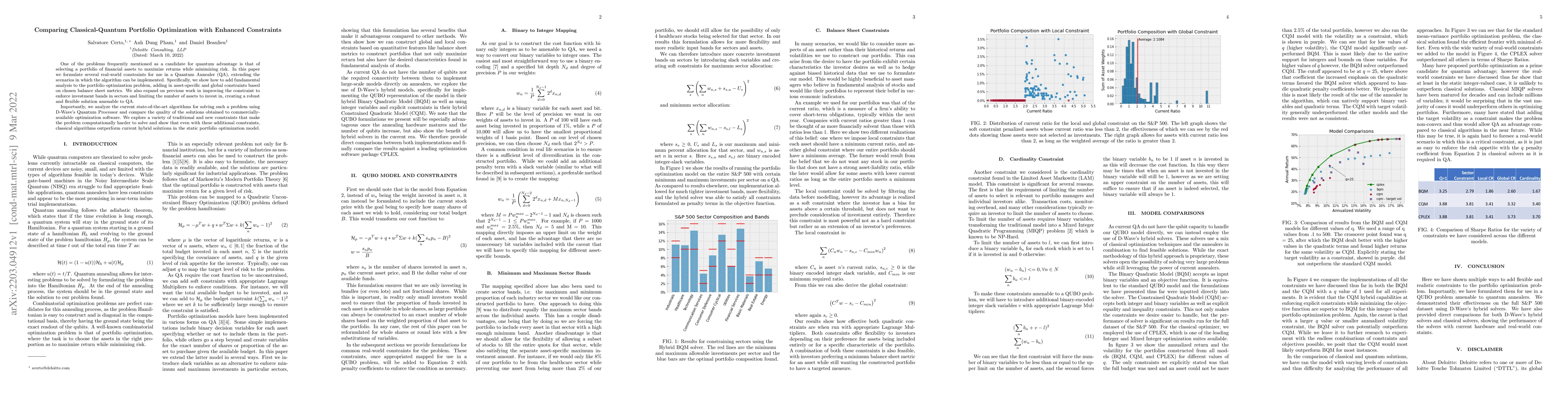

One of the problems frequently mentioned as a candidate for quantum advantage

is that of selecting a portfolio of financial assets to maximize returns while

minimizing risk. In this paper we formulate several real-world constraints for

use in a Quantum Annealer (QA), extending the scenarios in which the algorithm

can be implemented. Specifically, we show how to add fundamental analysis to

the portfolio optimization problem, adding in asset-specific and global

constraints based on chosen balance sheet metrics. We also expand on previous

work in improving the constraint to enforce investment bands in sectors and

limiting the number of assets to invest in, creating a robust and flexible

solution amenable to QA.

Importantly, we analyze the current state-of-the-art algorithms for solving

such a problem using D-Wave's Quantum Processor and compare the quality of the

solutions obtained to commercially-available optimization software. We explore

a variety of traditional and new constraints that make the problem

computationally harder to solve and show that even with these additional

constraints, classical algorithms outperform current hybrid solutions in the

static portfolio optimization model.

Discussion 0