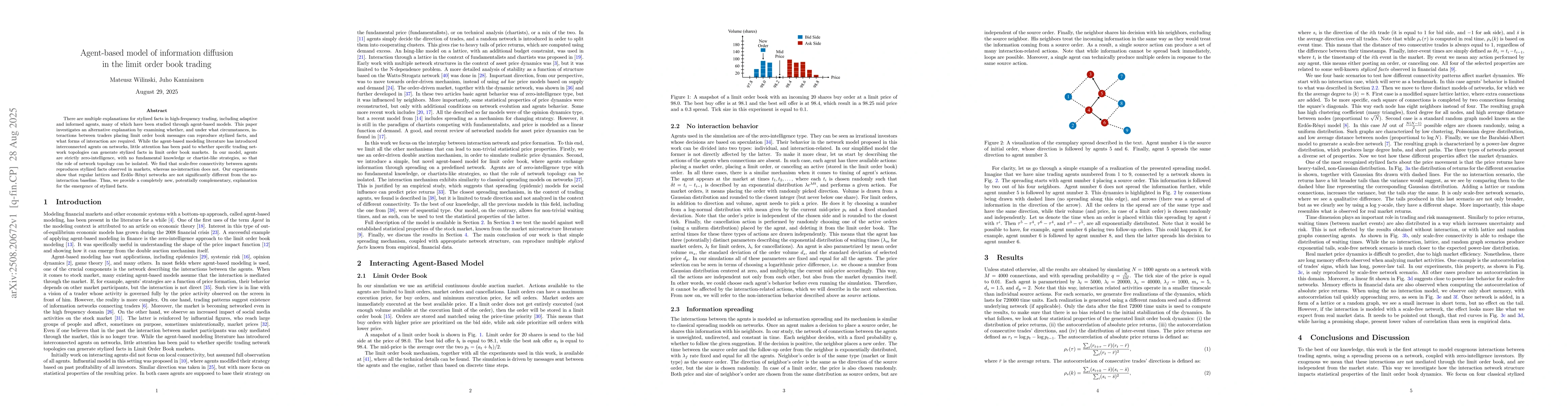

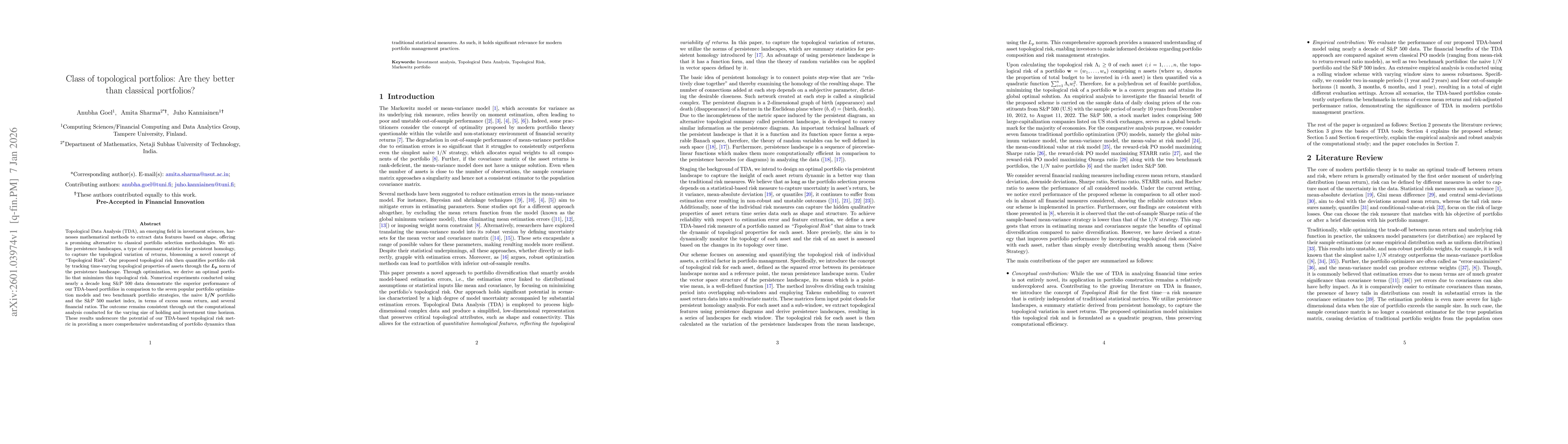

There are multiple explanations for stylized facts in high-frequency trading, including adaptive and informed agents, many of which have been studied through agent-based models. This paper investigate...

Modeling the dynamics of financial Limit Order Books (LOB) at the message level is challenging due to irregular event timing, rapid regime shifts, and the reactions of high-frequency traders to visibl...

Topological Data Analysis (TDA), an emerging field in investment sciences, harnesses mathematical methods to extract data features based on shape, offering a promising alternative to classical portfol...

Graph neural networks have achieved strong performance on graph-structured data, but their effectiveness depends heavily on the quality of the observed graph. In real applications, graph topology is o...