CryptoMamba: Leveraging State Space Models for Accurate Bitcoin Price Prediction

Publication

Metrics

AI Quick Summary

CryptoMamba introduces a novel Mamba-based State Space Model to predict Bitcoin prices, surpassing traditional models by capturing long-range dependencies and regime shifts, resulting in more accurate and generalizable forecasts for cryptocurrency markets.

Paper Preview

Abstract

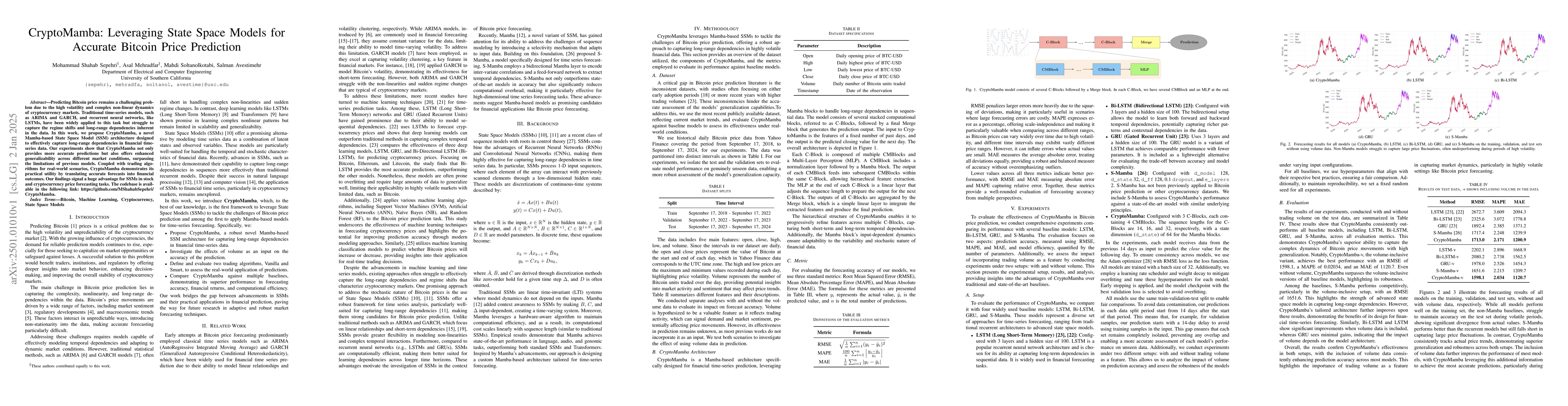

Predicting Bitcoin price remains a challenging problem due to the high volatility and complex non-linear dynamics of cryptocurrency markets. Traditional time-series models, such as ARIMA and GARCH, and recurrent neural networks, like LSTMs, have been widely applied to this task but struggle to capture the regime shifts and long-range dependencies inherent in the data. In this work, we propose CryptoMamba, a novel Mamba-based State Space Model (SSM) architecture designed to effectively capture long-range dependencies in financial time-series data. Our experiments show that CryptoMamba not only provides more accurate predictions but also offers enhanced generalizability across different market conditions, surpassing the limitations of previous models. Coupled with trading algorithms for real-world scenarios, CryptoMamba demonstrates its practical utility by translating accurate forecasts into financial outcomes. Our findings signal a huge advantage for SSMs in stock and cryptocurrency price forecasting tasks.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0