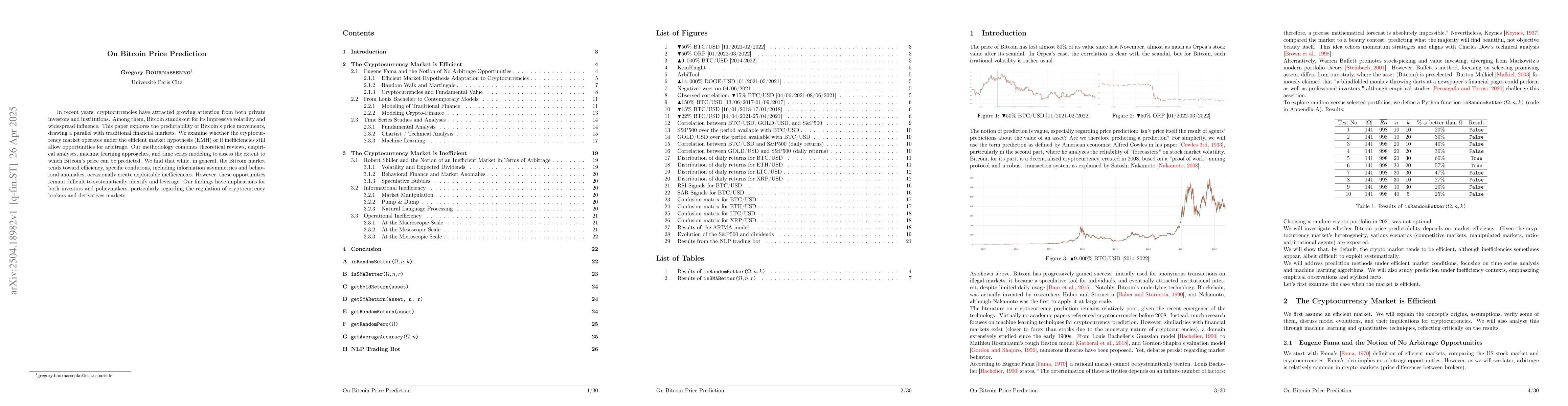

In recent years, cryptocurrencies have attracted growing attention from both

private investors and institutions. Among them, Bitcoin stands out for its

impressive volatility and widespread influence. This paper explores the

predictability of Bitcoin's price movements, drawing a parallel with

traditional financial markets. We examine whether the cryptocurrency market

operates under the efficient market hypothesis (EMH) or if inefficiencies still

allow opportunities for arbitrage. Our methodology combines theoretical

reviews, empirical analyses, machine learning approaches, and time series

modeling to assess the extent to which Bitcoin's price can be predicted. We

find that while, in general, the Bitcoin market tends toward efficiency,

specific conditions, including information asymmetries and behavioral

anomalies, occasionally create exploitable inefficiencies. However, these

opportunities remain difficult to systematically identify and leverage. Our

findings have implications for both investors and policymakers, particularly

regarding the regulation of cryptocurrency brokers and derivatives markets.

Discussion 0